PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1984857

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1984857

Food Pathogen Safety Testing Equipment & Supplies Market by Type (Systems, Consumables & Supplies ), Food Tested, by Site (In-House Laboratories, Outsourcing Facilities, Government Labs), Technology, and Region - Global Forecast to 2031

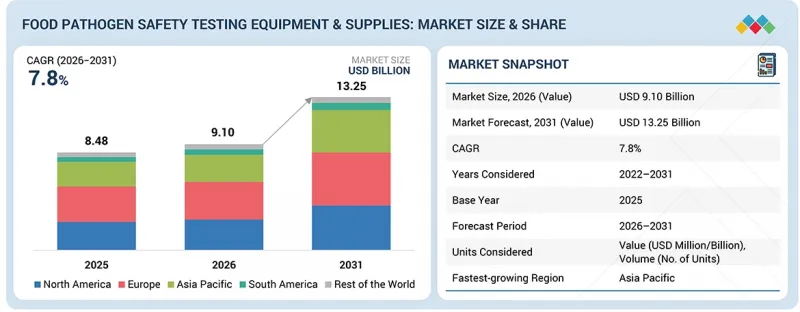

The food pathogen safety testing equipment & supplies market is estimated to be USD 9.10 billion in 2026 and is projected to reach USD 13.25 billion by 2031, at a CAGR of 7.8%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion) and Volume (Kiloton) |

| Segments | Type, Food Tested, Technology and Region |

| Regions covered | North America, Asia Pacific, Europe, the Middle East & Africa, and South America |

The market is continuing to rise, and this is a result of the rising interest in food safety and quality in the food industry, pharmaceutical industry, and also in the animal feed industry. Increased rate of food-borne diseases and the high compliance demands are compelling manufacturers to ensure that they establish effective pathogen testing procedures to preserve product safety as well as ensure that their products comply with the provisions. The market is also expanding due to the improvement of rapid testing methods like the PCR-based testing, immunoassays, and the automated microbial detection and testing system, which are used to enhance quality testing and turnaround time. Moreover, the growing popularity of processed food products, ready-to-eat and packaged food products, is prompting the use of tests and consumables that can be trusted across the production and supply chain. As the food trade worldwide continues to grow and increasing attention is given to the traceability of products, it can be forecasted that the ongoing demand for food pathogen safety testing equipment and supplies will be supported by the influx of investments in on-site testing, laboratory automation, and computerized systems of food quality control over the coming years.

In type, the segments of consumables and kits are projected to take the biggest share of the market in the food pathogen safety testing equipment and supplies.

The highest share of the market is comprised of consumables and kits, which are principally attributed to the recurring nature of their application in routine pathogen testing processes. These will be the reagents, test kits, culture media, and sample preparation products that are mandatory in every test performed in food production and quality control plants. The ever-increasing requirements of routine and quick testing in order to comply with food safety standards have raised the pressure on the consumption of good-quality consumables within the in-house and third-party laboratories. Also, the increasing usage of PCR-based and immunoassay-based testing technologies is contributing to the consumption of pathogen detection kits, which has a similar effect on the dominance of the segment in the market.

The meat & poultry category is determined to take the highest portion of the market among foods tested.

The meat & poultry segment is the most vulnerable to microbial contamination and high regulatory monitoring requirements; therefore, it has the highest share in the market. Salmonella, Listeria, and E. coli are more likely to happen in this type of food. Thus, it is important to regularly test food products during processing, packaging, and distribution processes. The rise in the consumption of processed and packaged meat products around the world has further augmented the demand to identify the best pathogen testing solutions. Consequently, food manufacturing companies are putting more money into sophisticated testing tools and consumables in order to secure the safety of the products and have them in line with food safety standards.

According to site, outsourcing facilities (service laboratories) are projected to take over the market.

The largest site segment is outsourcing facilities through third-party and contract testing laboratories. The high cost of testing infrastructure and technical skills makes many food manufacturers outsource pathogen testing services to special laboratories. Laboratories provide a high level of testing, quicker turnaround, and assistance when it comes to fulfilling regulatory compliance. The rising number of food safety requirements, as well as the demand to perform precise microbial testing, prompts businesses to trust certified external laboratories to perform regular quality control and verification procedures.

In terms of region, Europe has been estimated to be the largest market in the food pathogen safety testing equipment and supplies.

The Europe region is the greatest contributor to global market share, which is a result of stringent food safety standards and comprehensive quality assurance systems in the entire food processing industry. The introduction of regulatory tests to establish food safety and traceability has prompted the use of pathogen test solutions, which have become a mandatory testing requirement in the region. Also, the high concentration of processed food producers and increased awareness of consumers about the quality of food and food safety have also contributed to market growth. The laboratory automation and sophisticated microbial testing technologies are also making investments in the region, leading to the top position in the market.

In-depth interviews have been conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the food pathogen safety testing equipment & supplies market.

- By Company Type: Tier 1 - 30%, Tier 2 - 25%, and Tier 3 - 45%

- By Designation: Directors - 30%, Managers - 25%, Others - 45%

- By Region: North America - 20%, Europe - 30%, Asia Pacific - 40%, and Rest of the World - 10%

Prominent companies in the market include Thermo Fisher Scientific Inc. (US), Bio-Rad Laboratories, Inc. (US), Merck KGaA (Germany), Neogen Corporation (US), bioMerieux (France), Agilent Technologies, Inc. (US), QIAGEN (Germany), Shimadzu Corporation (Japan), Bruker (US), PerkinElmer Inc. (US), Hygiena, LLC (US), Solabia Group (France), Roka Bio Science (US), Promega Corporation (US), Romer Labs Division Holding (Austria), and others.

Research Coverage

This research report categorizes the food pathogen safety testing equipment & supplies market by type (systems [hybridization-based, chromatography-based, spectrometry-based, immunoassay-based], consumables & supplies [test kits, microbial culture media, reagents & other consumables]), food tested (meat & poultry, fish & seafood, processed food, fruits & vegetables, dairy products, cereals & grains, other food products), by site (in-house laboratories [factory labs], outsourcing facilities [service labs], government labs), technology [qualitative], and region (North America, Europe, Asia Pacific, South America, and Rest of the World).

