PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071399

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071399

Agriculture Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

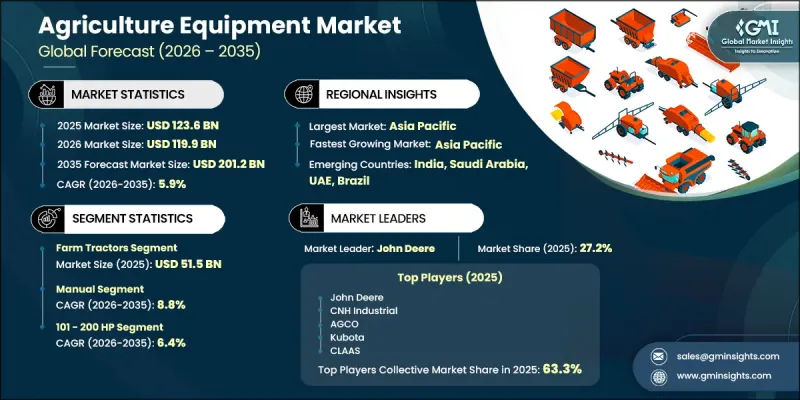

The Global Agriculture Equipment Market was valued at USD 123.6 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 201.2 billion by 2035.

The agriculture equipment market is witnessing steady expansion as rising food requirements continue to place greater pressure on agricultural productivity worldwide. Growing population levels and increasing demand for agricultural output are encouraging farmers to invest in modern machinery capable of improving operational efficiency and maximizing crop yields. Mechanized farming has become increasingly important as agricultural producers seek to optimize production on limited arable land while addressing labor availability challenges. The adoption of precision agriculture technologies is further transforming the industry by enabling more accurate field management and resource utilization. Technological developments have introduced advanced equipment equipped with intelligent systems that improve monitoring, cultivation, and harvesting activities. The integration of automation, positioning technologies, and digital farming tools is helping producers enhance productivity while reducing operational complexity. In addition, the growing emphasis on sustainable farming practices is supporting demand for environmentally responsible machinery that contributes to lower emissions, improved resource efficiency, and better soil management. These factors, combined with ongoing innovation and evolving agricultural practices, continue to strengthen the long-term outlook for the agriculture equipment market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $123.6 Billion |

| Forecast Value | $201.2 Billion |

| CAGR | 5.9% |

The farm tractors segment generated USD 51.5 billion in 2025. Rising awareness regarding precision farming techniques is increasing demand for advanced planting and fertilization equipment capable of optimizing seed placement and nutrient application. Farmers are increasingly investing in specialized machinery designed to improve productivity, maximize crop performance, and support efficient resource utilization. The growing need for higher agricultural output and improved farming efficiency is expected to continue driving demand across this segment.

The manual equipment segment accounted for 49% share in 2025. Manual equipment continues to play a vital role in agricultural operations, particularly in regions where farming activities remain smaller in scale and access to advanced technologies is limited. Cost-effectiveness, ease of operation, and practical functionality continue to support demand for manual equipment. At the same time, increasing investments in automation are creating significant growth opportunities for advanced agricultural machinery, although certain farming activities still rely on conventional manual tools and equipment.

United States Agriculture Equipment Market held an 80% share and generated USD 27.4 billion in 2025. Market growth across the country is being supported by ongoing technological advancements, increased mechanization, and the wider adoption of precision farming practices. Large-scale agricultural operations continue to invest heavily in advanced machinery to improve productivity, enhance operational efficiency, and streamline farming processes. Strong emphasis on modernization, resource optimization, and high-yield farming techniques is expected to sustain equipment demand across the country throughout the forecast period.

