PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071403

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071403

Automotive Over-the-Air Testing System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

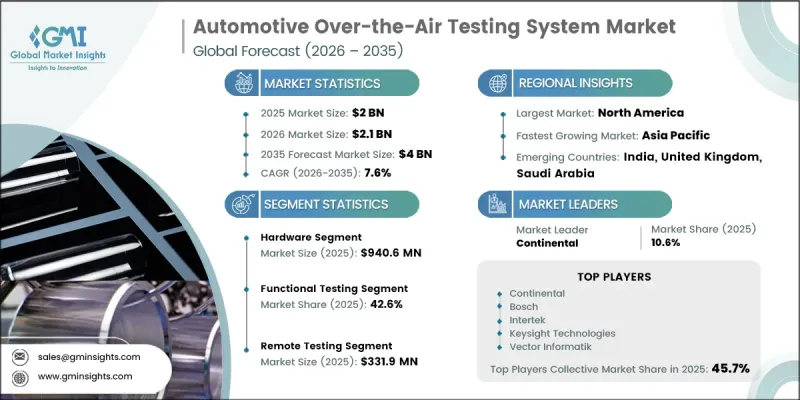

The Global Automotive Over-The-Air Testing System Market was valued at USD 2 billion in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 4 billion by 2035.

Growth is driven by the rising complexity of connected vehicle ecosystems, the expansion of electric vehicle software stacks, and increasing regulatory emphasis on cybersecurity and update integrity. Modern vehicles rely heavily on software systems controlling battery performance, thermal regulation, regenerative braking, charging coordination, and powertrain optimization, which significantly increases the need for robust validation frameworks. As automotive architectures evolve toward centralized domain controllers and zonal computing systems, individual computing units manage higher software loads and interdependencies, requiring advanced testing environments capable of simulating real-world vehicle conditions. This has accelerated adoption of hardware-in-the-loop (HIL), software-in-the-loop (SIL), and cloud-based orchestration platforms that collectively validate software updates across large vehicle fleets. A complete OTA testing ecosystem typically integrates RF chambers, network emulation systems, cybersecurity validation tools, simulation software, and compliance reporting frameworks to ensure safe and reliable deployment.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2 Billion |

| Forecast Value | $4 Billion |

| CAGR | 7.6% |

The hardware segment generated USD 940.6 million in 2025, accounting for 47.4% share, and is projected to reach USD 1.75 billion by 2035, growing at a CAGR of 6.8%. Hardware demand includes anechoic and semi-anechoic chambers, HIL testing benches, network simulation systems, spectrum analyzers, and cellular protocol testing platforms designed to evaluate OTA communication performance and antenna behavior under varied conditions. Growth in this segment is relatively moderate due to the presence of established infrastructure in several mature markets, although ongoing upgrades are required to support evolving communication standards such as 5G Sub-6 GHz and mmWave, as well as multi-antenna vehicle configurations.

The functional testing segment captured USD 846.6 million in 2025, representing 42.6% share. This segment focuses on validating update installation, execution accuracy, rollback mechanisms, ECU interoperability, and system stability across connected vehicle platforms. Functional validation platforms such as NI VeriStand and ETAS ISOLAR are widely used for integrating HIL workflows and ensuring software reliability across complex automotive architectures.

North America Automotive Over-The-Air Testing System Market reached USD 852.2 million in 2025, representing 42.9% share. This leadership is supported by strong connected vehicle penetration, stringent cybersecurity frameworks, and widespread OTA deployment across leading automotive platforms in the region.

Major players operating in the global automotive over-the-air testing system market include Rohde & Schwarz, Keysight Technologies, Anritsu, NI (Emerson Test & Measurement), Vector Informatik, dSPACE GmbH, ETS-Lindgren, Microwave Vision (MVG), DEKRA, and TUV SUD. Companies in the automotive over-the-air (OTA) testing system market are strengthening their position by expanding cloud-native testing platforms that enable scalable, remote validation of software updates across large vehicle fleets. They are investing heavily in AI-driven simulation environments to improve predictive testing accuracy and reduce validation cycles. Strategic partnerships with automakers and Tier-1 suppliers are increasing to integrate testing systems directly into vehicle development pipelines. Firms are also enhancing cybersecurity testing capabilities to address growing regulatory requirements around secure software deployment. Continuous upgrades to hardware-in-the-loop and software-in-the-loop systems support compatibility with evolving vehicle architectures.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Testing Method

- 2.2.4 Offering

- 2.2.5 Application

- 2.2.6 Vehicle

- 2.2.7 End User

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component suppliers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Service providers

- 3.1.1.5 Distribution channel

- 3.1.1.6 End Use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing Adoption of Connected Vehicles

