PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1942451

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1942451

Insulated Metal Panels Market by Metal Type (Steel, Aluminum, Others), Insulation Material (PIR/PUR, Polystyrene, Mineral Wool), By Application (Exterior Wall, Others), By End-use (Residential, Non-residential), and Region - Global Forecast to 2030

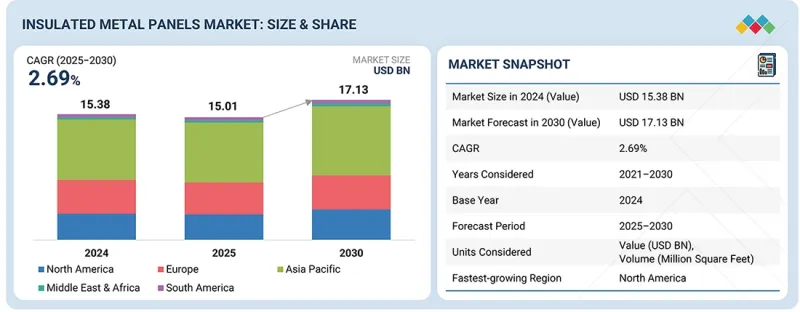

The insulated metal panels market is projected to reach USD 15.01 billion in 2025 and USD 17.13 billion by 2030, at a CAGR of 2.69% from 2025 to 2030.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) Volume (Million Square Feet) |

| Segments | Metal Type, Insulation Material, Application, End-use, and Region |

| Regions covered | North America, Asia Pacific, Europe, the Middle East & Africa, and South America |

The market will expand as high levels of urbanization increase demand for quick, efficient, and long-lasting construction technologies, particularly in commercial and industrial structures. Governments are becoming more rigorous in implementing energy-saving and thermal insulation requirements to curb carbon emissions.

"The steel segment is projected to capture the largest market share in 2030."

In 2030, the steel segment is expected to have the highest market share because of its high strength, durability, and structural reliability in building practice. It is also good in terms of fire resistance and long service life; hence it can be used in industrial and non-residential works. Steel panels are cost-effective and universally available, with well-established supply chains.

"The mineral wool segment is projected to exhibit the highest CAGR from 2025 to 2030."

The mineral wool segment is forecast to have the highest CAGR between 2025 and 2030, owing to its superior fire resistance and acoustic insulation. The growing emphasis on fire safety measures, particularly in buildings with large occupancies and on industrial premises, favors its development. It also offers strong thermal performance without compromising safety.

"The exterior walls segment is projected to capture the largest market share in 2030."

The exterior walls segment is expected to get the highest market share in 2030 because they are critical in thermal insulation and building envelope performance. Dominance is supported by increasing demand for the energy-efficient facade of commercial and industrial buildings. They are also aesthetically flexible, which further increases adoption.

"The non-residential segment is projected to have the highest CAGR from 2025 to 2030."

The non-residential segment will record the highest CAGR between 2025 and 2030, driven by increased construction of warehouses, cold storage facilities, factories, and data centers. These buildings require high thermal efficiency, durability, and rapid installation, with insulated metal panels preferred.

"The North America insulated metal panels market is projected to grow at the highest CAGR during the forecast period."

The North America insulated metal panel market is expected to have the highest CAGR over the forecast period, driven by the strong implementation of energy-efficient building codes and fire safety measures. Demand is increasing due to greater investment in cold storage, data centers, and commercial construction. The adoption of these panels is also being prompted by government incentives for net-zero and green buildings.

By Company Type: Tier 1 - 60%, Tier 2 - 20%, and Tier 3 - 20%

By Designation: C-level Executives - 33, Directors - 33%, and Others - 34%

By Region: North America - 20%, Europe - 25%, Asia Pacific - 25%, South America - 10%, and Middle East & Africa - 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: Kingspan Group (Ireland), Nucor Corporation (US), ArcelorMittal (Luxembourg), Recticel NV/SA (Belgium), and Tata Steel (India), among other companies, are covered in the report.

The study includes an in-depth competitive analysis of these key players in the insulated metal panels market, covering their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the insulated metal panels market by metal type (steel, aluminum, and other metals), insulation material (PIR/PUR, polystyrene, mineral wool, and other materials), application (interior walls, exterior walls, roofs, ceilings, and other applications), end use (residential and non-residential), and region (Asia Pacific, North America, Europe, South America, and the Middle East & Africa). The report's scope includes detailed information on the drivers, restraints, challenges, and opportunities influencing the growth of the insulated metal panels market. A detailed analysis of key industry players provides insights into their business overviews, products offered, and key strategies, such as expansions, acquisitions, product launches, partnerships, agreements, and contracts, associated with the insulated metal panels market. This report also includes a competitive analysis of upcoming startups in the insulated metal panels market.

