PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071328

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071328

Kitchen Faucets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

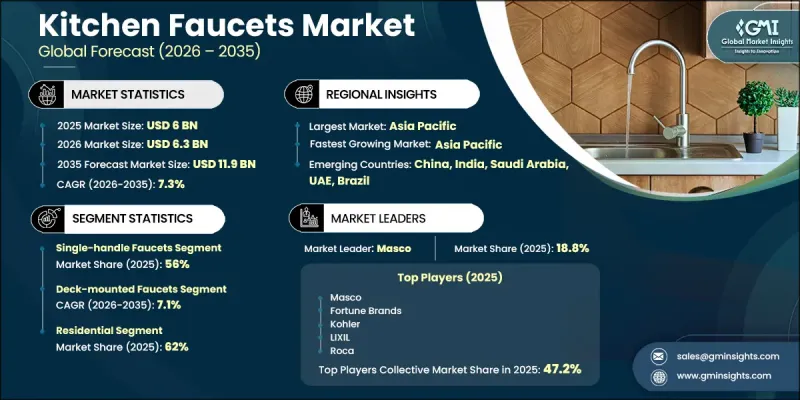

The Global Kitchen Faucets Market was valued at USD 6 billion in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 11.9 billion by 2035.

Market expansion is driven by a combination of steady residential replacement activity in established economies, rising initial installation demand in rapidly urbanizing regions, and a clear shift toward premium and technology-enabled faucet designs that command higher price realization. The industry demonstrates strong structural stability, as kitchen faucets typically fall into a semi-essential renovation category where replacement is triggered more by wear, design obsolescence, or functional decline rather than purely economic sentiment. This creates a consistent baseline demand even during periods of macroeconomic uncertainty. Unlike more discretionary home renovation segments, kitchen faucet replacement tends to remain steady across cycles, supporting long-term resilience. Additionally, ongoing product innovation, including smart functionality, improved water efficiency, and enhanced finishes, is contributing to higher average selling prices, ensuring revenue growth continues to outpace unit expansion. Increasing urbanization, especially in emerging economies, is further reinforcing demand through new housing development and first-time installations. Overall, the market is benefiting from both replacement-driven consumption in mature regions and expansion-led demand in developing economies, creating a balanced and sustainable growth trajectory across the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6 Billion |

| Forecast Value | $11.9 Billion |

| CAGR | 7.3% |

Single-handle faucets accounted for 56% share in 2025 and is projected to grow at a CAGR of 7.8% through 2035, making it the fastest-growing product category. Demand for this segment is supported by ease of use, simplified installation, and compatibility with modern compact kitchen layouts. The design allows efficient temperature and water flow control through a single mechanism, making it widely preferred across residential and commercial applications. Its adoption is also reinforced by increasing integration of advanced features such as touch and motion-based controls, which align well with single-handle configurations. As modern kitchen design continues to prioritize convenience and space efficiency, this segment is expected to maintain strong momentum throughout the forecast period.

The deck-mounted faucets segment held an 84% share in 2025. This installation type continues to lead due to its broad compatibility with standard kitchen sink designs and ease of installation across both residential and commercial environments. Its widespread use is supported by flexible design applications and availability across multiple price points, ranging from entry-level to premium product categories. The segment benefits from established consumer familiarity and consistent demand across renovation and new construction activities, reinforcing its leading position in the market structure.

North America Kitchen Faucets Market accounted for 29% share in 2025 and is expected to grow at a CAGR of 7.2% through 2035. The United States remains the primary contributor to regional demand, supported by a large installed base of residential housing and ongoing kitchen renovation activity. Replacement demand remains steady due to aging infrastructure and continuous home improvement investments. Strong distribution networks and well-established retail channels further support product accessibility across the region. Canada is also contributing to market growth through sustained residential development activity and multi-family housing expansion in major urban centers, supporting incremental demand for kitchen faucet installations.

Key companies operating in the global kitchen faucets market include Masco Corporation, LIXIL Corporation, Fortune Brands Home & Security, Roca Group, and Kohler Co. Companies operating in the kitchen faucets market are focusing on several strategic initiatives to strengthen their competitive position and expand market share. Product innovation remains central, with manufacturers introducing advanced faucet designs that incorporate water efficiency, durable materials, and smart functionality. Investments in design aesthetics and premium finishes are helping brands differentiate their offerings in an increasingly competitive environment. Companies are also expanding their presence across digital retail channels and strengthening partnerships with distributors, contractors, and home improvement retailers to improve market reach. Geographic expansion into high-growth regions is another key focus area, supported by localized product development strategies. In addition, mergers, acquisitions, and portfolio diversification are enabling firms to enhance their technological capabilities and broaden their product offerings, while continuous research and development investments are ensuring long-term competitiveness and sustained brand positioning.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Valve mechanism

