PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083254

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083254

Air Hoses Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

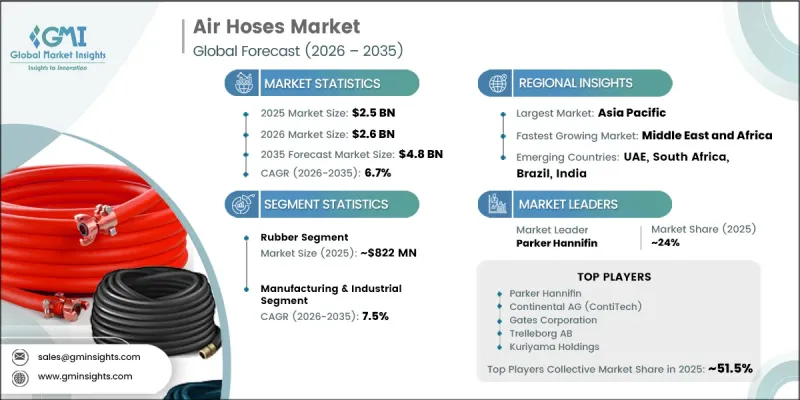

The Global Air Hoses Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 4.8 billion by 2035.

The air hoses market is experiencing steady and sustained growth driven by the expansion of industrial operations and the increasing reliance on compressed air systems across multiple end-use sectors. Growing adoption of pneumatic tools and equipment in manufacturing, automotive, construction, mining, and maintenance applications is reinforcing demand for durable and high-performance air hose solutions. Automation in production environments is further strengthening market growth, as compressed air distribution systems remain essential for powering pneumatic machinery and assembly operations. The rise of robotics and advanced manufacturing technologies has significantly increased the need for efficient air delivery infrastructure, directly supporting air hose consumption. In addition, ongoing investments in industrial infrastructure and facility expansion are contributing to higher compressor installations, which further drives demand for air hoses. As industries continue to modernize and integrate automation into core operations, the air hoses market is expected to maintain stable long-term growth supported by efficiency requirements and industrial productivity improvements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $4.8 Billion |

| CAGR | 6.7% |

The rubber segment generated USD 822 million in 2025 and is projected to grow at a CAGR of 5.7% through 2035, owing to its strong durability, flexibility, and cost-effectiveness across industrial applications. Its ability to withstand high-pressure conditions, resist abrasion, and maintain performance under demanding operating environments makes it highly suitable for use in manufacturing plants, construction activities, and mining operations. In addition, rubber hoses offer reliable performance across varying temperature conditions, enabling consistent functionality across different geographic regions and industrial settings.

The manufacturing and industrial segment accounted for 33.6% share in 2025 and is expected to grow at a CAGR of 7.5% through 2035. This segment leads the market because compressed air systems are a fundamental utility across most production facilities. Air hoses are extensively used in pneumatic tools, automated machinery, assembly lines, and material handling systems, making them an essential component of modern industrial operations. Increasing adoption of automation, smart manufacturing systems, and high-efficiency production technologies is further driving demand for reliable air distribution solutions across industrial environments.

North America Air Hoses Market held 28.5% share in 2025, supported by its advanced industrial base and high level of automation across key sectors. The region continues to demonstrate strong demand across manufacturing, automotive, aerospace, oil and gas, and construction industries, where pneumatic systems play a vital operational role. Air hoses are widely used in maintenance activities and heavy-duty industrial applications that require high reliability and safety performance. Ongoing modernization of manufacturing facilities and replacement of outdated pneumatic systems continue to support steady market growth across the region.

Major companies operating in the global air hoses market include Festo SE & Co. KG, Eaton Corporation, Trelleborg AB, Gates Corporation, Parker Hannifin Corporation, Kuriyama Holdings Corporation, Alfagomma S.p.A., Continental AG (ContiTech), SMC Corporation, Novaflex Group, Milton Industries Inc., Semperit AG, Dixon Valve & Coupling Company, Toyox Co., Ltd., Prevost SAS, Legacy Manufacturing Co. (Flexzilla(R)), Kanaflex Corporation, Sumitomo Riko Hosetex, Ltd., Coilhose Pneumatics, Nitta Corporation, Teknor Apex (Apex Hose Division), and Dayco. Companies operating in the air hoses market are strengthening their competitive position by investing in advanced material technologies, high-performance elastomer development, and enhanced product durability to meet demanding industrial requirements. Many manufacturers are expanding their production capacities and optimizing supply chains to support rising global demand. Strategic partnerships with industrial equipment providers and automation solution companies are helping broaden application reach and improve market penetration. Businesses are also focusing on product innovation, including lightweight designs, higher pressure resistance, and improved flexibility to enhance operational efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Region

- 2.2.2 Material Type

- 2.2.3 Pressure Rating

- 2.2.4 Pricing Range

- 2.2.5 Diameter

- 2.2.6 Reinforcement Type

- 2.2.7 End-user Industry

- 2.2.8 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Accelerating industrial automation & robotics integration driving pneumatic component demand

- 3.2.1.2 Rising global manufacturing infrastructure investment

- 3.2.1.3 Stringent workplace safety regulations mandating high-performance hose assemblies

- 3.2.1.4 Growing adoption of air-powered tools in automotive & construction sectors

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High volatility in raw material costs (rubber, polymers, steel wire) squeezing margins

- 3.2.2.2 Threat of substitution from all-electric & battery-powered tools

- 3.2.2.3 Long product lifecycles & high durability elongating replacement cycles