Reasons to Buy the Report

The report will provide market leaders and new entrants with the closest available estimates of revenue for the overall insulated metal panels market and its subsegments. It will help stakeholders understand the competitive landscape, gain insights into positioning their businesses more effectively, and plan suitable go-to-market strategies. The report will also provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of key drivers (global construction scale, urbanization, and sustainability mandates), restraints (high upfront costs that limit adoption of insulated metal panels despite long-term benefits), opportunities (expanding renovation and retrofit activities), and challenges (intense competition from alternative wall systems)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the insulated metal panels market

- Market Development: Comprehensive information about profitable markets-the report analyzes the insulated metal panels market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the insulated metal panels market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as Kingspan Group (Ireland), Nucor Corporation (US), ArcelorMittal (Luxembourg), Recticel NV/SA (Belgium), Tata Steel (India), and others

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.3.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING INSULATED METAL PANELS MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: ASIA PACIFIC MARKET SIZE AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INSULATED METAL PANELS MARKET

- 3.2 INSULATED METAL PANELS MARKET, BY METAL TYPE AND REGION

- 3.3 INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL

- 3.4 INSULATED METAL PANELS MARKET, BY APPLICATION

- 3.5 INSULATED METAL PANELS MARKET, BY END USE

- 3.6 INSULATED METAL PANELS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Global construction scale, urbanization, and sustainability mandates

- 4.2.1.2 GHGs reduction & sustainability initiatives

- 4.2.1.3 Rising demand for refrigerated and processed foods

- 4.2.2 RESTRAINTS

- 4.2.2.1 High upfront costs limit adoption despite long-term benefits

- 4.2.2.2 Awareness gaps and misconceptions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expanding renovation and retrofit activities

- 4.2.4 CHALLENGES

- 4.2.4.1 Intense competition from alternative wall systems

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN INSULATED METAL PANELS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.4.2.1 Construction ↔ energy efficiency

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC ANALYSIS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 PRICING ANALYSIS

- 5.4.1.1 Pricing analysis based on region

- 5.4.1 PRICING ANALYSIS

- 5.5 TRADE ANALYSIS

- 5.5.1 IMPORT SCENARIO (HS CODE 730890)

- 5.5.2 EXPORT SCENARIO (HS CODE 730890)

- 5.6 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.7.1 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 IMPACT OF 2025 US TARIFF: INSULATED METAL PANELS MARKET

- 5.9.1 INTRODUCTION

- 5.9.2 KEY TARIFF RATES

- 5.9.3 PRICE IMPACT ANALYSIS

- 5.9.4 IMPACT ON COUNTRY/REGION

- 5.9.4.1 US

- 5.9.4.2 Asia Pacific

- 5.9.4.3 Europe

- 5.9.5 END-USE SECTOR IMPACT

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 PHASE CHANGE MATERIALS

- 6.1.2 AEROGEL INSULATION

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 PHOTOVOLTAIC (PV) SOLAR INTEGRATION

- 6.2.2 SMART BUILDING SENSORS AND IOT INTEGRATION

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 MODULAR AND PREFABRICATED CONSTRUCTION

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.4.2 MID-TERM (2027-2030) | EXPANSION & INTEGRATION

- 6.4.3 LONG-TERM (2030-2035+) | MATURITY & AUTONOMOUS SYSTEMS

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 METHODOLOGY

- 6.5.3 INSULATED METAL PANELS MARKET, PATENT ANALYSIS, 2014-2025

- 6.6 FUTURE APPLICATIONS

- 6.6.1 INTEGRATION OF INSULATED METAL PANELS IN SMART & ENERGY-EFFICIENT BUILDINGS

- 6.7 IMPACT OF AI/GEN AI ON INSULATED METAL PANELS MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN INSULATED METAL PANELS PROCESSING

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN INSULATED METAL PANELS MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN INSULATED METAL PANELS MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF INSULATED METAL PANELS

- 7.2.1.1 Carbon Impact Reduction

- 7.2.1.2 Eco-Applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF INSULATED METAL PANELS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END USE SEGMENTS

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY APPLICATION

9 INSULATED METAL PANELS MARKET, BY METAL TYPE

- 9.1 INTRODUCTION

- 9.2 STEEL

- 9.2.1 STEEL-BASED INSULATED METAL PANELS SUPPORT HIGH-LOAD, FIRE-SAFE, AND SUSTAINABLE CONSTRUCTION

- 9.3 ALUMINUM

- 9.3.1 ALUMINUM-BASED INSULATED METAL PANELS OFFER LIGHTWEIGHT DESIGN, SUPERIOR CORROSION RESISTANCE, AND SUSTAINABILITY

- 9.4 OTHER METAL TYPES

10 INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL

- 10.1 INTRODUCTION

- 10.2 POLYURETHANE (PUR)/POLYISOCYANURATE (PIR)

- 10.2.1 SUPERIOR THERMAL AND FIRE PERFORMANCE OF PIR/PUR CORES

- 10.3 MINERAL WOOL

- 10.3.1 GROWING ADOPTION OF FIRE-RATED, HIGH-STABILITY BUILDING ENVELOPES

- 10.4 POLYSTYRENE

- 10.4.1 RISING PREFERENCE FOR LIGHTWEIGHT AND ECONOMICAL INSULATION SOLUTIONS

- 10.5 OTHER INSULATION MATERIALS

11 INSULATED METAL PANELS MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 INTERIOR WALLS

- 11.2.1 ADOPTION OF MODULAR AND FAST-TRACK CONSTRUCTION SOLUTIONS

- 11.3 EXTERIOR WALLS

- 11.3.1 RISING DEMAND FOR SUSTAINABLE AND HIGH-PERFORMANCE BUILDING ENVELOPES

- 11.4 ROOFS

- 11.4.1 ADOPTION OF GREEN BUILDING AND COOL ROOF STANDARDS

- 11.5 CEILINGS

- 11.5.1 GROWTH OF COLD CHAIN, FOOD PROCESSING, AND CLEAN ROOM FACILITIES

- 11.6 OTHER APPLICATIONS

12 INSULATED METAL PANELS MARKET, BY END USE

- 12.1 INTRODUCTION

- 12.2 RESIDENTIAL

- 12.2.1 GROWTH IN URBAN HOUSING AND MULTI-FAMILY RESIDENTIAL DEVELOPMENTS

- 12.3 NON-RESIDENTIAL

- 12.3.1 EXPANSION OF COLD STORAGE, INDUSTRIAL, AND DATA-INTENSIVE FACILITIES

13 INSULATED METAL PANELS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 ASIA PACIFIC

- 13.2.1 CHINA

- 13.2.1.1 Expansion of cold chain infrastructure and sustainable logistics

- 13.2.2 JAPAN

- 13.2.2.1 Stricter energy efficiency regulations and mandatory building standards