- 2.2.4 Technology

- 2.2.5 Application

- 2.2.6 Price range

- 2.2.7 End users

- 2.2.8 Distribution channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Price trends

- 3.4.1 Historical price trend analysis

- 3.4.2 Pricing strategy by player type

- 3.5 Regulatory framework

- 3.5.1 US Regulations: WaterSense Program, Lead-Free Mandates (Safe Drinking Water Act)

- 3.5.2 European Regulations: EU Construction Products Regulation, REACH (Hexavalent Chromium)

- 3.5.3 Asia Pacific Regulations: BIS (India), China GB Standards, Japan JIS

- 3.5.4 Water Efficiency Standards & Certifications by Region (WaterSense, WELS, WRAS, EU Ecolabel)

- 3.5.5 Building Codes & Plumbing Standards Impact on Product Design (IPC, UPC, EN 817)

- 3.6 Porter's five forces analysis

- 3.7 PESTEL analysis

- 3.8 Trade data analysis (based on paid database) (HS Code: 8481.80)

- 3.8.1 Import/export volume & value trends

- 3.8.2 Key trade corridors & tariff impact

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of traditional business models

- 3.9.2 GenAI use cases & adoption roadmap by customer segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Future market trends

- 3.11 Technology and innovation landscape

- 3.11.1 Current technological trends

- 3.11.2 Emerging technologies

- 3.12 Consumer behavior analysis

- 3.12.1 Purchasing patterns

- 3.12.2 Preference analysis

- 3.12.3 Regional variations in consumer behavior

- 3.12.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Single-handle faucets

- 5.2.1 Standard/stationary single handle

- 5.2.2 Pull-down single-handle

- 5.2.3 Pull-out single-handle

- 5.2.4 Swivel spout single-handle

- 5.3 Dual-handle faucets

- 5.3.1 Centerset dual handle

- 5.3.2 Widespread dual handle

- 5.3.3 Bridge dual-handle

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Stainless steel

- 6.3 Brass

- 6.4 Chrome/nickel alloy

- 6.5 Bronze/copper

- 6.6 Plastic/polymer

- 6.7 Others (zinc alloys, composite materials etc.)

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Manual kitchen faucets

- 7.3 Electronic/automatic kitchen faucets

- 7.3.1 Sensor/infrared-activated (touchless) kitchen faucets

- 7.3.2 Touch-activated kitchen faucets

- 7.3.3 Voice-activated kitchen faucets

Chapter 8 Market Estimates & Forecast, By Mounting Type, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Deck-mounted faucets

- 8.3 Wall-mounted faucets

Chapter 9 Market Estimates & Forecast, By Price Range, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Low (under US$ 50)

- 9.3 Medium (US$ 50 - US$ 199)

- 9.4 High (US$ 200 - US$ 499)

- 9.5 Premium (US$ 500 and above)

Chapter 10 Market Estimates & Forecast, By End Users, 2022 - 2035 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 Residential

- 10.3 Commercial

- 10.3.1 Hospitality

- 10.3.2 Healthcare

- 10.3.3 Office & corporate buildings

- 10.3.4 Retail & food service establishments

- 10.3.5 Educational institutions

- 10.4 Industrial

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 11.1 Key trends

- 11.2 Online

- 11.2.1 E-commerce

- 11.2.2 Company websites

- 11.3 Offline

- 11.3.1 Supermarkets/hypermarket

- 11.3.2 Specialty retail stores

- 11.3.3 Others (independent retailer etc.)

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Spain

- 12.3.5 Italy

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 Japan

- 12.4.3 India

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global Key Players

- 13.1.1 Fortune Brands

- 13.1.2 Hansgrohe

- 13.1.3 Kohler

- 13.1.4 LIXIL

- 13.1.5 Masco

- 13.1.6 Roca Group

- 13.1.7 TOTO

- 13.2 Regional Players

- 13.2.1 Arrow Home Group

- 13.2.2 Cera Sanitaryware

- 13.2.3 FM Mattsson

- 13.2.4 Hindware (HSIL Ltd.)

- 13.2.5 Huida Sanitary Ware

- 13.2.6 Oras Group

- 13.2.7 Vitra (Eczacibasi Group)

- 13.3 Emerging/Niche Specialists

- 13.3.1 Bravat

- 13.3.2 Chicago Faucets

- 13.3.3 Fantini Rubinetti

- 13.3.4 Gessi

- 13.3.5 T&S Brass and Bronze Works

- 13.3.6 THG Paris

- 13.3.7 Zucchetti Rubinetteria