The report's scope encompasses detailed information on the major factors, including drivers, restraints, challenges, and opportunities, that influence the growth of the food pathogen safety testing equipment & supplies industry. A thorough analysis of the key industry players has been done to provide insights into their business, services, key strategies, contracts, partnerships, agreements, product launches, mergers & acquisitions, and recent developments associated with the food pathogen safety testing equipment & supplies market. This report provides a competitive analysis of emerging startups in the food pathogen safety testing equipment & supplies market ecosystem. Furthermore, the study covers industry-specific trends, including technology analysis, ecosystem & market mapping, and patent & regulatory landscape, among others.

Reasons to Buy This Report

The report provides market leaders/new entrants with information on the closest approximations of revenue numbers for the overall food pathogen safety testing equipment & supplies market and its subsegments. It will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market, providing them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (expansion of genomic surveillance and traceability), restraints (high capital and recurring cost), opportunities (expansion of portable and on-site rapid testing), and challenges (regulatory fragmentation and acceptance timelines) influencing the growth of the food pathogen safety testing equipment & supplies market

- Product Development/Innovation: Detailed insights into research & development activities and new product launches in the food pathogen safety testing equipment & supplies market

- Market Development: Comprehensive information about lucrative markets-analysis of food pathogen safety testing equipment & supplies across varied regions

- Market Diversification: Exhaustive information about new product sources, untapped geographies, recent developments, and investments in the food pathogen safety testing equipment & supplies market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, brand/product comparison, and product footprints of leading players such as Thermo Fisher Scientific Inc. (US), Bio-Rad Laboratories, Inc. (US), Merck KGaA (Germany), Neogen Corporation (US), bioMerieux (France), Agilent Technologies, Inc. (US), QIAGEN (Germany), Shimadzu Corporation (Japan), Bruker (US), PerkinElmer Inc. (US), Hygiena, LLC (US), Solabia Group (France), Roka Bio Science (US), Promega Corporation (US), Romer Labs Division Holding (Austria) and others in the food pathogen safety testing equipment & supplies market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE AND SEGMENTATION

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.5.1 CURRENCY UNIT

- 1.5.2 VOLUME UNIT

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET

- 3.2 FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY TYPE AND REGION

- 3.3 FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SITE

- 3.4 FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY TYPES OF FOOD TESTED

- 3.5 FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SYSTEMS

- 3.6 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY CONSUMABLES & SUPPLIES

- 3.7 FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Persistent burden of foodborne illness

- 4.2.1.2 Regulatory tightening and preventive controls

- 4.2.1.3 Expansion of genomic surveillance and traceability

- 4.2.1.4 Faster testing and automation needs

- 4.2.2 RESTRAINTS

- 4.2.2.1 High capital and recurring costs

- 4.2.2.2 Workforce and technical capacity gaps

- 4.2.2.3 Complex validation and multi-jurisdictional compliance

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of portable and on-site rapid testing

- 4.2.3.2 Digital integration and smart laboratory ecosystems

- 4.2.3.3 Reagent-as-a-service and flexible commercial models

- 4.2.4 CHALLENGES

- 4.2.4.1 Regulatory fragmentation and acceptance timelines

- 4.2.4.2 Cybersecurity and data integrity risks

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET

- 4.3.1.1 Rapid on-site confirmatory testing

- 4.3.1.2 Cost-effective validated solutions for emerging markets

- 4.3.1.3 Laboratory digitization and cybersecurity-hardened solutions

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.3.2.1 Viability-aware rapid testing platforms

- 4.3.2.2 Flexible commercial deployment models

- 4.3.2.3 Genomic surveillance-as-a-service platforms

- 4.3.2.4 Digitally secure smart laboratory infrastructure

- 4.3.1 UNMET NEEDS IN FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 THREAT OF NEW ENTRANTS

- 5.2 MACROECONOMICS OUTLOOK

- 5.2.1 RISING GLOBAL POPULATION AND INCREASING FOOD DEMAND

- 5.2.2 INDUSTRIALIZATION OF FOOD PROCESSING IN EMERGING ECONOMIES

- 5.2.3 RISING PUBLIC HEALTH EXPENDITURE AND FOOD SAFETY INVESTMENTS

- 5.3 SUPPLY CHAIN ANALYSIS (MICROBIOLOGY AGAR CULTURE PRODUCTS)

- 5.3.1 INPUT AND RAW MATERIAL SOURCING

- 5.3.2 CULTIVATION AND SEAWEED PROCESSING

- 5.3.3 AGAR EXTRACTION AND REFINEMENT

- 5.3.4 MEDIA FORMULATION AND MANUFACTURING

- 5.3.5 QUALITY TESTING AND CERTIFICATION

- 5.3.6 PACKAGING & LABELING

- 5.3.7 WAREHOUSING & DISTRIBUTION

- 5.3.8 END-USE APPLICATION

- 5.4 VALUE CHAIN ANALYSIS (FOOD PATHOGEN TESTING KITS)

- 5.4.1 RAW MATERIAL PROCUREMENT

- 5.4.2 KIT FORMULATION & MANUFACTURING

- 5.4.3 QUALITY ASSURANCE & REGULATORY CERTIFICATION

- 5.4.4 SALES, MARKETING & DISTRIBUTION

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY SYSTEM

- 5.6.2 AVERAGE SELLING PRICE, BY SYSTEMS

- 5.6.3 AVERAGE SELLING PRICE OF TEST KITS, BY REGION

- 5.6.4 AVERAGE SELLING PRICE OF MICROBIAL CULTURE MEDIA, BY REGION

- 5.6.5 AVERAGE SELLING PRICE OF REAGENTS & CONSUMABLES, BY REGION

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 902720)

- 5.7.2 EXPORT SCENARIO (HS CODE 902720)

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 BCN RESEARCH LABORATORIES PARTNERED WITH BIOMERIEUX TO INTRODUCE GENE-UP SYSTEMS FOR FOOD SAFETY TESTING

