PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071372

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071372

Freight Forwarding Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

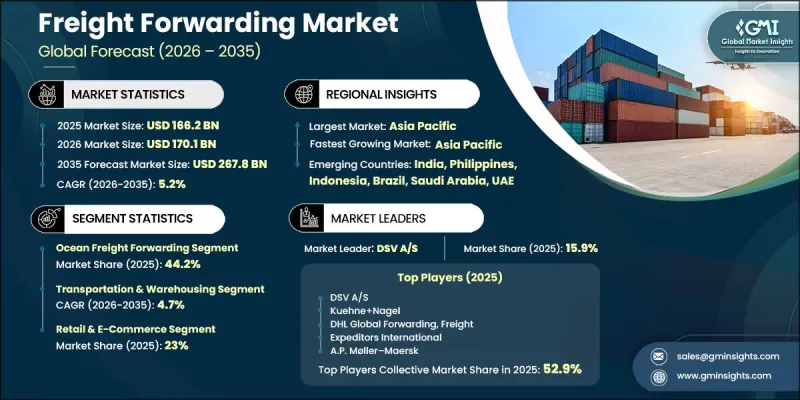

The Global Freight Forwarding Market was valued at USD 166.2 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 267.8 billion by 2035.

Growth in the market continues to be supported by rising international trade activity and the increasing complexity of global supply chains. Freight forwarding providers play a critical role in coordinating transportation networks, managing customs requirements, optimizing shipping routes, and ensuring timely delivery across multiple regions. As companies diversify manufacturing and sourcing operations, demand for efficient logistics coordination is increasing across global markets. The ongoing reconfiguration of supply chains is changing shipment origins and trade patterns, creating new opportunities for freight forwarding companies without reducing overall demand for forwarding services. Businesses are increasingly seeking flexible logistics solutions capable of managing multi-country sourcing strategies and evolving trade requirements. At the same time, fluctuating transportation costs and fuel-related expenses continue to influence market dynamics, encouraging greater emphasis on pricing transparency and risk management. Digitalization is also transforming the industry, with advanced freight management platforms becoming an essential component of procurement and logistics operations. As customers demand greater visibility, operational efficiency, and real-time shipment tracking, technology-enabled freight forwarding services are becoming increasingly important across global transportation networks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $166.2 Billion |

| Forecast Value | $267.8 Billion |

| CAGR | 5.2% |

The transportation and warehousing segment generated USD 103.4 billion in 2025, accounting for 62.2% share. Although growth remains slightly below the overall market average, this reflects an evolving service mix that increasingly favors higher-value logistics solutions rather than weakness in core transportation activities. Service providers are expanding integrated offerings that combine transportation management, storage capabilities, inventory control, and logistics coordination, enabling them to generate greater value per shipment while strengthening customer relationships and improving operational efficiency.

China Freight Forwarding Market accounted for USD 41.4 billion in 2025 and is expected to reach USD 71.1 billion by 2035. Market growth is supported by the country's strong export activity, extensive logistics infrastructure, and strategic role within international trade networks. The region continues to serve as a major hub for manufacturing, sourcing, and global distribution, creating sustained demand for freight forwarding services. Growing trade volumes, expanding cross-border logistics requirements, and increasing supply chain complexity continue to support long-term market opportunities throughout the country and the broader Asia Pacific region.

Key participants operating in the global freight forwarding market include DHL Global, Kuehne+Nagel International, DSV A/S, CEVA Logistics, Sinotrans, GEODIS, Expeditors International, Nippon Express, A.P. Moller - Maersk, and C.H. Robinson. Companies operating in the freight forwarding market are adopting a variety of strategic initiatives to strengthen their market position and expand their global presence. Investments in digital transformation remain a primary focus, with providers implementing advanced logistics platforms, real-time shipment visibility tools, data analytics, and automation technologies to improve service efficiency. Market participants are also expanding integrated logistics capabilities by combining transportation, warehousing, inventory management, and value-added supply chain services into comprehensive solutions. Strategic acquisitions, regional expansion initiatives, and partnerships with carriers and logistics providers are helping companies broaden their geographic reach and service offerings. In addition, businesses are prioritizing sustainability initiatives, operational optimization, and customer-centric service models to enhance competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Mode of Transport

