PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083323

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083323

Caps and Closures Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

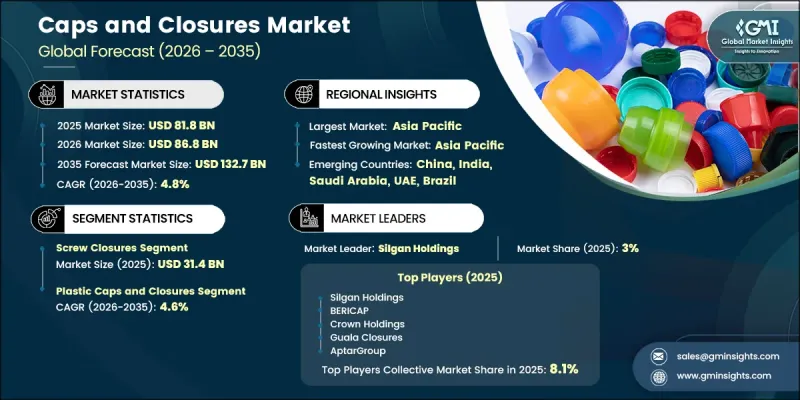

The Global Caps and Closures Market was valued at USD 81.8 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 132.7 billion by 2035.

The industry is undergoing a clear structural transition from basic commodity sealing products toward highly engineered closure systems designed for specific end-use requirements. This evolution is creating a dual-track growth pattern, where standardized closure formats in price-sensitive markets face margin pressure, while advanced solutions such as dispensing closures, child-resistant pharmaceutical formats, and smart or functional caps are generating higher value realization. Growth is further reinforced by expanding global beverage consumption, driven by urban population growth, higher disposable incomes, and increasing diversification in product categories such as functional drinks and premium packaged beverages. The pharmaceutical sector is also strengthening structural demand for tamper-evident, safety-compliant, and precision dosing closure systems. At the same time, sustainability requirements and regulatory pressure are encouraging innovation in lightweight materials, recyclability, and reduced plastic usage, shaping long-term product development strategies across the industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $81.8 Billion |

| Forecast Value | $132.7 Billion |

| CAGR | 4.8% |

The screw closures segment reached USD 31.4 billion in 2025, accounting for 38% share. This segment is expected to grow at a CAGR of 5.2%, outperforming the overall market average due to its widespread application across bottled beverages, packaged liquids, and food products. Demand expansion across high-volume consumer categories in emerging economies continues to reinforce its dominant position, particularly where cost efficiency and reliability remain key purchasing factors.

The plastic-based caps and closures segment held 79% share, equivalent to USD 65.1 billion in 2025, and is projected to grow at a CAGR of 4.6% through 2035. Polypropylene continues to serve as the primary material due to its durability, chemical resistance, ease of processing, and suitability for large-scale injection molding operations. A major ongoing shift within this segment is the industry-wide adaptation to regulatory requirements for tethered caps and increased incorporation of recycled polymer content, driving continuous material innovation and redesign of closure structures.

North America Caps and Closures Market was valued at USD 16.1 billion in 2025, accounting for 20% share, and is expected to grow at a CAGR of 4.5% through 2035. The United States remains the primary contributor to regional demand, supported by strong consumption across packaged beverages, bottled water, and premium functional drinks, along with consistent pharmaceutical packaging requirements for safety-compliant closures. The regional supply landscape is supported by established manufacturers such as Silgan Holdings and Closure Systems International (CSI), which operate extensive production networks across multiple U.S. manufacturing locations serving food, beverage, and healthcare customers.

Key players operating in the global caps and closures industry include Amcor, AptarGroup, BERICAP, Closure Systems International (CSI), Crown Holdings, Guala Closures, Silgan Holdings, HERTI JSC, MRP Solutions, Nippon Closures, Pact Group, Pelliconi, Tecnocap, UNITED CAPS, Alcopack, Blackhawk Molding, Caprite Australia, JSD Pharma, PHOENIX Packaging, SRS Packaging, and UAB Elmoris. Companies in the caps and closures market are strengthening their position by investing in advanced closure technologies that improve functionality, safety, and user convenience. Manufacturers are increasingly focusing on developing dispensing systems, tamper-evident designs, and child-resistant solutions tailored for pharmaceutical and premium beverage applications. Sustainability has become a central strategy, with firms integrating recycled plastics, lightweight designs, and circular packaging models to meet regulatory and consumer expectations. Strategic expansion of production capacity in high-growth regions is also helping companies improve supply chain efficiency and reduce lead times.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Material type

- 2.2.4 Closure size

- 2.2.5 End use industry

- 2.2.6 Distribution channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Price trends

- 3.4.1 Historical price trend analysis

- 3.4.2 Pricing strategy by player type

- 3.5 Regulatory framework

- 3.5.1 North America: US FDA packaging regulations & Canada Health packaging standards