- 5.11.2 EUROFINS COLLABORATED WITH RHEONIX TO INTRODUCE RHEONIX LISTERIA PATTERNALERT ASSAY

- 5.12 IMPACT OF 2025 US TARIFF - FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRIES/REGIONS

- 5.12.4.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGY ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 PCR-BASED MOLECULAR DIAGNOSTICS

- 6.1.2 MICROARRAY-BASED DETECTION PLATFORMS

- 6.1.3 RAPID ON-SITE DETECTION SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 AUTOMATED MICROBIAL DETECTION SYSTEMS

- 6.2.2 CHROMATOGRAPHY-BASED TESTING SOLUTIONS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 BIOSENSOR-BASED DETECTION TECHNOLOGIES

- 6.3.2 AI-ENABLED FOOD SAFETY MONITORING PLATFORMS

- 6.4 PATENT ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.2 LIST OF MAJOR PATENTS, JANUARY 2017-DECEMBER 2025

- 6.5 FUTURE APPLICATIONS

- 6.5.1 AI-INTEGRATED PATHOGEN DETECTION PLATFORMS

- 6.5.2 PORTABLE ON-SITE FOOD TESTING DEVICES

- 6.5.3 LAB-ON-CHIP RAPID DETECTION SYSTEMS

- 6.5.4 MICROFLUIDIC BIOSENSOR-BASED DETECTION

- 6.5.5 REAL-TIME FOOD QUALITY MONITORING SENSORS

- 6.6 IMPACT OF AI/GEN AI ON FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES INDUSTRY

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN BIOTECHNOLOGY PROCESSING AND CULTIVATION

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 READINESS TO ADOPT GENERATIVE AI IN FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.7.1 CLEAR LABS: AUTOMATED NGS-BASED PATHOGEN DETECTION FOR FOOD SAFETY

- 6.7.2 NEMIS TECHNOLOGIES: ON-SITE RAPID PATHOGEN DETECTION FOR FOOD PROCESSING FACILITIES

- 6.7.3 PATHOGENDX: MICROARRAY-BASED MULTI-PATHOGEN DETECTION TECHNOLOGY

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY FRAMEWORK

- 7.1.1.1 Global Food Safety Initiative (GFSI)

- 7.1.1.2 North America

- 7.1.1.2.1 US

- 7.1.1.2.1.1 Federal Legislation

- 7.1.1.2.1.2 State Legislation

- 7.1.1.2.1.3 Food Safety in Retail Food

- 7.1.1.2.1.4 Food Safety in Trade

- 7.1.1.2.1.5 HACCP Regulation

- 7.1.1.2.1.6 US Regulation for Foodborne Pathogens in Poultry

- 7.1.1.2.1.7 Food Safety Regulation for Fruit and Vegetable Growers

- 7.1.1.2.2 Canada

- 7.1.1.2.3 Mexico

- 7.1.1.2.1 US

- 7.1.1.3 Europe

- 7.1.1.3.1 European Union

- 7.1.1.3.1.1 Microbiological Criteria Regulation

- 7.1.1.3.2 Germany

- 7.1.1.3.3 UK

- 7.1.1.3.4 France

- 7.1.1.3.5 Italy

- 7.1.1.3.6 Poland

- 7.1.1.3.1 European Union

- 7.1.1.4 Asia Pacific

- 7.1.1.4.1 China

- 7.1.1.4.2 Japan

- 7.1.1.4.3 India

- 7.1.1.4.3.1 Food Safety Standards Amendment Regulation, 2012

- 7.1.1.4.3.2 Food Safety Standards Amendment Regulation, 2011

- 7.1.1.4.3.3 Food Safety and Standards Act, 2006

- 7.1.1.4.4 Australia and New Zealand

- 7.1.1.4.4.1 Food Standards Australia and New Zealand

- 7.1.1.5 South America

- 7.1.1.5.1 Brazil

- 7.1.1.5.1.1 Ministry of Agriculture, Livestock, and Food Supply (MAPA)

- 7.1.1.5.1.2 Ministry of Health (MS)

- 7.1.1.5.2 Argentina

- 7.1.1.5.1 Brazil

- 7.1.1.6 Rest of the World

- 7.1.1.6.1 South Africa

- 7.1.1.6.1.1 International vs. Local Standards & Legislation

- 7.1.1.6.1.2 Private Standards in South Africa and Requirements for Product Testing

- 7.1.1.6.1 South Africa

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.3 INDUSTRY STANDARDS

- 7.1.4 LABELING REQUIREMENTS AND CLAIMS

- 7.1.5 ANTICIPATED REGULATORY CHANGES IN NEXT 5-10 YEARS

- 7.1.5.1 Stricter validation requirements for microbiological testing methods

- 7.1.5.2 Expansion of rapid testing approval pathways

- 7.1.5.3 Mandatory digital traceability in food safety testing workflows

- 7.1.5.4 Strengthening of environmental monitoring and hygiene testing regulations

- 7.1.1 REGULATORY FRAMEWORK

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 ENERGY-EFFICIENT LABORATORY SYSTEMS

- 7.2.2 SUSTAINABLE REAGENTS AND WASTE MANAGEMENT

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY SOURCE

9 FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 SYSTEMS

- 9.2.1 HYBRIDIZATION-BASED

- 9.2.1.1 Need for high analytical precision in food testing to drive adoption of hybridization-based systems

- 9.2.1.2 Polymerase chain reaction (PCR)

- 9.2.1.3 Gene amplifiers

- 9.2.2 CHROMATOGRAPHY-BASED

- 9.2.2.1 Focus on detecting chemical contaminants in food to encourage use of chromatography-based techniques

- 9.2.2.2 High-performance liquid chromatography (HPLC)

- 9.2.2.3 Liquid chromatography

- 9.2.2.4 Gas chromatography

- 9.2.2.5 Other chromatography-based systems

- 9.2.3 SPECTROMETRY-BASED

- 9.2.3.1 Growing demand to gain analytical approach to food pathogen testing to drive market