Key participants operating in the global agriculture equipment market include John Deere, Mahindra & Mahindra, Kubota, CNH Industrial, CLAAS, AGCO, Yanmar Holdings, Zoomlion Heavy Industry, Escorts Kubota, TAFE, YTO Group, International Tractors, Lovol, Stara, Lindsay, Topcon Agriculture, Carbon Robotics, Naio Technologies, Energreen, Oxbo, and XAG. Companies operating in the agriculture equipment market are focusing on product innovation, automation, and precision farming technologies to strengthen their competitive position and expand market presence. Manufacturers are investing heavily in research and development to introduce intelligent machinery equipped with advanced monitoring, automation, and connectivity features. Strategic partnerships with technology providers are helping companies enhance digital farming capabilities and deliver integrated solutions to agricultural producers. Market participants are also expanding manufacturing facilities and distribution networks to improve product accessibility across key agricultural regions. In addition, businesses are emphasizing sustainability by developing equipment that improves fuel efficiency, reduces emissions, and supports environmentally responsible farming practices.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Machinery

- 2.2.3 Power

- 2.2.4 Technology

- 2.2.5 Application

- 2.2.6 Distribution channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Supply chain analysis

- 3.2.1 Key input materials

- 3.2.2 Manufacturing hubs & sourcing patterns by region

- 3.2.3 Supply chain vulnerabilities & risk mitigation

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.3.3 Opportunities

- 3.4 Growth potential analysis

- 3.5 Price trends

- 3.5.1 Historical price trend analysis

- 3.5.2 Pricing strategy by player type

- 3.6 Regulatory framework

- 3.6.1 Global Emissions & Safety Standards (EPA Tier 4, EU Stage V, China Stage III/IV)

- 3.6.2 North America Regulatory Framework

- 3.6.3 Europe Regulatory Framework (EU Green Deal, Farm to Fork Impact)

- 3.6.4 Asia Pacific: China & India Regulatory Framework & Subsidy Programs

- 3.6.5 Trade Policy, Tariffs & Import/Export Regulations

- 3.7 Porter's five forces analysis

- 3.8 PESTEL analysis

- 3.9 Trade data analysis (based on paid database) (HS Code: 8432)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-driven disruption of traditional business models

- 3.10.2 GenAI use cases & adoption roadmap by customer segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Future market trends

- 3.12 Technology and innovation landscape

- 3.12.1 Current technological trends

- 3.12.2 Emerging technologies

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Machinery, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Farm tractors

- 5.2.1 Sub-compact & garden tractors

- 5.2.2 Compact tractors

- 5.2.3 Utility tractors

- 5.2.4 Row crop tractors

- 5.2.5 Orchard & vineyard tractors

- 5.2.6 High-power & 4WD tractors

- 5.2.7 Others (track / crawler tractors etc.)

- 5.3 Harvesting machinery

- 5.3.1 Combine harvester

- 5.3.2 Forage harvester

- 5.3.3 Thresher

- 5.3.4 Reaper

- 5.4 Plowing and cultivation machinery

- 5.4.1 Ploughs

- 5.4.2 Harrows

- 5.4.3 Cultivators & tillers

- 5.5 Planting and fertilizing machinery

- 5.5.1 Seed drills

- 5.5.2 Planters

- 5.5.3 Spreaders

- 5.5.4 Sprayers

- 5.6 Haying machinery

- 5.6.1 Balers

- 5.6.2 Mower-conditioner

- 5.6.3 Tedders & rakes

- 5.7 Others (irrigation machinery, post-harvest equipment etc.)

Chapter 6 Market Estimates & Forecast, By Power, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 < 30 HP

- 6.3 31 - 100 HP

- 6.4 101 - 200 HP

- 6.5 > 200 HP

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Manual

- 7.3 Semi-automated

- 7.4 Fully automated

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Row crops

- 8.3 Fruit & vegetables

- 8.4 Vineyards & orchards

- 8.5 Livestock farming

- 8.6 Forestry

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 AGCO

- 11.1.2 CLAAS

- 11.1.3 CNH Industrial

- 11.1.4 John Deere

- 11.1.5 Kubota

- 11.1.6 Mahindra & Mahindra

- 11.1.7 Yanmar Holdings

- 11.2 Regional Players

- 11.2.1 Escorts Kubota

- 11.2.2 International Tractors

- 11.2.3 Lovol

- 11.2.4 Stara

- 11.2.5 TAFE

- 11.2.6 YTO Group

- 11.2.7 Zoomlion Heavy Industry

- 11.3 Emerging/Niche Specialists

- 11.3.1 Carbon Robotics

- 11.3.2 Energreen

- 11.3.3 Lindsay

- 11.3.4 Naio Technologies

- 11.3.5 Oxbo

- 11.3.6 Topcon Agriculture

- 11.3.7 XAG