- 13.2.3 INDIA

- 13.2.3.1 Expansion of food processing, cold chain, and Agro-logistics infrastructure

- 13.2.4 SOUTH KOREA

- 13.2.4.1 Renovation of aging building stock across residential, commercial, and industrial sectors

- 13.2.5 AUSTRALIA

- 13.2.5.1 Expansion of cold storage and temperature-controlled logistics infrastructure

- 13.2.6 REST OF ASIA PACIFIC

- 13.2.1 CHINA

- 13.3 EUROPE

- 13.3.1 UK

- 13.3.1.1 Rapid expansion of warehousing, logistics, and cold-chain infrastructure

- 13.3.2 GERMANY

- 13.3.2.1 Expansion of logistics and advanced manufacturing infrastructure

- 13.3.3 FRANCE

- 13.3.3.1 RE2020 energy and carbon regulations

- 13.3.4 ITALY

- 13.3.4.1 Expansion of agri-food, cold storage, and logistics infrastructure

- 13.3.5 SPAIN

- 13.3.5.1 Energy transition targets and large-scale renovation funding

- 13.3.6 REST OF EUROPE

- 13.3.1 UK

- 13.4 NORTH AMERICA

- 13.4.1 US

- 13.4.1.1 Expanding processed food infrastructure and energy-efficient construction

- 13.4.2 CANADA

- 13.4.2.1 Government initiatives aimed at reducing greenhouse gas emissions and improving building performance

- 13.4.3 MEXICO

- 13.4.3.1 Industrial expansion, green construction, and cold-chain growth

- 13.4.1 US

- 13.5 SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Expanding processed food infrastructure and energy-efficient construction

- 13.5.2 ARGENTINA

- 13.5.2.1 Government push for energy-efficient and low-carbon buildings

- 13.5.3 REST OF SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 GCC COUNTRIES

- 13.6.1.1 Saudi Arabia

- 13.6.1.1.1 Expanding construction industry to drive demand

- 13.6.1.2 UAE

- 13.6.1.2.1 Expansion of real estate sector to drive demand

- 13.6.1.3 Rest of GCC Countries

- 13.6.1.1 Saudi Arabia

- 13.6.2 SOUTH AFRICA

- 13.6.2.1 Public sector commitments to accelerate infrastructure rollout

- 13.6.3 REST OF MIDDLE EAST & AFRICA

- 13.6.1 GCC COUNTRIES

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS

- 14.4 MARKET SHARE ANALYSIS

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.5.1 COMPANY VALUATION

- 14.6 FINANCIAL METRICS

- 14.7 BRAND/PRODUCT COMPARISON

- 14.8 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.8.1 STARS

- 14.8.2 EMERGING LEADERS

- 14.8.3 PERVASIVE PLAYERS

- 14.8.4 PARTICIPANTS

- 14.8.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.8.5.1 Company footprint

- 14.8.5.2 Region footprint

- 14.8.5.3 Insulation type footprint

- 14.8.5.4 Metal type footprint

- 14.8.5.5 Application footprint

- 14.8.5.6 End-use footprint

- 14.9 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.9.1 PROGRESSIVE COMPANIES

- 14.9.2 RESPONSIVE COMPANIES

- 14.9.3 DYNAMIC COMPANIES

- 14.9.4 STARTING BLOCKS

- 14.9.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.9.5.1 Detailed list of key startups/SMEs

- 14.9.5.2 Competitive benchmarking of key startups/SMEs

- 14.10 COMPETITIVE SCENARIO

- 14.10.1 PRODUCT LAUNCHES

- 14.10.2 DEALS

- 14.10.3 EXPANSIONS

- 14.10.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 KINGSPAN GROUP

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.3.2 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 NUCOR CORPORATION

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.3.2 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 ARCELORMITTAL

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.3.2 Deals

- 15.1.3.3.3 Other developments

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 RECTICEL NV/SA

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 TATA STEEL

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 ISOPAN S.P.A.

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.4 MnM view

- 15.1.7 KPS GLOBAL LLC

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Expansions

- 15.1.7.4 MnM view

- 15.1.7.4.1 Key strengths

- 15.1.8 WGI WESTMAN GROUP INC.

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 MnM view

- 15.1.9 BRUCHA GMBH

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 MnM view

- 15.1.10 ASSAN PANEL A.S.

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 MnM view

- 15.1.1 KINGSPAN GROUP

- 15.2 OTHER PLAYERS

- 15.2.1 NORBEC INC.

- 15.2.2 ZAMIL STEEL HOLDING COMPANY LIMITED

- 15.2.3 LONDON ECO-METAL MANUFACTURING

- 15.2.4 BRDECO GROUP

- 15.2.5 STRUCTURAL PANELS, INC.

- 15.2.6 ADVANCED PANEL PRODUCTS LTD.

- 15.2.7 ATAS INTERNATIONAL, INC.

- 15.2.8 GREEN SPAN PROFILES

- 15.2.9 FALK BOUWSYSTEMEN B.V.