- 2.2.2 Service

- 2.2.3 End Use

- 2.2.4 Customer

- 2.2.5 Enterprise Size

- 2.2.6 Region

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component suppliers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Service providers

- 3.1.1.5 Distribution channel

- 3.1.1.6 End Use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of Global Trade and Cross-Border Commerce

- 3.2.1.2 Growth of E-Commerce and Omnichannel Retail Logistics

- 3.2.1.3 Supply Chain Diversification and Nearshoring Initiatives

- 3.2.1.4 Increasing Outsourcing of Logistics and Transportation Functions

- 3.2.1.5 Rising Demand for High-Value and Time-Sensitive Shipments

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Geopolitical Tensions and Trade Uncertainties

- 3.2.2.2 Volatility in Freight Rates and Fuel Prices

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of Emerging Trade Corridors

- 3.2.3.2 Adoption of Digital Freight and Logistics Platforms

- 3.2.3.3 Growth of Cold Chain and Temperature-Controlled Logistics

- 3.2.3.4 Increasing Demand for Sustainable and Green Logistics Solutions

- 3.2.3.5 Expansion of Integrated End-to-End Supply Chain Services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 U.S.: Federal Maritime Commission (FMC) - Ocean Transportation Intermediary (OTI) Regulations

- 3.5.1.2 U.S.: Transportation Security Administration (TSA) Air Cargo Security Requirements

- 3.5.1.3 U.S.: Customs and Border Protection (CBP) Customs Trade Partnership Against Terrorism (CTPAT)

- 3.5.1.4 Canada: Canada Border Services Agency (CBSA) Customs Regulations

- 3.5.1.5 Canada: Partners in Protection (PIP) Supply Chain Security Program

- 3.5.1.6 Canada: Provincial E-Bike Regulations

- 3.5.2 Europe

- 3.5.2.1 European Union Customs Code (UCC)

- 3.5.2.2 Authorized Economic Operator (AEO) Program

- 3.5.2.3 EU Import Control System 2 (ICS2)

- 3.5.2.4 EU Mobility Package for Road Freight Transport

- 3.5.2.5 EU Emissions Trading System (ETS) for Maritime Transport

- 3.5.3 Asia-Pacific

- 3.5.3.1 China Customs Advanced Certified Enterprise (ACE) Program

- 3.5.3.2 China Regulations on International Freight Forwarding Enterprises

- 3.5.3.3 Japan Authorized Economic Operator (AEO) Framework

- 3.5.3.4 Australia Trusted Trader Program (ATT)

- 3.5.3.5 Singapore Customs TradeFIRST & Secure Trade Partnership (STP)

- 3.5.4 Latin America

- 3.5.4.1 Brazil Authorized Economic Operator (AEO) Program

- 3.5.4.2 Brazil National Land Transport Agency (ANTT) Freight Regulations

- 3.5.4.3 Mexico Authorized Economic Operator (OEA) Program

- 3.5.4.4 Mexico Customs Law and Foreign Trade Regulations

- 3.5.5 Middle East & Africa

- 3.5.5.1 GCC Unified Customs Law

- 3.5.5.2 UAE Authorized Economic Operator (AEO) Program

- 3.5.5.3 Saudi Arabia Zakat, Tax and Customs Authority (ZATCA) Logistics Regulations

- 3.5.5.4 South Africa Customs and Excise Act

- 3.5.5.5 African Continental Free Trade Area (AfCFTA) Trade Facilitation Framework

- 3.5.1 North America

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 Automated design optimization

