PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071384

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071384

Pocket Door Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

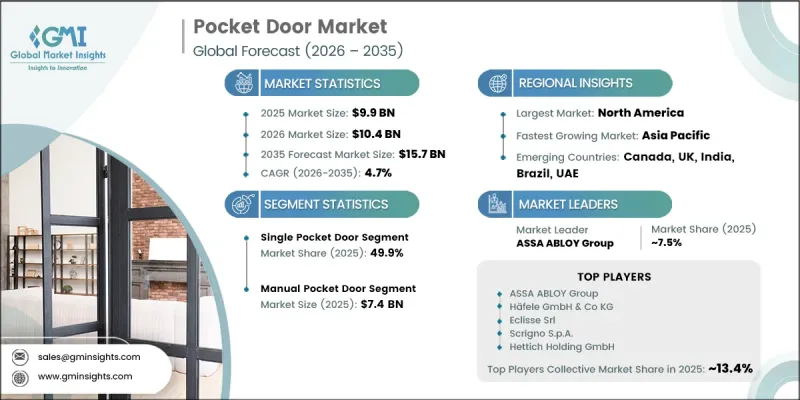

The Global Pocket Door Market was valued at USD 9.9 billion in 2025 and is estimated to grow at a CAGR of 4.7% to reach USD 15.7 billion by 2035.

Market growth is supported by the increasing adoption of space-saving interior door systems across both residential and commercial construction projects worldwide. A key factor driving demand is the ongoing reduction in average living space within densely populated urban areas across North America, Europe, and Asia Pacific, making efficient space utilization a critical design consideration. As a result, pocket doors are increasingly being incorporated into modern architectural layouts to maximize usable floor area while maintaining aesthetic appeal. Rising demand for flexible interior configurations, combined with growing investments in renovation and remodeling activities, continues to support market expansion. The industry is also benefiting from increasing preference for premium door solutions, including larger-format and technologically advanced systems that contribute to higher installation values. Commercial sectors such as healthcare, hospitality, and mixed-use developments continue to generate steady demand due to the importance of efficient space planning and streamlined interior design. At the same time, renovation projects across mature housing markets are creating additional opportunities independent of new construction activity, supporting long-term growth across the global pocket door industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.9 Billion |

| Forecast Value | $15.7 Billion |

| CAGR | 4.7% |

The single pocket door segment accounted for USD 4.9 billion in 2025, representing 49.9% share, reflecting the widespread adoption across standard residential construction projects. Its strong market position is supported by broad usage across various interior spaces where practical functionality, affordability, and efficient space management remain key purchasing considerations. The segment continues to maintain the largest installation base due to its suitability for a wide range of residential project requirements and budget levels.

The manual pocket door systems segment generated USD 7.4 billion in 2025 and represented 74.3% share. Their dominant position is largely attributed to lower installation costs, straightforward operation, and reduced maintenance requirements compared with automated alternatives. These advantages continue to support strong adoption across residential, commercial, and institutional environments. In many markets, particularly those prioritizing cost efficiency and ease of installation, manual systems remain the preferred choice and are expected to sustain substantial demand throughout the forecast period.

United States Pocket Door Market accounted for USD 2.5 billion in 2025, representing 79.5% share. Growth in the country is being driven by robust residential construction activity, increasing renovation spending, and rising demand for space-optimized interior layouts. The growing popularity of open-concept floor plans across newly constructed homes is further contributing to the adoption of pocket door systems. Additionally, accessibility-focused building requirements across healthcare facilities, hospitality properties, and public infrastructure projects continue to create consistent demand for these solutions, supporting market expansion across the region.

Key companies operating in the global pocket door market include Hettich Holding GmbH & Co. oHG, Johnson Hardware, Hafele GmbH & Co KG, Eclisse Srl, ASSA ABLOY Group, Raydoor Inc., Linvisibile S.r.l., Ferrero Legno S.p.A., Andersen Corporation, JB Kind Ltd., Bertolotto Porte S.r.l., LPD Doors Ltd., Scrigno S.p.A., Portman Doors Ltd., and Cavity Sliders. Companies operating in the pocket door market are focusing on product innovation, portfolio diversification, and strategic partnerships to strengthen their market presence and competitive positioning. Manufacturers are investing in advanced hardware systems, premium design options, and automated door technologies to address evolving consumer preferences and increase average product value. Many companies are expanding distribution networks and strengthening relationships with architects, contractors, builders, and interior designers to improve market penetration. Investments in sustainable materials, enhanced durability, and space-efficient product designs are also becoming key competitive differentiators. In addition, businesses are pursuing acquisitions, collaborations, and regional expansion initiatives to broaden their customer base and access emerging construction markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Material

- 2.2.4 Mechanism

- 2.2.5 Installation type

- 2.2.6 End-user

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid urbanization & shrinking living spaces driving space-saving solutions

- 3.2.1.2 Rising residential & commercial construction activity globally

- 3.2.1.3 Growing adoption of minimalist & open-concept interior design

- 3.2.1.4 Increasing demand for ADA-compliant & barrier-free accessibility solutions

- 3.2.1.5 Smart home integration & demand for motorized door systems

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Intense competition from barn doors & bifold door alternatives

- 3.2.2.2 Raw material price volatility (timber, aluminum, glass)

- 3.2.2.3 Lack of consumer awareness in middle-income & developing markets

- 3.2.2.4 Variability in installer skill levels leading to inconsistent outcomes

- 3.2.3 Opportunities

- 3.2.3.1 Rising demand for acoustic/soundproof pocket door systems

- 3.2.3.2 Micro-apartment & compact urban housing boom creating structural demand

- 3.2.3.3 Growing adoption of fire-rated pocket doors in commercial buildings

- 3.2.3.4 Eco-friendly & recycled material innovations aligning with green building codes

- 3.2.3.5 Untapped demand in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Trade data analysis (HS Code 4418.2)

- 3.7.1 Import/export volume & value trends

- 3.7.2 Key trade corridors & tariff impact

- 3.8 Pricing analysis

- 3.8.1 Historical price trend analysis (driven by primary research)

- 3.8.2 Pricing strategy by player type (premium / value / mass market)

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 GenAI use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Single pocket door

- 5.3 Double pocket door

- 5.4 Unilateral pocket door

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Wood

- 6.3 Glass

- 6.4 Aluminum/metal

- 6.5 Vinyl/plastic

- 6.6 Others (steel, fiberglass)

Chapter 7 Market Estimates & Forecast, By Mechanism, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Manual

- 7.3 Automatic

Chapter 8 Market Estimates & Forecast, By Installation Type, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 New construction

- 8.3 Retrofit/renovation

Chapter 9 Market Estimates & Forecast, By End-Use, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.4 Industrial

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce websites

- 10.2.2 Company-owned websites

- 10.3 Offline

- 10.3.1 Specialty stores

- 10.3.2 Departmental stores

- 10.3.3 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.4.7 Malaysia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Top Global Players

- 12.1.1 ASSA ABLOY Group

- 12.1.2 Eclisse Srl

- 12.1.3 Hafele GmbH

- 12.1.4 Johnson Hardware

- 12.1.5 Scrigno S.p.A.

- 12.2 Regional Champions

- 12.2.1 Anderson Corporation

- 12.2.2 Portman Doors

- 12.2.3 JB Kind

- 12.2.4 Ferrero Legno

- 12.2.5 Cavity Sliders

- 12.3 Emerging Players

- 12.3.1 Raydoor Inc.

- 12.3.2 Bertolotto Porte

- 12.3.3 LPD Doors

- 12.3.4 Linvisibile

- 12.3.5 Hettich Holding