- 15.2.10 PERMATHERM

- 15.2.11 RAUTARUUKKI CORPORATION

- 15.2.12 AMERICAN INSULATED PANEL

- 15.2.13 LATTONEDIL

- 15.2.14 STRUCTALL BUILDING SYSTEMS, INC.

- 15.2.15 VULCAN STEEL STRUCTURES, INC.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.3 DATA TRIANGULATION

- 16.4 RESEARCH ASSUMPTIONS

- 16.5 RISK ASSESSMENT

- 16.6 GROWTH RATE ASSUMPTIONS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 CUSTOMIZATION OPTIONS

- 17.3 RELATED REPORTS

- 17.4 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.5 AUTHOR DETAILS

List of Tables

- TABLE 1 REGION-WISE GOALS RELATED TO SUSTAINABILITY, ENERGY-EFFICIENT STRUCTURES, AND DECARBONIZATION

- TABLE 2 PORTER'S FIVE FORCES ANALYSIS

- TABLE 3 GLOBAL GDP GROWTH PROJECTION, BY REGION, 2021-2028 (USD TRILLION)

- TABLE 4 ROLES OF COMPANIES IN INSULATED METAL PANELS ECOSYSTEM

- TABLE 2 AVERAGE SELLING PRICE OF INSULATED METAL PANELS, BY REGION, 2021-2024 (USD/SQUARE FEET)

- TABLE 3 IMPORT DATA RELATED TO HS CODE 730890-STRUCTURES AND PARTS OF STRUCTURES, OF IRON OR STEEL, N.E.S. (EXCL. BRIDGES AND BRIDGE-SECTIONS, TOWERS AND LATTICE MASTS, DOORS AND WINDOWS AND THEIR FRAMES, THRESHOLDS FOR DOORS, PROPS AND SIMILAR EQUIPMENT FOR SCAFFOLDING, SHUTTERING, PROPPING OR PIT-PROPPING), BY COUNTRY, 2020-2024 (USD BILLION)

- TABLE 4 EXPORT DATA RELATED TO HS CODE 730890-STRUCTURES AND PARTS OF STRUCTURES, OF IRON OR STEEL, N.E.S. (EXCL. BRIDGES AND BRIDGE-SECTIONS, TOWERS AND LATTICE MASTS, DOORS AND WINDOWS AND THEIR FRAMES, THRESHOLDS FOR DOORS, PROPS AND SIMILAR EQUIPMENT FOR SCAFFOLDING, SHUTTERING, PROPPING OR PIT-PROPPING), 2020-2024 (USD BILLION)

- TABLE 5 INSULATED METAL PANELS MARKET: DETAILED LIST OF CONFERENCES AND EVENTS, 2025-2026

- TABLE 6 INSULATED METAL PANELS MARKET: LIST OF KEY PATENTS, 2023-2024

- TABLE 7 TOP USE CASES AND MARKET POTENTIAL

- TABLE 8 BEST PRACTICES: COMPANIES IMPLEMENTING USE CASES

- TABLE 9 INSULATED METAL PANELS MARKET: CASE STUDIES RELATED TO GEN AI IMPLEMENTATION

- TABLE 10 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 ROW: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 GLOBAL INDUSTRY STANDARDS IN INSULATED METAL PANELS MARKET

- TABLE 15 CERTIFICATIONS, LABELING, ECO-STANDARDS IN INSULATED METAL PANELS MARKET

- TABLE 16 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY END USE (%)

- TABLE 17 KEY BUYING CRITERIA, BY END USE

- TABLE 18 UNMET NEEDS IN INSULATED METAL PANELS MARKET, BY END USE

- TABLE 19 INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 20 INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 21 INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 22 INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 23 INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 24 INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 25 INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 26 INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 27 INSULATED METAL PANELS MARKET, BY APPLICATION, 2021-2023 (USD MILLION)

- TABLE 28 INSULATED METAL PANELS MARKET, BY APPLICATION, 2024-2030 (USD MILLION)

- TABLE 29 INSULATED METAL PANELS MARKET, BY APPLICATION, 2021-2023 (MILLION SQUARE FEET)

- TABLE 30 INSULATED METAL PANELS MARKET, BY APPLICATION, 2024-2030 (MILLION SQUARE FEET)

- TABLE 31 INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 32 INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 33 INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 34 INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 35 INSULATED METAL PANELS MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 36 INSULATED METAL PANELS MARKET, BY REGION, 2024-2030 (USD MILLION)

- TABLE 37 INSULATED METAL PANELS MARKET, BY REGION, 2021-2023 (MILLION SQUARE FEET)

- TABLE 38 INSULATED METAL PANELS MARKET, BY REGION, 2024-2030 (MILLION SQUARE FEET)

- TABLE 39 ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 40 ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY COUNTRY, 2024-2030 (USD MILLION)

- TABLE 41 ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY COUNTRY, 2021-2023 (MILLION SQUARE FEET)

- TABLE 42 ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY COUNTRY, 2024-2030 (MILLION SQUARE FEET)