- 9.2.3.2 UV-visible spectroscopy

- 9.2.3.3 Infrared (IR) spectroscopy

- 9.2.3.4 Mass spectrometry (MS)

- 9.2.4 IMMUNOASSAY-BASED

- 9.2.4.1 Focus on building ability to test multiple samples to drive use of immunoassay-based systems

- 9.2.1 HYBRIDIZATION-BASED

- 9.3 CONSUMABLES & SUPPLIES

- 9.3.1 TEST KITS

- 9.3.1.1 Need for user-friendly and efficient food testing solutions to boost growth

- 9.3.2 MICROBIAL CULTURE MEDIA

- 9.3.2.1 Growing demand for advanced technologies to drive adoption of food safety testing solutions

- 9.3.3 REAGENTS & OTHER CONSUMABLES

- 9.3.3.1 Need for operational efficiency and ease of use in food safety testing environments

- 9.3.1 TEST KITS

10 FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY FOOD TESTED

- 10.1 INTRODUCTION

- 10.2 MEAT & POULTRY

- 10.2.1 RISING GLOBAL MEAT AND POULTRY CONSUMPTION TO SPUR DEMAND

- 10.3 FISH & SEAFOOD

- 10.3.1 GROWING RISK OF CONTAMINATION OF FISH AND SEAFOOD DUE TO SUPPLY CHAIN COMPLEXITIES TO DRIVE MARKET

- 10.4 DAIRY PRODUCTS

- 10.4.1 MOUNTING CASES OF LISTERIOSIS AND OTHER PATHOGEN-RELATED ILLNESSES IN DAIRY PRODUCTS TO STIMULATE MARKET DEMAND

- 10.5 PROCESSED FOOD

- 10.5.1 PROCESSED FOODS' SUSCEPTIBILITY TO PATHOGEN CONTAMINATION TO DRIVE DEMAND FOR SAFETY TESTING EQUIPMENT

- 10.6 FRUITS & VEGETABLES

- 10.6.1 MULTIPLE OUTBREAKS ASSOCIATED WITH PATHOGENS IN FRUITS AND VEGETABLES TO FUEL MARKET GROWTH

- 10.7 CEREALS & GRAINS

- 10.7.1 GROWING RISK OF CROSS-CONTAMINATION DUE TO WIDE APPLICATION OF CEREALS AND GRAINS IN FOOD INDUSTRY TO BOOST MARKET

- 10.8 OTHER FOOD PRODUCTS

11 FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SITE

- 11.1 INTRODUCTION

- 11.2 IN-HOUSE LABORATORIES (FACTORY LABS)

- 11.2.1 NEED TO MAINTAIN BRAND REPUTATION AND CONSUMER TRUST TO DRIVE USE OF IN-HOUSE LABORATORIES

- 11.3 OUTSOURCING FACILITIES (SERVICE LABS)

- 11.3.1 NEED TO ACCESS SPECIALIZED EXPERTISE AND ADVANCED TECHNOLOGIES TO DRIVE DEMAND FOR OUTSOURCING LABORATORIES

- 11.4 GOVERNMENT LABS

- 11.4.1 INDEPENDENT AND IMPARTIAL TESTING PROVIDED BY GOVERNMENT LABS TO FUEL MARKET GROWTH

12 FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY TECHNOLOGY (QUALITATIVE)

- 12.1 INTRODUCTION

- 12.2 MOLECULAR METHODS

- 12.3 IMMUNOLOGICAL METHODS

- 12.4 CULTURAL AND TRADITIONAL METHODS

- 12.5 SENSOR AND BIOSENSOR TECHNOLOGIES

- 12.6 EMERGING RAPID AND POINT OF CARE TECHNOLOGIES

13 FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Stringent food safety regulations to stimulate market

- 13.2.2 CANADA

- 13.2.2.1 Government initiatives aimed at reducing pathogens in meat and poultry to boost growth

- 13.2.3 MEXICO

- 13.2.3.1 Growing food exports to US and need for stringent safety measures to boost market

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Rising concerns over foodborne illnesses to drive market

- 13.3.2 FRANCE

- 13.3.2.1 Prevalence of multiple product recalls in country to stimulate growth

- 13.3.3 UK

- 13.3.3.1 Government funding and support initiatives for tracking foodborne pathogens to propel market

- 13.3.4 ITALY

- 13.3.4.1 Thriving tourism and hospitality industry to boost growth

- 13.3.5 SPAIN

- 13.3.5.1 Ongoing struggle with listeriosis and other foodborne illnesses to spur growth

- 13.3.6 POLAND

- 13.3.6.1 Growing dairy industry and exports to Ukraine to drive growth

- 13.3.7 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Government regulations and certifications for food safety to propel market

- 13.4.2 JAPAN

- 13.4.2.1 Rising incidences of food poisoning and increased food safety tests to drive market

- 13.4.3 INDIA

- 13.4.3.1 Growing food processing market to boost demand for food pathogen testing equipment

- 13.4.4 AUSTRALIA & NEW ZEALAND

- 13.4.4.1 Fear of outbreaks of Salmonella and E. coli to boost demand for food pathogen testing equipment

- 13.4.5 SOUTHEAST ASIA

- 13.4.5.1 Increasing awareness regarding safety and quality of food to encourage adoption of food pathogen testing equipment

- 13.4.6 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Booming food processing industry to spur market

- 13.5.2 ARGENTINA

- 13.5.2.1 Awareness among consumers regarding mounting cases of foodborne illnesses to contribute to market growth

- 13.5.3 REST OF SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.6 REST OF THE WORLD

- 13.6.1 MIDDLE EAST

- 13.6.1.1 Heavy reliance on imported foods to drive demand for food pathogen safety testing equipment

- 13.6.2 AFRICA

- 13.6.2.1 Increasing international collaborations dedicated to elevating food safety standards to drive demand

- 13.6.1 MIDDLE EAST

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS, 2022-2024

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.5.1 COMPANY VALUATION

- 14.5.2 EV/EBITDA

- 14.6 BRAND COMPARISON ANALYSIS

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: KEY STARTUPS/SMES, 2025

- 14.9 COMPETITIVE SCENARIO AND TRENDS

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

- 14.9.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 THERMO FISHER SCIENTIFIC INC.