- 3.2.1.2 Rapid Growth of Electric Vehicles (EVs)

- 3.2.1.3 Stringent Vehicle Cybersecurity and Software Compliance Regulations

- 3.2.1.4 Rising Complexity of Vehicle Software Ecosystems

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Cost and Complexity of Testing Infrastructure

- 3.2.2.2 Fragmented Vehicle Architectures and ECU Diversity

- 3.2.3 Market opportunities

- 3.2.3.1 Cloud-Based Remote Testing Infrastructure

- 3.2.3.2 AI-Augmented Test Coverage Optimization

- 3.2.3.3 5G and C-V2X Network Simulation

- 3.2.3.4 Cybersecurity Certification Services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.5.1.2 American National Standards Institute (ANSI)

- 3.5.2 Europe

- 3.5.2.1 Vehicle Certification Agency (VCA)

- 3.5.2.2 Centre National de Reception des Vehicules (CNRV)

- 3.5.2.3 UTAC CERAM

- 3.5.3 Asia-Pacific

- 3.5.3.1 Ministry of Industry and Information Technology (MIIT)

- 3.5.3.2 State Administration for Market Regulation (SAMR)

- 3.5.3.3 China Automotive Technology and Research Center (CATARC)

- 3.5.4 Latin America

- 3.5.4.1 Secretaria Nacional de Transito (SENATRAN)

- 3.5.4.2 Instituto Nacional de Metrologia, Qualidade e Tecnologia (Inmetro)

- 3.5.5 Middle East & Africa

- 3.5.5.1 National Regulator for Compulsory Specifications (NRCS)

- 3.5.5.2 Gulf Standardization Organization (GSO)

- 3.5.1 North America

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 Automated design optimization

- 3.10.3 Supply chain AI for demand forecasting

- 3.10.4 GenAI use cases & adoption roadmap by segment

- 3.10.5 Risks, Limitations & Regulatory Considerations

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.12.1 Base Case - key macro & industry variables driving CAGR

- 3.12.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.12.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

- 4.5 Company tier benchmarking

- 4.5.1 Tier classification criteria & qualifying thresholds

- 4.5.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Testing Method, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Field Testing

- 6.3 Lab Testing

- 6.4 Remote Testing

Chapter 7 Market Estimates & Forecast, By Offering, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Functional Testing

- 7.3 Security Testing

- 7.4 Compatibility Testing

- 7.5 Performance Testing

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Software Updates

- 8.3 Security Patches

- 8.4 Diagnostic Testing

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Passenger Vehicles

- 9.2.1 SUV

- 9.2.2 Sedan

- 9.2.3 Hatchback

- 9.3 Commercial Vehicles

- 9.3.1 LCV

- 9.3.2 MCV

- 9.3.3 HCV

Chapter 10 Market Estimates & Forecast, By End User, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 Automotive OEMs

- 10.3 Telecommunication Companies

- 10.4 Automotive Service Providers

- 10.5 Research & Development Institutes

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 11.1 North America

- 11.1.1 US

- 11.1.2 Canada

- 11.2 Europe

- 11.2.1 UK

- 11.2.2 Germany

- 11.2.3 France

- 11.2.4 Italy

- 11.2.5 Spain

- 11.2.6 Belgium

- 11.2.7 Netherlands

- 11.2.8 Sweden

- 11.2.9 Russia

- 11.3 Asia Pacific

- 11.3.1 China

- 11.3.2 India

- 11.3.3 Japan

- 11.3.4 Australia

- 11.3.5 Singapore

- 11.3.6 South Korea

- 11.3.7 Vietnam

- 11.3.8 Indonesia

- 11.3.9 Thailand

- 11.4 Latin America

- 11.4.1 Brazil

- 11.4.2 Mexico

- 11.4.3 Argentina

- 11.5 MEA

- 11.5.1 South Africa

- 11.5.2 Saudi Arabia

- 11.5.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Bosch

- 12.1.2 Continental

- 12.1.3 Vector Informatik

- 12.1.4 ETAS

- 12.1.5 Keysight

- 12.1.6 dSPACE

- 12.1.7 Intertek

- 12.1.8 Rohde & Schwarz

- 12.1.9 Anritsu

- 12.1.10 Spirent Communications

- 12.2 Regional Players

- 12.2.1 NI (Emerson Test & Measurement)

- 12.2.2 ETS-Lindgren

- 12.2.3 Microwave Vision

- 12.2.4 DEKRA

- 12.2.5 TUV SUD

- 12.2.6 S.E.A. Datentechnik

- 12.2.7 Bluetest

- 12.2.8 SGS

- 12.2.9 TOYO

- 12.2.10 RanLOS