- TABLE 43 ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 44 ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 45 ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 46 ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 47 ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 48 ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 49 ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 50 ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 51 ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 52 ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 53 ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 54 ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 55 CHINA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 56 CHINA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 57 CHINA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 58 CHINA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 59 CHINA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 60 CHINA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 61 CHINA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 62 CHINA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 63 CHINA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 64 CHINA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 65 CHINA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 66 CHINA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 67 JAPAN: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 68 JAPAN: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 69 JAPAN: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 70 JAPAN: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 71 JAPAN: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 72 JAPAN: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 73 JAPAN: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 74 JAPAN: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 75 JAPAN: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 76 JAPAN: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 77 JAPAN: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 78 JAPAN: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 79 INDIA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 80 INDIA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 81 INDIA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 82 INDIA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 83 INDIA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 84 INDIA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 85 INDIA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 86 INDIA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 87 INDIA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 88 INDIA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 89 INDIA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 90 INDIA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 91 SOUTH KOREA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 92 SOUTH KOREA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 93 SOUTH KOREA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 94 SOUTH KOREA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 95 SOUTH KOREA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 96 SOUTH KOREA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 97 SOUTH KOREA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 98 SOUTH KOREA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 99 SOUTH KOREA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 100 SOUTH KOREA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 101 SOUTH KOREA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 102 SOUTH KOREA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 103 AUSTRALIA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 104 AUSTRALIA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 105 AUSTRALIA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 106 AUSTRALIA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 107 AUSTRALIA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 108 AUSTRALIA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 109 AUSTRALIA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 110 AUSTRALIA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 111 AUSTRALIA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 112 AUSTRALIA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 113 AUSTRALIA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 114 AUSTRALIA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 115 REST OF ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 116 REST OF ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 117 REST OF ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 118 REST OF ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 119 REST OF ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 120 REST OF ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 121 REST OF ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 122 REST OF ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 123 REST OF ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 124 REST OF ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 125 REST OF ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 126 REST OF ASIA PACIFIC: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 127 EUROPE: INSULATED METAL PANELS MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 128 EUROPE: INSULATED METAL PANELS MARKET, BY COUNTRY, 2024-2030 (USD MILLION)

- TABLE 129 EUROPE: INSULATED METAL PANELS MARKET, BY COUNTRY, 2021-2023 (MILLION SQUARE FEET)

- TABLE 130 EUROPE: INSULATED METAL PANELS MARKET, BY COUNTRY, 2024-2030 (MILLION SQUARE FEET)

- TABLE 131 EUROPE: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 132 EUROPE: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 133 EUROPE: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 134 EUROPE: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 135 EUROPE: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 136 EUROPE: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 137 EUROPE: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 138 EUROPE: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 139 EUROPE: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 140 EUROPE: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 141 EUROPE: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 142 EUROPE: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 143 UK: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 144 UK: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 145 UK: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 146 UK: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 147 UK: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 148 UK: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 149 UK: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 150 UK: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 151 UK: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 152 UK: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 153 UK: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 154 UK: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 155 GERMANY: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 156 GERMANY: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 157 GERMANY: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 158 GERMANY: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 159 GERMANY: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 160 GERMANY: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 161 GERMANY: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 162 GERMANY: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 163 GERMANY: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 164 GERMANY: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 165 GERMANY: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 166 GERMANY: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 167 FRANCE: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 168 FRANCE: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 169 FRANCE: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 170 FRANCE: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 171 FRANCE: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 172 FRANCE: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 173 FRANCE: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 174 FRANCE: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 175 FRANCE: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 176 FRANCE: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 177 FRANCE: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 178 FRANCE: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 179 ITALY: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 180 ITALY: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 181 ITALY: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 182 ITALY: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 183 ITALY: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 184 ITALY: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 185 ITALY: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 186 ITALY: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 187 ITALY: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 188 ITALY: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 189 ITALY: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 190 ITALY: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 191 SPAIN: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 192 SPAIN: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 193 SPAIN: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 194 SPAIN: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 195 SPAIN: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 196 SPAIN: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 197 SPAIN: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 198 SPAIN: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 199 SPAIN: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 200 SPAIN: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 201 SPAIN: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 202 SPAIN: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 203 REST OF EUROPE: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 204 REST OF EUROPE: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 205 REST OF EUROPE: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 206 REST OF EUROPE: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 207 REST OF EUROPE: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 208 REST OF EUROPE: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 209 REST OF EUROPE: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 210 REST OF EUROPE: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 211 REST OF EUROPE: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 212 REST OF EUROPE: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 213 REST OF EUROPE: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 214 REST OF EUROPE: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 215 NORTH AMERICA: INSULATED METAL PANELS MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 216 NORTH AMERICA: INSULATED METAL PANELS MARKET, BY COUNTRY, 2024-2030 (USD MILLION)

- TABLE 217 NORTH AMERICA: INSULATED METAL PANELS MARKET, BY COUNTRY, 2021-2023 (MILLION SQUARE FEET)

- TABLE 218 NORTH AMERICA: INSULATED METAL PANELS MARKET, BY COUNTRY, 2024-2030 (MILLION SQUARE FEET)

- TABLE 219 NORTH AMERICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 220 NORTH AMERICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 221 NORTH AMERICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 222 NORTH AMERICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 223 NORTH AMERICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 224 NORTH AMERICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 225 NORTH AMERICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 226 NORTH AMERICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 227 NORTH AMERICA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 228 NORTH AMERICA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 229 NORTH AMERICA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 230 NORTH AMERICA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 231 US: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 232 US: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 233 US: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 234 US: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 235 US: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 236 US: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 237 US: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 238 US: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 239 US: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 240 US: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 241 US: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 242 US: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 243 CANADA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 244 CANADA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 245 CANADA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 246 CANADA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 247 CANADA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 248 CANADA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 249 CANADA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 250 CANADA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 251 CANADA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 252 CANADA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 253 CANADA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 254 CANADA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 255 MEXICO: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 256 MEXICO: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 257 MEXICO: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 258 MEXICO: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 259 MEXICO: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 260 MEXICO: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 261 MEXICO: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 262 MEXICO: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 263 MEXICO: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 264 MEXICO: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 265 MEXICO: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 266 MEXICO: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 267 SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 268 SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY COUNTRY, 2024-2030 (USD MILLION)