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.3.2 Expansions

- 15.1.1.3.3 Other developments

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices made

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 BIO-RAD LABORATORIES, INC.

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 MERCK KGAA

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Expansions

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 NEOGEN CORPORATION

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 SHIMADZU CORPORATION

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices made

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 BIOMERIEUX

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches

- 15.1.6.3.2 Deals

- 15.1.6.4 MnM view

- 15.1.7 AGILENT TECHNOLOGIES, INC.

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Expansions

- 15.1.7.4 MnM view

- 15.1.8 QIAGEN

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches

- 15.1.8.3.2 Deals

- 15.1.8.4 MnM view

- 15.1.9 BRUKER

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.9.4 MnM view

- 15.1.10 PERKINELMER INC.

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches

- 15.1.10.3.2 Expansions

- 15.1.10.4 MnM view

- 15.1.11 HYGIENA, LLC

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Product launches

- 15.1.11.3.2 Deals

- 15.1.11.4 MnM view

- 15.1.12 SOLABIA GROUP (BIOKAR)

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Deals

- 15.1.12.4 MnM view

- 15.1.13 ROKA BIO SCIENCE

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.13.3 Recent developments

- 15.1.13.4 MnM view

- 15.1.14 PROMEGA CORPORATION

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Deals

- 15.1.14.4 MnM view

- 15.1.15 ROMER LABS DIVISION HOLDING

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.15.3 Recent developments

- 15.1.15.4 MnM view

- 15.1.1 THERMO FISHER SCIENTIFIC INC.

- 15.2 STARTUPS/SMES

- 15.2.1 CHARM SCIENCES

- 15.2.1.1 Business overview

- 15.2.1.2 Products/Solutions/Services offered

- 15.2.1.3 Recent developments

- 15.2.1.3.1 Other developments

- 15.2.1.4 MnM view

- 15.2.2 MICROBIOLOGICS, INC.

- 15.2.2.1 Business overview

- 15.2.2.2 Products/Solutions/Services offered

- 15.2.2.3 Recent developments

- 15.2.2.3.1 Deals

- 15.2.2.4 MnM view

- 15.2.3 R-BIOPHARM

- 15.2.3.1 Business overview

- 15.2.3.2 Products/Solutions/Services offered

- 15.2.3.3 Recent developments

- 15.2.3.3.1 Deals

- 15.2.3.4 MnM view

- 15.2.4 CONDALAB

- 15.2.4.1 Business overview

- 15.2.4.2 Products/Solutions/Services offered

- 15.2.4.3 Recent developments

- 15.2.4.4 MnM view

- 15.2.5 CHROMAGAR

- 15.2.5.1 Business overview

- 15.2.5.2 Products/Solutions/Services offered

- 15.2.5.3 Recent developments

- 15.2.5.4 MnM view

- 15.2.6 GOLD STANDARD DIAGNOSTICS

- 15.2.7 CLEAR LABS, INC.

- 15.2.8 RING BIOTECHNOLOGY CO LTD.

- 15.2.9 NEMIS TECHNOLOGIES AG

- 15.2.10 PATHOGENDX CORPORATION

- 15.2.1 CHARM SCIENCES

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Breakdown of primary profiles

- 16.1.2.3 Key insights from industry experts

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 TOP-DOWN APPROACH

- 16.2.2 SUPPLY-SIDE ANALYSIS

- 16.2.3 BOTTOM-UP APPROACH (DEMAND SIDE)

- 16.3 DATA TRIANGULATION

- 16.4 RESEARCH ASSUMPTIONS

- 16.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

17 ADJACENT AND RELATED MARKETS

- 17.1 INTRODUCTION

- 17.2 LIMITATIONS

- 17.3 FOOD SAFETY TESTING MARKET

- 17.3.1 MARKET DEFINITION

- 17.3.2 MARKET OVERVIEW

- 17.4 FOOD DIAGNOSTICS MARKET

- 17.4.1 MARKET DEFINITION

- 17.4.2 MARKET OVERVIEW

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS

List of Tables

- TABLE 1 INCLUSIONS AND EXCLUSIONS

- TABLE 2 USD EXCHANGE RATES, 2020-2024

- TABLE 3 INTERCONNECTED MARKETS

- TABLE 4 CROSS-SECTOR OPPORTUNITIES

- TABLE 5 KEY MOVES AND STRATEGIC FOCUS

- TABLE 6 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 7 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET: SUPPLY CHAIN ANALYSIS (MICROBIOLOGY AGAR CULTURE PRODUCTS)

- TABLE 8 ROLES OF COMPANIES IN FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES ECOSYSTEM

- TABLE 9 IMPORT DATA RELATED TO HS CODE 902720-COMPLIANT PRODUCTS, BY KEY COUNTRY, 2025-2022 (USD THOUSANDS)

- TABLE 10 EXPORT DATA RELATED TO HS CODE 902720-COMPLIANT PRODUCTS, BY KEY COUNTRY, 2025-2022 (USD THOUSANDS)

- TABLE 11 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET: LIST OF KEY CONFERENCES AND EVENTS, 2026-2027

- TABLE 12 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 13 TOP USE CASES AND MARKET POTENTIAL

- TABLE 14 BEST PRACTICES: COMPANIES IMPLEMENTING USE CASES

- TABLE 15 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET: CASE STUDIES RELATED TO GEN AI IMPLEMENTATION

- TABLE 16 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- TABLE 17 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 20 SOUTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 21 GLOBAL INDUSTRY STANDARDS IN FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET

- TABLE 22 LABELING REQUIREMENTS AND CLAIMS IN FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET

- TABLE 23 CERTIFICATIONS, LABELLING, AND ECO-STANDARDS IN FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET

- TABLE 24 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS

- TABLE 25 KEY CRITERIA FOR SELECTING SUPPLIERS/VENDORS

- TABLE 26 UNMET NEEDS IN FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY END-USE INDUSTRY

