PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083386

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083386

Artificial Intelligence in Medical Imaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

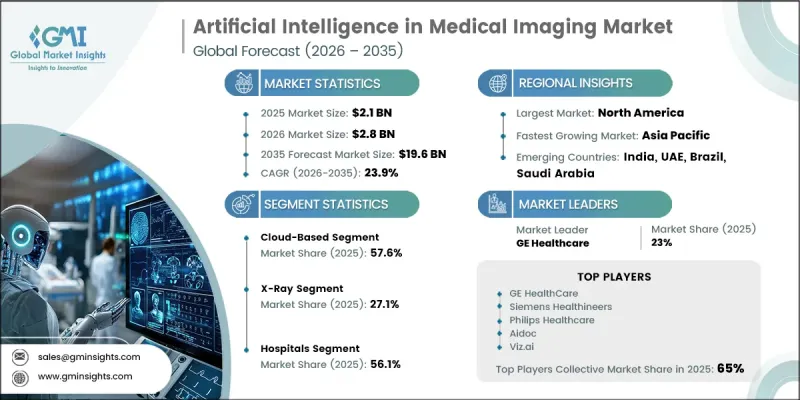

The Global AI in Medical Imaging Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 23.9% to reach USD 19.6 billion by 2035.

The market is undergoing rapid transformation as deep learning technologies become deeply embedded into clinical imaging workflows, significantly improving diagnostic accuracy and operational efficiency. AI-enabled imaging solutions are increasingly being used to support early disease identification, reduce variability in diagnostic interpretation, and enhance treatment planning across oncology, neurology, and cardiology applications. Clinical validation studies and peer-reviewed research continue to demonstrate that advanced algorithms can achieve diagnostic performance levels comparable to experienced radiologists across multiple imaging modalities. Growing regulatory acceptance of AI-based diagnostic tools is accelerating hospital adoption and expanding reimbursement pathways in major healthcare systems. In parallel, rising investments from healthcare technology providers, imaging equipment manufacturers, academic institutions, and early-stage innovators are accelerating product development cycles and broadening application areas. Public sector research support, including funding initiatives from national biomedical agencies, continues to advance innovation in imaging reconstruction, cardiac diagnostics, and multi-modal data integration. As healthcare systems prioritize precision medicine and efficiency, AI-based imaging is becoming a core component of modern diagnostic infrastructure across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.1 Billion |

| Forecast Value | $19.6 Billion |

| CAGR | 23.9% |

The cloud-based deployment segment accounted for 57.6% share in 2025. Cloud infrastructure is increasingly preferred due to its ability to support rapid algorithm deployment, scalable computing power, seamless software updates, and reduced upfront capital requirements. These advantages make cloud-based solutions especially suitable for healthcare facilities that lack large-scale on-premise computing systems, enabling broader adoption across diverse healthcare environments.

The hospital segment held a 56.1% share in 2025. Hospitals remain the primary end-use setting due to their advanced imaging infrastructure, high patient volumes, and strong institutional capacity for digital health investments. Large healthcare networks and academic medical centers are among the earliest adopters of enterprise-scale AI imaging systems, where high imaging throughput justifies the cost of integration, licensing, and workflow transformation.

North America AI in Medical Imaging Market accounted for 43.8% share in 2025, maintaining the largest regional share. The region's leadership is supported by widespread deployment of regulatory-cleared AI imaging solutions, strong hospital IT investment, and established reimbursement structures that prioritize diagnostic accuracy and operational efficiency. The United States represents most regional revenue, while Canada continues to expand adoption through national-level digital health initiatives focused on advanced clinical imaging technologies.

Major companies operating in the global AI in medical imaging market include Philips Healthcare, GE HealthCare, Siemens Healthineers, Fujifilm Holdings, Canon Medical Systems, Aidoc, Viz.ai, Qure.ai, Lunit, RapidAI, Annalise.ai, Subtle Medical, Tempus Radiology, Rad AI, and Cleerly Inc. Companies in the AI in medical imaging market are strengthening their market position through continuous advancement of AI algorithms, expansion of clinical validation studies, and integration of solutions into existing hospital imaging workflows. Many players are prioritizing partnerships with hospitals, academic institutions, and healthcare networks to accelerate real-world deployment and improve algorithm training using large-scale imaging datasets. Strategic collaborations with medical device manufacturers and cloud service providers are enabling scalable and interoperable platforms. Companies are also focusing on regulatory approvals across multiple regions to expand commercialization opportunities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definitions

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy & data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation for any one approach

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.1.1 Business trends

- 2.1.2 Deployment trends

- 2.1.3 Modality trends

- 2.1.4 Indication trends

- 2.1.5 Application trends

- 2.1.6 End use trends

- 2.1.7 Regional trends

- 2.2 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements in AI

- 3.2.1.2 Shortage of radiologists accelerating the AI adoption

- 3.2.1.3 Improved diagnostic accuracy and treatment planning

- 3.2.1.4 Rising R&D investment supporting innovation and market expansion

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Slow regulatory approval process

- 3.2.2.2 Risk of patient safety concerns due to AI-driven diagnostic errors

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of AI-enabled population screening and preventive healthcare

- 3.2.3.2 Integration of AI imaging platforms with multimodal clinical data ecosystems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing trend analysis (Driven by primary research)

- 3.6 Regulatory landscape (Driven by primary research)

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.11 Investment & funding analysis (Driven by primary research)

- 3.12 PACS integration

- 3.12.1 PACS-based AI integration into radiology systems

- 3.12.2 AI-driven workflow optimization and reporting efficiency

- 3.13 FDA-Cleared AI landscape

- 3.13.1 Expansion of FDA-cleared AI imaging solutions

- 3.13.2 Increasing approvals driving market adoption

- 3.14 Reimbursement landscape

- 3.14.1 AI reimbursement trends and adoption drivers

- 3.14.2 CMS reimbursement pathways supporting AI imaging

- 3.14.3 NTAP approvals enabling adoption in critical imaging applications

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis (Driven by primary research)

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Deployment, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Cloud-based

- 5.3 On-premises

Chapter 6 Market Estimates and Forecast, By Modality, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 X-ray

- 6.3 Computed tomography (CT)

- 6.4 Magnetic Resonance Imaging (MRI)

- 6.5 Ultrasound imaging

- 6.6 Molecular imaging

- 6.7 Nuclear imaging

- 6.8 Other modalities

Chapter 7 Market Estimates and Forecast, By Indication, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Breast imaging

- 7.3 Lung imaging

- 7.4 Neurology

- 7.5 Cardiovascular applications

- 7.6 Liver imaging

- 7.7 Orthopedics

- 7.8 Other indications

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Diagnostic decision support

- 8.3 Radiation therapy planning

- 8.4 Surgical & interventional planning

- 8.5 Longitudinal disease monitoring

- 8.6 Clinical research & trials

- 8.7 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Clinics

- 9.4 Diagnostic centers

- 9.5 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 France

- 10.3.3 UK

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 GE HealthCare

- 11.2 Siemens Healthineers

- 11.3 Philips Healthcare

- 11.4 Canon Medical Systems

- 11.5 Fujifilm Holdings

- 11.6 Aidoc

- 11.7 Viz.ai

- 11.8 RapidAI

- 11.9 Tempus Radiology

- 11.10 Lunit

- 11.11 Qure.ai

- 11.12 Annalise.ai

- 11.13 Subtle Medical

- 11.14 Rad AI

- 11.15 Cleerly