- TABLE 269 SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY COUNTRY, 2021-2023 (MILLION SQUARE FEET)

- TABLE 270 SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY COUNTRY, 2024-2030 (MILLION SQUARE FEET)

- TABLE 271 SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 272 SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 273 SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 274 SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 275 SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 276 SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 277 SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 278 SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 279 SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 280 SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 281 SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 282 SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 283 BRAZIL: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 284 BRAZIL: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 285 BRAZIL: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 286 BRAZIL: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 287 BRAZIL: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 288 BRAZIL: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 289 BRAZIL: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 290 BRAZIL: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 291 BRAZIL: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 292 BRAZIL: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 293 BRAZIL: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 294 BRAZIL: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 295 ARGENTINA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 296 ARGENTINA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 297 ARGENTINA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 298 ARGENTINA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 299 ARGENTINA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 300 ARGENTINA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 301 ARGENTINA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 302 ARGENTINA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 303 ARGENTINA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 304 ARGENTINA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 305 ARGENTINA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 306 ARGENTINA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 307 REST OF SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 308 REST OF SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 309 REST OF SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 310 REST OF SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 311 REST OF SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 312 REST OF SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 313 REST OF SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 314 REST OF SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 315 REST OF SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 316 REST OF SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 317 REST OF SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 318 REST OF SOUTH AMERICA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 319 MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 320 MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY COUNTRY, 2024-2030 (USD MILLION)

- TABLE 321 MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY COUNTRY, 2021-2023 (MILLION SQUARE FEET)

- TABLE 322 MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY COUNTRY, 2024-2030 (MILLION SQUARE FEET)

- TABLE 323 MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 324 MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 325 MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 326 MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 327 MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 328 MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 329 MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 330 MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 331 MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 332 MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 333 MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 334 MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 335 GCC COUNTRIES: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 336 GCC COUNTRIES: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 337 GCC COUNTRIES: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 338 GCC COUNTRIES: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 339 GCC COUNTRIES: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 340 GCC COUNTRIES: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 341 GCC COUNTRIES: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 342 GCC COUNTRIES: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 343 GCC COUNTRIES: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 344 GCC COUNTRIES: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 345 GCC COUNTRIES: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 346 GCC COUNTRIES: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 347 SAUDI ARABIA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 348 SAUDI ARABIA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 349 SAUDI ARABIA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 350 SAUDI ARABIA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 351 SAUDI ARABIA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 352 SAUDI ARABIA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 353 SAUDI ARABIA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 354 SAUDI ARABIA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 355 SAUDI ARABIA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 356 SAUDI ARABIA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 357 SAUDI ARABIA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 358 SAUDI ARABIA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 359 UAE: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 360 UAE: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 361 UAE: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 362 UAE: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 363 UAE: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 364 UAE: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 365 UAE: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 366 UAE: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 367 UAE: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 368 UAE: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 369 UAE: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 370 UAE: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 371 REST OF GCC: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 372 REST OF GCC: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 373 REST OF GCC: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 374 REST OF GCC: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 375 REST OF GCC: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 376 REST OF GCC: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 377 REST OF GCC: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 378 REST OF GCC: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 379 REST OF GCC: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 380 REST OF GCC: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 381 REST OF GCC : INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 382 REST OF GCC: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 383 SOUTH AFRICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 384 SOUTH AFRICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 385 SOUTH AFRICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 386 SOUTH AFRICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 387 SOUTH AFRICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 388 SOUTH AFRICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 389 SOUTH AFRICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 390 SOUTH AFRICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 391 SOUTH AFRICA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 392 SOUTH AFRICA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 393 SOUTH AFRICA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 394 SOUTH AFRICA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 395 REST OF MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (USD MILLION)

- TABLE 396 REST OF MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (USD MILLION)

- TABLE 397 REST OF MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 398 REST OF MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY METAL TYPE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 399 REST OF MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (USD MILLION)

- TABLE 400 REST OF MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (USD MILLION)

- TABLE 401 REST OF MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2021-2023 (MILLION SQUARE FEET)

- TABLE 402 REST OF MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2024-2030 (MILLION SQUARE FEET)

- TABLE 403 REST OF MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (USD MILLION)

- TABLE 404 REST OF MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (USD MILLION)

- TABLE 405 REST OF MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY END USE, 2021-2023 (MILLION SQUARE FEET)

- TABLE 406 REST OF MIDDLE EAST & AFRICA: INSULATED METAL PANELS MARKET, BY END USE, 2024-2030 (MILLION SQUARE FEET)

- TABLE 407 INSULATED METAL PANELS MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY MARKET PLAYERS BETWEEN JANUARY 2021 AND JANUARY 2026

- TABLE 408 INSULATED METAL PANELS MARKET: DEGREE OF COMPETITION

- TABLE 409 INSULATED METAL PANELS MARKET: REGION FOOTPRINT

- TABLE 410 INSULATED METAL PANELS MARKET: INSULATION TYPE FOOTPRINT

- TABLE 411 INSULATED METAL PANELS MARKET: METAL TYPE FOOTPRINT

- TABLE 412 INSULATED METAL PANELS MARKET: APPLICATION FOOTPRINT

- TABLE 413 INSULATED METAL PANELS MARKET: END-USE FOOTPRINT

- TABLE 414 INSULATED METAL PANEL MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 415 INSULATED METAL PANELS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 416 INSULATED METAL PANELS MARKET: PRODUCT LAUNCHES, JANUARY 2021-JANUARY 2026