- TABLE 27 COST DYNAMICS IN FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET

- TABLE 28 MARGIN OPPORTUNITIES IN FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY TYPE

- TABLE 29 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 30 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 31 FOOD PATHOGEN SAFETY TESTING SYSTEMS MARKET, BY SUBTYPE, 2022-2025 (USD MILLION)

- TABLE 32 FOOD PATHOGEN SAFETY TESTING SYSTEMS MARKET, BY SUBTYPE, 2026-2031 (USD MILLION)

- TABLE 33 FOOD PATHOGEN SAFETY TESTING SYSTEMS MARKET, BY SUBTYPE, 2022-2025 (NO. OF UNITS)

- TABLE 34 FOOD PATHOGEN SAFETY TESTING SYSTEMS MARKET, BY SUBTYPE, 2026-2031 (NO. OF UNITS)

- TABLE 35 FOOD PATHOGEN SAFETY TESTING SYSTEMS MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 36 FOOD PATHOGEN SAFETY TESTING SYSTEMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 37 GENE TARGETS USED FOR FOOD PATHOGENS IN DEVELOPED PCR TESTS

- TABLE 38 HYBRIDIZATION-BASED FOOD PATHOGEN SAFETY TESTING SYSTEMS MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 39 HYBRIDIZATION-BASED FOOD PATHOGEN SAFETY TESTING SYSTEMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 40 CHROMATOGRAPHY-BASED FOOD PATHOGEN SAFETY TESTING SYSTEMS MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 41 CHROMATOGRAPHY-BASED FOOD PATHOGEN SAFETY TESTING SYSTEMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 42 SPECTROMETRY-BASED FOOD PATHOGEN SAFETY TESTING SYSTEMS MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 43 SPECTROMETRY-BASED FOOD PATHOGEN SAFETY TESTING SYSTEMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 44 IMMUNOASSAY-BASED FOOD PATHOGEN SAFETY TESTING SYSTEMS MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 45 IMMUNOASSAY-BASED FOOD PATHOGEN SAFETY TESTING SYSTEMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 46 FOOD PATHOGEN SAFETY TESTING CONSUMABLES & SUPPLIES MARKET, BY SUBTYPE, 2022-2025 (USD MILLION)

- TABLE 47 FOOD PATHOGEN SAFETY TESTING CONSUMABLES & SUPPLIES MARKET, BY SUBTYPE, 2026-2031 (USD MILLION)

- TABLE 48 FOOD PATHOGEN SAFETY TESTING CONSUMABLES & SUPPLIES MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 49 FOOD PATHOGEN SAFETY TESTING CONSUMABLES & SUPPLIES MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 50 FOOD PATHOGEN SAFETY TEST KITS MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 51 FOOD PATHOGEN SAFETY TEST KITS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 52 FOOD PATHOGEN SAFETY TEST KITS MARKET, BY REGION, 2022-2025 (MILLION TEST UNITS)

- TABLE 53 FOOD PATHOGEN SAFETY TEST KITS MARKET, BY REGION, 2026-2031 (MILLION TEST UNITS)

- TABLE 54 FOOD PATHOGEN SAFETY TESTING MICROBIAL CULTURE MEDIA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 55 FOOD PATHOGEN SAFETY TESTING MICROBIAL CULTURE MEDIA MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 56 FOOD PATHOGEN SAFETY TESTING MICROBIAL CULTURE MEDIA MARKET, BY REGION, 2022-2025 (TONS)

- TABLE 57 FOOD PATHOGEN SAFETY TESTING MICROBIAL CULTURE MEDIA MARKET, BY REGION, 2026-2031 (TONS)

- TABLE 58 FOOD PATHOGEN SAFETY TESTING REAGENTS AND OTHER CONSUMABLES MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 59 FOOD PATHOGEN SAFETY TESTING REAGENTS AND OTHER CONSUMABLES MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 60 FOOD PATHOGEN SAFETY TESTING REAGENTS AND OTHER CONSUMABLES MARKET, BY REGION, 2022-2025 (MILLION TEST UNITS)

- TABLE 61 FOOD PATHOGEN SAFETY TESTING REAGENTS AND OTHER CONSUMABLES MARKET, BY REGION, 2026-2031 (MILLION TEST UNITS)

- TABLE 62 FOODBORNE PATHOGENS, BY FOOD SOURCE

- TABLE 63 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 64 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 65 FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET FOR MEAT & POULTRY, BY REGION, 2022-2025 (USD MILLION)

- TABLE 66 FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET FOR MEAT & POULTRY, BY REGION, 2026-2031 (USD MILLION)

- TABLE 67 FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET FOR FISH & SEAFOOD, BY REGION, 2022-2025 (USD MILLION)

- TABLE 68 FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET FOR FISH & SEAFOOD, BY REGION, 2026-2031 (USD MILLION)

- TABLE 69 FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET FOR DAIRY PRODUCTS, BY REGION, 2022-2025 (USD MILLION)

- TABLE 70 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET FOR DAIRY PRODUCTS, BY REGION, 2026-2031 (USD MILLION)

- TABLE 71 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET FOR PROCESSED FOOD, BY REGION, 2022-2025 (USD MILLION)

- TABLE 72 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET FOR PROCESSED FOOD, BY REGION, 2026-2031 (USD MILLION)

- TABLE 73 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET FOR FRUITS & VEGETABLES, BY REGION, 2022-2025 (USD MILLION)

- TABLE 74 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET FOR FRUITS & VEGETABLES, BY REGION, 2026-2031 (USD MILLION)

- TABLE 75 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET FOR CEREALS & GRAINS, BY REGION, 2022-2025 (USD MILLION)

- TABLE 76 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET FOR CEREALS & GRAINS, BY REGION, 2026-2031 (USD MILLION)

- TABLE 77 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET FOR OTHER FOOD PRODUCTS, BY REGION, 2022-2025 (USD MILLION)

- TABLE 78 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET FOR OTHER FOOD PRODUCTS, BY REGION, 2026-2031 (USD MILLION)