- 3.10.3 Supply chain AI for demand forecasting

- 3.10.4 GenAI use cases & adoption roadmap by segment

- 3.10.5 Risks, Limitations & Regulatory Considerations

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Customer & Shipper Analysis

- 3.12.1 Freight Procurement Behavior by Enterprise Size

- 3.12.2 Key Vendor Selection Criteria by Industry

- 3.12.3 Customer Pain Point Analysis

- 3.12.4 Freight Forwarder Switching Trends & Retention Factors

- 3.12.5 Digital Adoption Preferences Among Shippers

- 3.13 Capacity & Utilization Analysis

- 3.13.1 Air Freight Capacity Utilization Trends

- 3.13.2 Ocean Container Capacity Utilization Trends

- 3.13.3 Trucking Capacity Availability & Utilization

- 3.13.4 Regional Capacity Imbalances

- 3.14 Global Trade Lane Analysis

- 3.14.1 Asia-North America Corridor

- 3.14.2 Asia-Europe Corridor

- 3.14.3 Intra-Asia Corridor

- 3.14.4 Europe-North America Corridor

- 3.14.5 Middle East-Africa Corridor

- 3.14.6 Emerging South-South Trade Corridors

- 3.15 Market Risk Assessment

- 3.15.1 Geopolitical Risk Matrix

- 3.15.2 Port Disruption Risk Assessment

- 3.15.3 Cybersecurity Risk Exposure

- 3.15.4 Regulatory & Compliance Risks

- 3.15.5 Climate & Extreme Weather Risks

- 3.16 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.16.1 Base Case - key macro & industry variables driving CAGR

- 3.16.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

- 4.5 Company tier benchmarking

- 4.5.1 Tier classification criteria & qualifying thresholds

- 4.5.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Mode of Transport, 2022 - 2035 ($Mn, 000'Tons)

- 5.1 Key trends

- 5.2 Ocean freight forwarding

- 5.3 Air freight forwarding

- 5.4 Road freight forwarding

- 5.5 Rail freight forwarding

- 5.6 Multimodal/Intermodal Freight Forwarding

Chapter 6 Market Estimates & Forecast, By Service, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Transportation & warehousing

- 6.3 Value-added services

- 6.4 Packaging

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn, 000'Tons)

- 7.1 Key trends

- 7.2 Manufacturing & Industrial

- 7.3 Retail & E-Commerce

- 7.4 Healthcare & Pharmaceuticals

- 7.5 Automotive

- 7.6 Oil, Gas & Energy

- 7.7 Food & Beverages

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Customer, 2022 - 2035 ($Mn, 000'Tons)

- 8.1 Key trends

- 8.2 B2B

- 8.3 B2C

Chapter 9 Market Estimates & Forecast, By Enterprise Size, 2022 - 2035 ($Mn, 000'Tons)

- 9.1 Key trends

- 9.2 Small and Medium Enterprises

- 9.3 Large Enterprises

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, 000'Tons)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.3.9 Thailand

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

- 10.5.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global players:

- 11.1.1 A.P. Moller - Maersk

- 11.1.2 C.H. Robinson Worldwide

- 11.1.3 CEVA Logistics

- 11.1.4 DHL Global Forwarding

- 11.1.5 DSV

- 11.1.6 Expeditors International

- 11.1.7 GEODIS

- 11.1.8 Kuehne+Nagel International

- 11.1.9 Nippon Express

- 11.1.10 Sinotrans

- 11.2 Regional Players

- 11.2.1 Agility Logistics

- 11.2.2 Aramex

- 11.2.3 Bollore Logistics

- 11.2.4 DACHSER

- 11.2.5 Hellmann Worldwide Logistics

- 11.2.6 Kerry Logistics Network (KLN)

- 11.2.7 Morrison Express

- 11.2.8 Savino Del Bene

- 11.2.9 Toll

- 11.2.10 Yusen Logistics

- 11.3 Emerging Players

- 11.3.1 Flexport

- 11.3.2 Forto

- 11.3.3 Freights

- 11.3.4 iContainers

- 11.3.5 Zencargo