PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071374

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071374

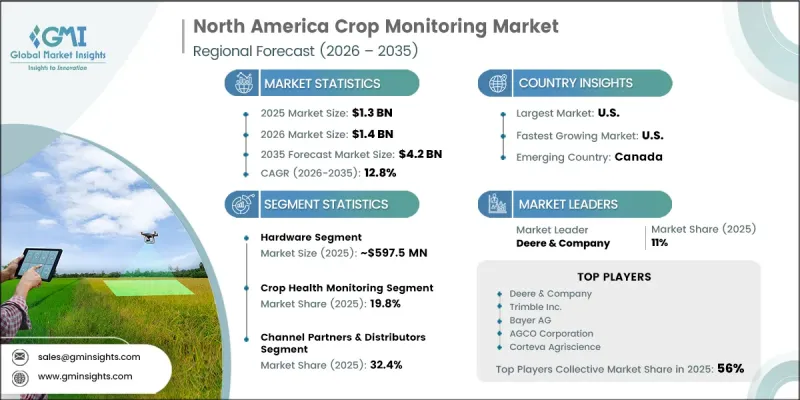

North America Crop Monitoring Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

North America Crop Monitoring Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 12.8% to reach USD 4.2 billion by 2035.

Market expansion is driven by increasing adoption of precision agriculture systems, growing deployment of satellite-enabled remote sensing technologies, and rising use of subscription-based digital farm management platforms across large commercial farming operations in the United States and Canada. A key structural driver of growth is the rising economic pressure on agricultural producers to reduce input costs while improving yield efficiency, particularly in large-scale crop production systems. In parallel, increasing climate variability is intensifying demand for real-time field intelligence and predictive agronomic insights. The rapid evolution of artificial intelligence and data analytics is further enabling the transformation of raw agricultural data into actionable decision-support tools for farmers. As a result, crop monitoring solutions are shifting from optional tools to essential operational infrastructure within modern agriculture. Increasing emphasis on productivity optimization, sustainability targets, and resource-efficient farming practices is reinforcing the adoption of integrated digital agriculture ecosystems across North America.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $4.2 Billion |

| CAGR | 12.8% |

The hardware segment held a 47.8% share, reaching USD 597.5 million in 2025. The segment's dominance is supported by the growing need for physical sensing and data-collection infrastructure required to enable precision agriculture systems at scale. This includes connected field devices, positioning systems, environmental sensing technologies, aerial monitoring platforms, and automated application control systems. Continued investment in farm digitization is strengthening hardware demand, particularly across large-scale agricultural operations where efficiency gains and input optimization are critical to profitability.

The soil monitoring segment represented 18% share in 2025 and is projected to grow at a CAGR of 12.8% through 2035. Growth in this segment is supported by increasing recognition of soil condition as a key determinant of agricultural productivity and long-term sustainability outcomes. Continuous soil data collection enables improved irrigation planning, fertilizer application timing, and field management strategies. The integration of sensor-based monitoring systems with cloud-enabled analytics platforms is further enhancing decision-making accuracy and operational efficiency across modern farming practices.

United States Crop Monitoring Market accounted for 79.5% share in 2026 and is expected to grow at a CAGR of 13.2%. Market growth is supported by the large concentration of commercial-scale farming operations, where operational scale enables higher adoption of advanced monitoring technologies. Increasing integration of digital agriculture solutions into mainstream farming practices is further accelerating market penetration. In addition, government-supported agricultural programs focused on resource efficiency and conservation practices are helping reduce adoption barriers and supporting wider deployment of precision agriculture technologies across the country.

Key companies operating in the North America crop monitoring market include Trimble Inc., CNH Industrial, Bayer AG, AGCO Corporation, Corteva Agriscience, Syngenta, Topcon Positioning Systems, Ag Leader Technology, AgEagle Aerial Systems Inc., Arable Labs Inc., Ceres Imaging Inc., CropX Technologies, EOS Data Analytics (EOSDA), Farmers Edge Inc., Intelinair Inc., Planet Labs PBC, PrecisionHawk Inc., Regrow Ag, Semios, and Sentera Inc. Companies in the North America crop monitoring market are adopting multiple strategic initiatives to strengthen their competitive positioning and expand market presence. Major players are heavily investing in artificial intelligence, machine learning, and advanced analytics capabilities to improve the accuracy and predictive power of crop insights. Many firms are integrating satellite imagery, IoT-enabled field sensors, and drone-based monitoring systems into unified digital platforms to offer end-to-end agricultural intelligence solutions. Strategic collaborations with agribusiness firms, technology providers, and research institutions are supporting faster innovation and broader adoption. Companies are also expanding subscription-based service models to ensure recurring revenue streams and long-term customer engagement.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Technology

- 2.2.3 Application

- 2.2.4 Crop Type

- 2.2.5 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Key news & initiatives

- 3.4 Technology & Innovation Landscape

- 3.5 Regulatory landscape

- 3.6 Impact on forces

- 3.6.1 Growth drivers

- 3.6.2 Industry pitfalls & challenges

- 3.6.3 Opportunities

- 3.7 Pricing analysis, 2025 (driven by primary research)

- 3.7.1 Historical price trend analysis (2022-2025)

- 3.7.2 Pricing strategy by player type (premium/value/cost-plus)

- 3.7.3 Regional price variation analysis

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Trade data analysis (driven by paid database)

- 3.11.1 Import/export volume & value trends (Driven by Primary Research)

- 3.11.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Producer (Driven by Primary Research)

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Remote Sensing & Satellite Imagery

- 6.3 UAV / Drone-Based Monitoring

- 6.4 IoT & Ground Sensors

- 6.5 AI & Machine Learning Analytics

- 6.6 Variable Rate Technology (VRT)

- 6.7 Others (GPS/GIS, Cloud, Blockchain)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Crop Health Monitoring

- 7.3 Soil Monitoring

- 7.4 Yield Monitoring & Forecasting

- 7.5 Pest & Disease Detection

- 7.6 Field Mapping

- 7.7 Irrigation Management

- 7.8 Weather Tracking & Forecasting

- 7.9 Others (VRA, Carbon Credit)

Chapter 8 Market Estimates & Forecast, By Crop Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Cereals & Grains

- 8.3 Oilseeds & Pulses

- 8.4 Fruits & Flowers

- 8.5 Stem & Tubers

- 8.6 Other (Plantation Crops, Forestry, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct Sales

- 9.3 Channel Partners & Distributors

- 9.4 Online / E-Commerce

- 9.5 OEM & System Integrators

Chapter 10 & Forecast, By Country, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 U.S.

- 10.3 Canada

Chapter 11 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 11.1 Global players

- 11.1.1 Deere & Company

- 11.1.2 Trimble Inc.

- 11.1.3 Bayer AG

- 11.1.4 AGCO Corporation

- 11.1.5 Corteva Agriscience

- 11.1.6 CNH Industrial

- 11.1.7 Planet Labs PBC

- 11.1.8 Topcon Positioning Systems

- 11.2 Regional players

- 11.2.1 Farmers Edge Inc.

- 11.2.2 Ag Leader Technology

- 11.2.3 Sentera Inc.

- 11.2.4 CropX Technologies

- 11.2.5 Intelinair Inc.

- 11.2.6 PrecisionHawk Inc.

- 11.2.7 Semios

- 11.3 Emerging players

- 11.3.1 EOS Data Analytics (EOSDA)

- 11.3.2 AgEagle Aerial Systems Inc.

- 11.3.3 Ceres Imaging Inc.

- 11.3.4 Arable Labs Inc.

- 11.3.5 Regrow Ag

- 11.3.6 Syngenta