- 3.5.2 Europe: EU packaging & packaging waste directive (PPWD), tethered cap mandates (SUP directive)

- 3.5.3 China: GB standards & NMPA packaging regulations

- 3.5.4 India: BIS standards & FSSAI packaging compliance

- 3.5.5 Japan: JIS standards & Ministry of Health closure regulations

- 3.5.6 ASEAN countries: harmonized packaging & food safety directives

- 3.5.7 Australia & New Zealand: FSANZ & TGA closure compliance

- 3.5.8 Latin America: ANVISA (Brazil) & ANMAT (Argentina) packaging regulations

- 3.5.9 Middle East & Africa: GCC standardization organization & regional food authority mandates

- 3.6 Porter's five forces analysis

- 3.7 PESTEL analysis

- 3.8 Trade Data Analysis (Based on Paid Database) (HS Code: 3923)

- 3.8.1 Import/export volume & value trends

- 3.8.2 Key trade corridors & tariff impact

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of traditional business models

- 3.9.2 GenAI use cases & adoption roadmap by customer segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Future market trends

- 3.11 Technology and innovation landscape

- 3.11.1 Current technological trends

- 3.11.2 Emerging technologies

- 3.12 Consumer behavior analysis

- 3.12.1 Purchasing patterns

- 3.12.2 Preference analysis

- 3.12.3 Regional variations in consumer behavior

- 3.12.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035 ($Billion, Million Units)

- 5.1 Key trends

- 5.2 Screw closures

- 5.2.1 Continuous thread (CT) caps

- 5.2.2 Lug & twist caps

- 5.2.3 Roll-on pilfer proof (ROPP) caps

- 5.2.4 Linerless & conical caps

- 5.3 Dispensing closures

- 5.3.1 Flip-top & snap-top caps

- 5.3.2 Push-pull caps

- 5.3.3 Disc-top caps

- 5.3.4 Pump & spray dispensers

- 5.3.5 Drop counter & dropper caps

- 5.4 Tamper-evident closures

- 5.4.1 Break-band closures

- 5.4.2 Shrink sleeve closures

- 5.4.3 Tear-off strip closures

- 5.5 Child-resistant closures (CRC)

- 5.5.1 Push-and-turn CRC

- 5.5.2 Squeeze-and-turn CRC

- 5.5.3 Senior-friendly CRC

- 5.6 Crown closures

- 5.6.1 Standard crown caps

- 5.6.2 Twist-off crown caps

- 5.6.3 Aerosol closures

- 5.6.4 Actuator caps

- 5.6.5 Overcaps

- 5.7 Others (snap-on & press-on caps, venting caps etc.)

Chapter 6 Market Estimates & Forecast, By Material Type, 2022 - 2035 ($Billion, Million Units)

- 6.1 Key trends

- 6.2 Plastic caps & closures

- 6.2.1 Polypropylene (PP)

- 6.2.2 Polyethylene (PE)

- 6.2.3 High-density polyethylene (HDPE)

- 6.2.4 Low-density polyethylene (LDPE)

- 6.2.5 Polyethylene terephthalate (PET)

- 6.2.6 Others (bio-based & sustainable plastics etc.)

- 6.3 Metal caps & closures

- 6.3.1 Aluminum

- 6.3.2 Steel & tin plate

Chapter 7 Market Estimates & Forecast, By Closure Size, 2022 - 2035 ($Billion, Million Units)

- 7.1 Key trends

- 7.2 Small (up to 20 mm)

- 7.3 Medium (21 mm - 40 mm)

- 7.4 Large (41 mm - 60 mm)

- 7.5 Extra-large (above 60 mm)

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 ($Billion, Million Units)

- 8.1 Key trends

- 8.2 Food and beverages

- 8.3 Pharmaceuticals & healthcare

- 8.4 Cosmetics & personal care

- 8.5 Household chemicals

- 8.6 Others (agricultural chemicals and industrial chemicals etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Million Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Amcor

- 11.1.2 AptarGroup

- 11.1.3 BERICAP

- 11.1.4 Closure Systems International (CSI)

- 11.1.5 Crown Holdings

- 11.1.6 Guala Closures

- 11.1.7 Silgan Holdings

- 11.2 Regional Players

- 11.2.1 HERTI JSC

- 11.2.2 MRP Solutions

- 11.2.3 Nippon Closures

- 11.2.4 Pact Group

- 11.2.5 Pelliconi

- 11.2.6 Tecnocap

- 11.2.7 UNITED CAPS

- 11.3 Emerging/Niche Specialists

- 11.3.1 Alcopack

- 11.3.2 Blackhawk Molding

- 11.3.3 Caprite Australia

- 11.3.4 JSD Pharma

- 11.3.5 PHOENIX Packaging

- 11.3.6 SRS Packaging

- 11.3.7 UAB Elmoris