- TABLE 417 INSULATED METAL PANELS MARKET: DEALS, JANUARY 2021-JANUARY 2026

- TABLE 418 INSULATED METAL PANELS MARKET: EXPANSIONS, JANUARY 2021-JANUARY 2026

- TABLE 419 INSULATED METAL PANELS MARKET: OTHER DEVELOPMENTS, JANUARY 2021-JANUARY 2026

- TABLE 420 KINGSPAN GROUP: COMPANY OVERVIEW

- TABLE 421 KINGSPAN GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 422 KINGSPAN GROUP: DEALS

- TABLE 423 KINGSPAN GROUP: EXPANSIONS

- TABLE 424 NUCOR CORPORATION: COMPANY OVERVIEW

- TABLE 425 NUCOR CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 426 NUCOR CORPORATION: DEALS

- TABLE 427 NUCOR CORPORATION: OTHER DEVELOPMENTS

- TABLE 428 ARCELORMITTAL: COMPANY OVERVIEW

- TABLE 429 ARCELORMITTAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 430 ARCELORMITTAL: PRODUCT LAUNCHES

- TABLE 431 ARCELORMITTAL: DEALS

- TABLE 432 ARCELORMITTAL: OTHER DEVELOPMENTS

- TABLE 433 RECTICEL NV/SA: COMPANY OVERVIEW

- TABLE 434 RECTICEL NV/SA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 435 RECTICEL NV/SA: DEALS

- TABLE 436 TATA STEEL: COMPANY OVERVIEW

- TABLE 437 TATA STEEL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 438 TATA STEEL: DEALS

- TABLE 439 ISOPAN S.P.A: COMPANY OVERVIEW

- TABLE 440 ISOPAN S.P.A.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 441 ISOPAN S.P.A.: DEALS

- TABLE 442 KPS GLOBAL LLC: COMPANY OVERVIEW

- TABLE 443 KPS GLOBAL LLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 444 KPS GLOBAL LLC: EXPANSIONS

- TABLE 445 WGI WESTMAN GROUP INC. (WGI): COMPANY OVERVIEW

- TABLE 446 WGI WESTMAN GROUP INC. (WGI): PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 447 BRUCHA GMBH: COMPANY OVERVIEW

- TABLE 448 BRUCHA GMBH: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 449 ASSAN PANEL A.S.: COMPANY OVERVIEW

- TABLE 450 ASSAN PANEL A.S.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 451 NORBEC INC.: COMPANY OVERVIEW

- TABLE 452 ZAMIL STEEL HOLDING COMPANY LIMITED: COMPANY OVERVIEW

- TABLE 453 LONDON ECO-METAL MANUFACTURING: COMPANY OVERVIEW

- TABLE 454 BRDECO GROUP: COMPANY OVERVIEW

- TABLE 455 STRUCTURAL PANELS, INC.: COMPANY OVERVIEW

- TABLE 456 ADVANCED PANEL PRODUCTS LTD.: COMPANY OVERVIEW

- TABLE 457 ATAS INTERNATIONAL, INC.: COMPANY OVERVIEW

- TABLE 458 GREEN SPAN PROFILES: COMPANY OVERVIEW

- TABLE 459 FALK BOUWSYSTEMEN B.V.: COMPANY OVERVIEW

- TABLE 460 PERMATHERM: COMPANY OVERVIEW

- TABLE 461 RAUTARUUKKI CORPORATION: COMPANY OVERVIEW

- TABLE 462 AMERICAN INSULATED PANEL: COMPANY OVERVIEW

- TABLE 463 LATTONEDIL: COMPANY OVERVIEW

- TABLE 464 STRUCTALL BUILDING SYSTEMS, INC.: COMPANY OVERVIEW

- TABLE 465 VULCAN STEEL STRUCTURES, INC.: COMPANY OVERVIEW

List of Figures

- FIGURE 1 INSULATED METAL PANELS MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 KEY INSIGHTS AND MARKET HIGHLIGHTS

- FIGURE 3 GLOBAL INSULATED METAL PANELS MARKET, 2025-2030

- FIGURE 4 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN INSULATED METAL PANELS MARKET (2021-2026)

- FIGURE 5 DISRUPTIVE TRENDS IMPACTING GROWTH OF INSULATED METAL PANELS MARKET DURING FORECAST PERIOD

- FIGURE 6 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS IN INSULATED METAL PANELS MARKET, 2024

- FIGURE 7 INDIA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 8 HIGH DEMAND FROM COMMERCIAL BUILDINGS, COLD STORAGE, INDUSTRIAL FACILITIES, AND DATA CENTERS TO CREATE OPPORTUNITIES FOR INSULATED METAL PANEL MANUFACTURERS

- FIGURE 9 ASIA PACIFIC ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

- FIGURE 10 PIR/PUR SEGMENT ACCOUNTED FOR LARGEST SHARE OF INSULATED METAL PANELS MARKET IN 2024

- FIGURE 11 INTERIOR WALL DOMINATED INSULATED METAL PANELS MARKET IN 2024

- FIGURE 12 NON-RESIDENTIAL SEGMENT ACCOUNTED FOR LARGEST SHARE OF INSULATED METAL PANELS MARKET IN 2024

- FIGURE 13 INDIA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 14 INSULATED METAL PANELS MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 15 GROSS VALUE ADDED BY CONSTRUCTION SECTOR IN INDIA, 2018-2025 (USD BILLION)

