PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083302

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083302

Pet Monoclonal Antibodies Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

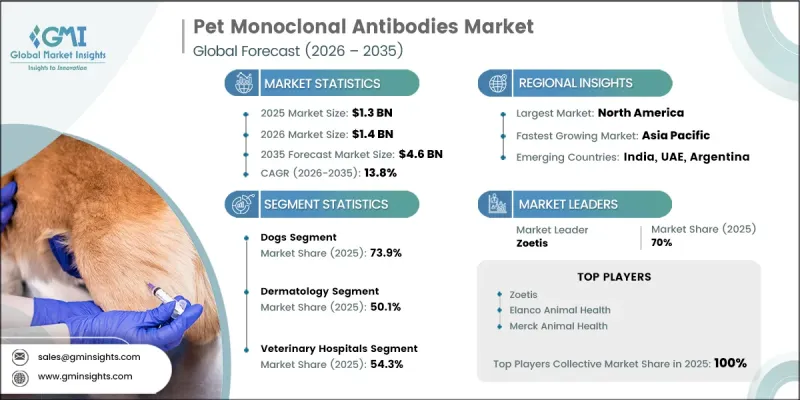

The Global Pet Monoclonal Antibodies Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 13.8% to reach USD 4.6 billion by 2035.

Growth in the pet monoclonal antibodies market is driven by the transition from conventional anti-inflammatory and pain management treatments toward targeted monoclonal antibody-based therapies for chronic animal health conditions. Rising prevalence of long-term disorders in companion animals, including dermatological and musculoskeletal diseases, is creating a stable and recurring demand base for biologic treatments. These conditions typically require continuous disease management rather than short-term intervention, supporting sustained prescription volumes. The commercialization of approved biologic therapies has further strengthened market expansion, while ongoing clinical development programs are broadening potential therapeutic applications in oncology and infectious disease areas. Increasing pet ownership, higher willingness among pet owners to spend on advanced veterinary care, and improved access to specialized veterinary services are also reinforcing market growth. Additionally, expanding veterinary healthcare infrastructure and rising adoption of advanced diagnostic and treatment protocols are contributing to stronger uptake of monoclonal antibody therapies. Overall, the market reflects a structural transformation in veterinary care toward high-precision, long-duration biologic treatment solutions that improve clinical outcomes and quality of life for companion animals.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $4.6 Billion |

| CAGR | 13.8% |

The dogs segment accounted for 73.9% share in 2025. This dominance is attributed to the strong clinical adoption of monoclonal antibody therapies for canine chronic conditions, particularly dermatological and pain-related disorders. Dogs represent the most established patient base for biologic veterinary treatments, supported by widespread clinical usage and strong treatment outcomes in long-term disease management. The segment continues to benefit from increasing awareness among pet owners regarding advanced therapeutic options and improved veterinary diagnostics that enable early disease detection and intervention.

The veterinary hospitals segment held a 54.3% share in 2025. This dominance is driven by the requirement for professional administration of monoclonal antibody therapies, which are typically delivered through clinical settings by trained veterinary specialists. Veterinary hospitals are equipped with the necessary infrastructure for biologic storage, controlled handling, and patient monitoring, making them the primary distribution and administration channel. The increasing integration of advanced treatment protocols within veterinary healthcare facilities continues to support strong demand in this segment, alongside rising adoption of specialty care services for chronic pet conditions.

North America Pet Monoclonal Antibodies Market held a 42.8% share in 2025. The region's leadership is supported by advanced veterinary healthcare systems, high expenditure on companion animal care, and early adoption of biologic therapies. Strong regulatory support for veterinary monoclonal antibody approvals has enabled faster commercialization and widespread clinical use across the region. The presence of well-established veterinary networks and growing awareness among pet owners regarding advanced treatment options further strengthens regional market dominance.

Major companies operating in the Global Pet Monoclonal Antibodies Market include Zoetis Inc., Elanco Animal Health, Merck & Co., Inc. (Merck Animal Health), Dechra Pharmaceuticals PLC, Vetigenics Inc., Akston Biosciences Corporation, MabGenesis LLC, and VETmAb Biosciences Ltd. Companies in the Pet Monoclonal Antibodies Market are focusing on expanding their biologic drug pipelines through intensive research and development aimed at addressing a wider range of chronic and complex animal diseases. Strategic collaborations with veterinary clinics, research institutions, and biotechnology firms are being leveraged to accelerate product development and clinical validation. Firms are investing in advanced antibody engineering platforms to improve treatment efficacy, safety, and species-specific targeting. Expansion of manufacturing capabilities and cold-chain distribution infrastructure is also being prioritized to support growing demand. In addition, companies are strengthening regulatory engagement strategies to streamline approval timelines across key global markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.1.1 Business trends

- 2.1.2 Animal trends

- 2.1.3 Application trends

- 2.1.4 End use trends

- 2.1.5 Regional trends

- 2.2 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic disease in pets

- 3.2.1.2 Growing advancement in targeted therapies

- 3.2.1.3 Increasing R&D investment and activities

- 3.2.1.4 Growing pet ownership and spending

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Adverse effects of the treatment

- 3.2.2.2 Regulatory challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into novel therapeutic indications

- 3.2.3.2 Development of novel administration routes

- 3.2.3.3 Shift in companion animal pharma economics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing trend analysis (Driven by primary research)

- 3.5.1 Pricing analysis, by product

- 3.5.2 Historic pricing analysis

- 3.6 Regulatory landscape (Driven by primary research)

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pipeline analysis (Driven by primary research)

- 3.10 Future market trends

- 3.11 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.12 Investment & funding analysis (Driven by primary research)

- 3.13 Pet statistics, by country (Driven by primary research)

- 3.14 Safety and tolerability considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis (Driven by primary research)

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Animal, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Dogs

- 5.3 Cats

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Dermatology

- 6.3 Osteoarthritis

- 6.4 Cancer

- 6.5 Infectious diseases

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Veterinary hospitals

- 7.3 Veterinary clinics

- 7.4 Academics and research institutes

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 UK

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Commercialized players

- 9.1.1 Zoetis Inc.

- 9.1.2 Merck Animal Health

- 9.1.3 Elanco Animal Health

- 9.2 Emerging/pipeline players

- 9.2.1 Vetigenics

- 9.2.2 Akston Biosciences

- 9.2.3 MabGenesis

- 9.2.4 Dechra Pharmaceuticals

- 9.2.5 VETmAb Biosciences