- TABLE 79 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY SITE, 2022-2025 (USD MILLION)

- TABLE 80 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY SITE, 2026-2031 (USD MILLION)

- TABLE 81 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET IN-HOUSE LABORATORIES, BY REGION, 2022-2025 (USD MILLION)

- TABLE 82 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET IN-HOUSE LABORATORIES, BY REGION, 2026-2031 (USD MILLION)

- TABLE 83 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET IN OUTSOURCING FACILITIES, BY REGION, 2022-2025 (USD MILLION)

- TABLE 84 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET IN OUTSOURCING FACILITIES, BY REGION, 2026-2031 (USD MILLION)

- TABLE 85 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET IN GOVERNMENT LABS, BY REGION, 2022-2025 (USD MILLION)

- TABLE 86 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET IN GOVERNMENT LABS, BY REGION, 2026-2031 (USD MILLION)

- TABLE 87 KEY EMERGING RAPID DETECTION PLATFORMS FOR FOOD PATHOGEN TESTING

- TABLE 88 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 89 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 90 NORTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 91 NORTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 92 NORTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SYSTEM, 2022-2025 (USD MILLION)

- TABLE 93 NORTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SYSTEM, 2026-2031 (USD MILLION)

- TABLE 94 NORTH AMERICA: FOOD PATHOGEN SAFETY TESTING CONSUMABLES & KITS MARKET, BY SUBTYPE, 2022-2025 (USD MILLION)

- TABLE 95 NORTH AMERICA: FOOD PATHOGEN SAFETY TESTING CONSUMABLES & KITS MARKET, BY SUBTYPE, 2026-2031 (USD MILLION)

- TABLE 96 NORTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 97 NORTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 98 NORTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SITE, 2022-2025 (USD MILLION)

- TABLE 99 NORTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SITE, 2026-2031 (USD MILLION)

- TABLE 100 NORTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 101 NORTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY COUNTRY, 2026-2031 (USD MILLION)

- TABLE 102 US: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 103 US: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 104 CANADA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 105 CANADA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 106 MEXICO: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 107 MEXICO: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 108 EUROPE: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 109 EUROPE: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 110 EUROPE: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY SYSTEM, 2022-2025 (USD MILLION)

- TABLE 111 EUROPE: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY SYSTEM, 2026-2031 (USD MILLION)

- TABLE 112 EUROPE: FOOD PATHOGEN SAFETY TESTING CONSUMABLES & KITS MARKET, BY SUBTYPE, 2022-2025 (USD MILLION)

- TABLE 113 EUROPE: FOOD PATHOGEN SAFETY TESTING CONSUMABLES & KITS MARKET, BY SUBTYPE, 2026-2031 (USD MILLION)

- TABLE 114 EUROPE: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 115 EUROPE: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 116 EUROPE: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY SITE, 2022-2025 (USD MILLION)

- TABLE 117 EUROPE: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY SITE, 2026-2031 (USD MILLION)

- TABLE 118 EUROPE: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 119 EUROPE: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY COUNTRY, 2026-2031 (USD MILLION)

- TABLE 120 GERMANY: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 121 GERMANY: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 122 FRANCE: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 123 FRANCE: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 124 UK: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 125 UK: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 126 ITALY: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 127 ITALY: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 128 SPAIN: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 129 SPAIN: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 130 POLAND: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 131 POLAND: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 132 REST OF EUROPE: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 133 REST OF EUROPE: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 134 ASIA PACIFIC: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 135 ASIA PACIFIC: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 136 ASIA PACIFIC: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SYSTEM, 2022-2025 (USD MILLION)

- TABLE 137 ASIA PACIFIC: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SYSTEM, 2026-2031 (USD MILLION)

- TABLE 138 ASIA PACIFIC: FOOD PATHOGEN SAFETY TESTING CONSUMABLES & KITS MARKET, BY SUBTYPE, 2022-2025 (USD MILLION)

- TABLE 139 ASIA PACIFIC: FOOD PATHOGEN SAFETY TESTING CONSUMABLES & KITS MARKET, BY SUBTYPE, 2026-2031 (USD MILLION)

- TABLE 140 ASIA PACIFIC: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 141 ASIA PACIFIC: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 142 ASIA PACIFIC: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SITE, 2022-2025 (USD MILLION)

- TABLE 143 ASIA PACIFIC: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SITE, 2026-2031 (USD MILLION)

- TABLE 144 ASIA PACIFIC: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 145 ASIA PACIFIC: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY COUNTRY, 2026-2031 (USD MILLION)

- TABLE 146 CHINA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 147 CHINA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 148 JAPAN: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 149 JAPAN: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 150 INDIA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 151 INDIA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 152 AUSTRALIA & NEW ZEALAND: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 153 AUSTRALIA & NEW ZEALAND: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 154 SOUTHEAST ASIA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 155 SOUTHEAST ASIA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 156 REST OF ASIA PACIFIC: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 157 REST OF ASIA PACIFIC: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 158 SOUTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 159 SOUTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 160 SOUTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SYSTEM, 2022-2025 (USD MILLION)

- TABLE 161 SOUTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SYSTEM, 2026-2031 (USD MILLION)

- TABLE 162 SOUTH AMERICA: FOOD PATHOGEN SAFETY TESTING CONSUMABLES & KITS MARKET, BY SUBTYPE, 2022-2025 (USD MILLION)

- TABLE 163 SOUTH AMERICA: FOOD PATHOGEN SAFETY TESTING CONSUMABLES & KITS MARKET, BY SUBTYPE, 2026-2031 (USD MILLION)

- TABLE 164 SOUTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 165 SOUTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 166 SOUTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SITE, 2022-2025 (USD MILLION)

- TABLE 167 SOUTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SITE, 2026-2031 (USD MILLION)

- TABLE 168 SOUTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 169 SOUTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY COUNTRY, 2026-2031 (USD MILLION)

- TABLE 170 BRAZIL: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 171 BRAZIL: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 172 ARGENTINA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 173 ARGENTINA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 174 REST OF SOUTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 175 REST OF SOUTH AMERICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 176 ROW: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 177 ROW: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 178 ROW: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SYSTEM, 2022-2025 (USD MILLION)