- FIGURE 16 OPERATING REVENUE IN CONSTRUCTION SECTOR OF SAUDI ARABIA, 2019-2024 (USD BILLION)

- FIGURE 17 GDP CONTRIBUTION BY CONSTRUCTION SECTOR IN UAE, 2019-2024 (USD BILLION)

- FIGURE 18 GLOBAL CO2 EMISSIONS OF BUILDINGS SECTOR, 2018-2023

- FIGURE 19 EXPORTS OF PROCESSED VEGETABLES GLOBALLY, 2019-2024 (USD BILLION)

- FIGURE 20 INSULATED METAL PANELS MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 21 INSULATED METAL PANELS MARKET: VALUE CHAIN ANALYSIS

- FIGURE 22 INSULATED METAL PANELS MARKET: ECOSYSTEM ANALYSIS

- FIGURE 23 AVERAGE SELLING PRICE TREND OF INSULATION MATERIAL, BY KEY PLAYER, 2024 (USD/SQUARE FEET)

- FIGURE 24 INSULATED METAL PANELS MARKET: AVERAGE SELLING PRICE, BY REGION, 2021-2024 (USD/SQUARE FEET)

- FIGURE 25 IMPORT DATA FOR HS CODE 730890-STRUCTURES AND PARTS OF STRUCTURES, OF IRON OR STEEL, N.E.S. (EXCL. BRIDGES AND BRIDGE-SECTIONS, TOWERS AND LATTICE MASTS, DOORS AND WINDOWS AND THEIR FRAMES, THRESHOLDS FOR DOORS, PROPS AND SIMILAR EQUIPMENT FOR SCAFFOLDING, SHUTTERING, PROPPING OR PIT-PROPPING), BY COUNTRY, 2020-2024 (USD BILLION)

- FIGURE 26 EXPORT DATA RELATED TO HS CODE 730890-STRUCTURES AND PARTS OF STRUCTURES, OF IRON OR STEEL, N.E.S. (EXCL. BRIDGES AND BRIDGE-SECTIONS, TOWERS AND LATTICE MASTS, DOORS AND WINDOWS AND THEIR FRAMES, THRESHOLDS FOR DOORS, PROPS AND SIMILAR EQUIPMENT FOR SCAFFOLDING, SHUTTERING, PROPPING OR PIT-PROPPING), BY COUNTRY, 2020-2024 (USD BILLION)

- FIGURE 27 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 28 INVESTMENT AND FUNDING SCENARIO, 2019-2025

- FIGURE 29 LIST OF MAJOR PATENTS FOR INSULATED METAL PANELS, 2014-2025

- FIGURE 30 MAJOR PATENTS APPLIED AND GRANTED RELATED TO INSULATED METAL PANELS, BY COUNTRY/REGION, 2014-2025

- FIGURE 32 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY END USE

- FIGURE 33 KEY BUYING CRITERIA, BY END USE

- FIGURE 35 INSULATED METAL PANELS MARKET, BY METAL TYPE, 2025 VS. 2030 (USD MILLION)

- FIGURE 36 INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL, 2025 VS. 2030 (USD MILLION)

- FIGURE 37 NUMBER OF HOME FIRE DEATHS IN US, 2018-2023

- FIGURE 38 EXTERIOR WALL SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 39 NON-RESIDENTIAL SEGMENT TO REGISTER FASTER GROWTH DURING FORECAST PERIOD

- FIGURE 40 ASIA PACIFIC TO ACCOUNT FOR LARGEST SHARE OF INSULATED METAL PANELS MARKET DURING FORECAST PERIOD

- FIGURE 41 ASIA PACIFIC: INSULATED METAL PANELS MARKET SNAPSHOT

- FIGURE 42 EUROPE: INSULATED METAL PANELS MARKET SNAPSHOT

- FIGURE 43 INSULATED METAL PANELS MARKET: REVENUE ANALYSIS OF KEY PLAYERS, 2020-2024 (USD BILLION)

- FIGURE 44 INSULATED METAL PANELS MARKET SHARE ANALYSIS, 2024

- FIGURE 45 INSULATED METAL PANELS MARKET: COMPANY VALUATION

- FIGURE 46 INSULATED METAL PANELS MARKET: FINANCIAL MATRIX (EV/EBITDA RATIO)

- FIGURE 47 INSULATED METAL PANELS MARKET: YEAR-TO-DATE PRICE AND FIVE-YEAR STOCK BETA

- FIGURE 48 INSULATED METAL PANELS MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 49 INSULATED METAL PANELS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 50 INSULATED METAL PANELS MARKET: COMPANY FOOTPRINT

- FIGURE 51 INSULATED METAL PANELS MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 52 KINGSPAN GROUP: COMPANY SNAPSHOT

- FIGURE 53 NUCOR CORPORATION: COMPANY SNAPSHOT

- FIGURE 54 ARCELORMITTAL: COMPANY SNAPSHOT

- FIGURE 55 RECTICEL NV/SA: COMPANY SNAPSHOT

- FIGURE 56 TATA STEEL: COMPANY SNAPSHOT

- FIGURE 57 INSULATED METAL PANELS MARKET: RESEARCH DESIGN

- FIGURE 58 BREAKDOWN OF PRIMARY INTERVIEWS

- FIGURE 59 MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

- FIGURE 60 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- FIGURE 61 MARKET SIZE ESTIMATION: SUPPLY-SIDE

- FIGURE 62 INSULATED METAL PANELS MARKET: DATA TRIANGULATION