- 3.2.3 Opportunities

- 3.2.3.1 Growing demand for smart & IoT-enabled air hoses with embedded pressure sensors

- 3.2.3.2 Rising preference for eco-friendly, recyclable & PVC-free hose materials

- 3.2.3.3 Expanding e-commerce & online distribution channels for direct-to-consumer reach

- 3.2.3.4 Untapped demand in agriculture & food processing sectors in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Supply Chain Analysis

- 3.4.1 Raw material sourcing & price volatility (rubber, polymers, steel)

- 3.4.2 Manufacturing concentration & outsourcing trends

- 3.4.3 Supply chain disruption risk assessment

- 3.5 Future market trends

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade data analysis (HS Code - 4009.12)

- 3.8.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.8.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-Driven Disruption of Existing Business Models

- 3.9.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.9.3 Risks, Limitations & Regulatory Considerations

- 3.10 Pricing Analysis

- 3.11 Historical Price Trend Analysis (Driven by Primary Research)

- 3.12 Pricing Strategy by Player Type (Premium / Value / Cost-plus) (Driven by Primary Research)

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Material Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key Trends

- 5.2 Rubber Air Hoses

- 5.2.1 EPDM Rubber

- 5.2.2 SBR Rubber

- 5.2.3 NBR (Nitrile) Rubber

- 5.3 PVC Air Hoses

- 5.3.1 Standard PVC

- 5.3.2 Reinforced PVC

- 5.4 Polyurethane (PU) Air Hoses

- 5.4.1 Standard PU

- 5.4.2 Premium PU (Coiled / Retractable)

- 5.5 Hybrid Air Hoses

- 5.6 Others (Silicone, TPE, Specialty Composites)

Chapter 6 Market Estimates & Forecast, By Pressure Rating, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key Trends

- 6.2 Low Pressure (Up to 10 bar)

- 6.3 Medium Pressure (10-20 bar)

- 6.4 High Pressure (Above 20 bar)

Chapter 7 Market Estimates & Forecast, By Price Range, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key Trends

- 7.2 Economy

- 7.3 Mid-Range

- 7.4 Premium

Chapter 8 Market Estimates & Forecast, By Diameter, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key Trends

- 8.2 Less than 1/4 inch

- 8.3 1/4 inch to 1/2 inch

- 8.4 1/2 inch to 1 inch

- 8.5 Greater than 1 inch

Chapter 9 Market Estimates & Forecast, By Reinforcement Type, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key Trends

- 9.2 Single Layer (Unreinforced)

- 9.3 Double Layer / Braided

- 9.4 Spiral / Wire Reinforced

Chapter 10 Market Estimates & Forecast, By End-user Industry, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key Trends

- 10.2 Manufacturing & Industrial

- 10.2.1 General Manufacturing & Assembly Lines

- 10.2.2 Electronics & Semiconductor Assembly

- 10.2.3 Textile & Apparel Manufacturing

- 10.3 Automotive

- 10.3.1 OEM Assembly Plants

- 10.3.2 Aftermarket Repair Workshops

- 10.4 Construction

- 10.4.1 Residential Construction

- 10.4.2 Commercial & Infrastructure Projects

- 10.5 Oil & Gas

- 10.5.1 Upstream (Exploration & Drilling)

- 10.5.2 Downstream (Refining & Processing)

- 10.6 Mining

- 10.7 Agriculture

- 10.8 Food & Beverage

- 10.9 Others (Marine, Aerospace, Chemical Processing)

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 11.1 Key Trends

- 11.2 Industrial Distributors / Direct Sales

- 11.2.1 OEM Bundling & Key Account Sales

- 11.2.2 MRO (Maintenance, Repair & Operations) Procurement

- 11.3 Retail (Offline)

- 11.3.1 Hardware & Home Improvement Stores

- 11.3.2 Specialty Tool & Equipment Retailers

- 11.3.3 Automotive Aftermarket Chains

- 11.4 E-Commerce (Online)

- 11.4.1 Third-Party Marketplaces (Amazon, Alibaba, Indiamart)

- 11.4.2 Manufacturer (Direct-to-Consumer Digital Platforms)

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 12.1 Key Trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 France

- 12.3.3 UK

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 Japan

- 12.4.3 India

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 Saudi Arabia

- 12.6.2 UAE

- 12.6.3 South Africa

Chapter 13 Company Profiles

- 13.1 Parker Hannifin Corporation

- 13.2 Gates Corporation

- 13.3 Continental AG (ContiTech)

- 13.4 Trelleborg AB

- 13.5 Kuriyama Holdings Corporation

- 13.6 Coilhose Pneumatics

- 13.7 Legacy Manufacturing Co. (Flexzilla®)

- 13.8 Prevost SAS

- 13.9 Milton Industries Inc.

- 13.10 Semperit AG

- 13.11 Toyox Co., Ltd.

- 13.12 Novaflex Group

- 13.13 Alfagomma S.p.A.

- 13.14 Festo SE & Co. KG

- 13.15 SMC Corporation

- 13.16 Sumitomo Riko Hosetex, Ltd.

- 13.17 Dayco

- 13.18 Eaton Corporation

- 13.19 Dixon Valve & Coupling Company

- 13.20 Teknor Apex (Apex Hose Division)

- 13.21 Kanaflex Corporation

- 13.22 Nitta Corporation