- TABLE 179 ROW: FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET, BY SYSTEM, 2026-2031 (USD MILLION)

- TABLE 180 ROW: FOOD PATHOGEN SAFETY TESTING CONSUMABLES & KITS MARKET, BY SUBTYPE, 2022-2025 (USD MILLION)

- TABLE 181 ROW: FOOD PATHOGEN SAFETY TESTING CONSUMABLES & KITS MARKET, BY SUBTYPE, 2026-2031 (USD MILLION)

- TABLE 182 ROW: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 183 ROW: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 184 ROW: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY SITE, 2022-2025 (USD MILLION)

- TABLE 185 ROW: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY SITE, 2026-2031 (USD MILLION)

- TABLE 186 ROW: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 187 ROW: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 188 MIDDLE EAST: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 189 MIDDLE EAST: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 190 AFRICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2022-2025 (USD MILLION)

- TABLE 191 AFRICA: FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET, BY FOOD TESTED, 2026-2031 (USD MILLION)

- TABLE 192 OVERVIEW OF STRATEGIES ADOPTED BY KEY FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MANUFACTURERS

- TABLE 193 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET: DEGREE OF COMPETITION

- TABLE 194 FOOD PATHOGEN SAFETY EQUIPMENT & SUPPLIES MARKET: REGIONAL FOOTPRINT, 2025

- TABLE 195 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET: TYPE FOOTPRINT, 2025

- TABLE 196 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET: FOOD TESTED FOOTPRINT, 2025

- TABLE 197 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET: DETAILED LIST OF KEY STARTUPS/SMES, 2025

- TABLE 198 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES, 2025

- TABLE 199 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET: PRODUCT LAUNCHES, JANUARY 2022-FEBRUARY 2026

- TABLE 200 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET: DEALS, JANUARY 2022-FEBRUARY 2026

- TABLE 201 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET: EXPANSIONS, JANUARY 2022-FEBRUARY 2026

- TABLE 202 FOOD PATHOGEN SAFETY TESTING EQUIPMENT & SUPPLIES MARKET: OTHER DEVELOPMENTS, JANUARY 2022-FEBRUARY 2026

- TABLE 203 THERMO FISHER SCIENTIFIC, INC.: BUSINESS OVERVIEW

- TABLE 204 THERMO FISHER SCIENTIFIC INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 205 THERMO FISHER SCIENTIFIC INC.: DEALS

- TABLE 206 THERMO FISHER SCIENTIFIC INC.: EXPANSIONS

- TABLE 207 THERMO FISHER SCIENTIFIC INC.: OTHER DEVELOPMENTS

- TABLE 208 BIO-RAD LABORATORIES, INC.: BUSINESS OVERVIEW

- TABLE 209 BIO-RAD LABORATORIES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 210 BIO-RAD LABORATORIES, INC.: PRODUCT LAUNCHES

- TABLE 211 MERCK KGAA: BUSINESS OVERVIEW

- TABLE 212 MERCK KGAA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 213 MERCK KGAA: EXPANSIONS

- TABLE 214 NEOGEN CORPORATION: BUSINESS OVERVIEW

- TABLE 215 NEOGEN CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 216 NEOGEN CORPORATION: PRODUCT LAUNCHES

- TABLE 217 NEOGEN CORPORATION: DEALS

- TABLE 218 SHIMADZU CORPORATION: BUSINESS OVERVIEW

- TABLE 219 SHIMADZU CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 220 SHIMADZU CORPORATION: PRODUCT LAUNCHES

- TABLE 221 BIOMERIEUX: BUSINESS OVERVIEW

- TABLE 222 BIOMERIEUX: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 223 BIOMERIEUX: PRODUCT LAUNCHES

- TABLE 224 BIOMERIEUX: DEALS

- TABLE 225 AGILENT TECHNOLOGIES, INC.: BUSINESS OVERVIEW

- TABLE 226 AGILENT TECHNOLOGIES, INC.: PRODUCT/SOLUTION/SERVICES OFFERED

- TABLE 227 AGILENT TECHNOLOGIES, INC.: EXPANSIONS

- TABLE 228 QIAGEN: BUSINESS OVERVIEW

- TABLE 229 QIAGEN: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 230 QIAGEN: PRODUCT LAUNCHES

- TABLE 231 QIAGEN: DEALS

- TABLE 232 BRUKER: BUSINESS OVERVIEW

- TABLE 233 BRUKER: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 234 BRUKER: DEALS

- TABLE 235 PERKINELMER INC.: BUSINESS OVERVIEW

- TABLE 236 PERKINELMER INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 237 PERKINELMER INC.: PRODUCT LAUNCHES

- TABLE 238 PERKINELMER INC.: EXPANSIONS

- TABLE 239 HYGIENA, LLC: BUSINESS OVERVIEW

- TABLE 240 HYGIENA, LLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 241 HYGIENA, LLC: PRODUCT LAUNCHES

- TABLE 242 HYGIENA, LLC: DEALS

- TABLE 243 SOLABIA GROUP: BUSINESS OVERVIEW

- TABLE 244 SOLABIA GROUP: PRODUCT/SOLUTION/SERVICES OFFERED

- TABLE 245 SOLABIA GROUP: DEALS

- TABLE 246 ROKA BIO SCIENCE: BUSINESS OVERVIEW

- TABLE 247 ROKA BIO SCIENCE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 248 PROMEGA CORPORATION: BUSINESS OVERVIEW

- TABLE 249 PROMEGA CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 250 PROMEGA CORPORATION: DEALS

- TABLE 251 ROMER LABS DIVISION HOLDING: BUSINESS OVERVIEW

- TABLE 252 ROMER LABS DIVISION HOLDING: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 253 CHARM SCIENCES: BUSINESS OVERVIEW

- TABLE 254 CHARM SCIENCES: PRODUCT/SOLUTION/SERVICES OFFERED

- TABLE 255 CHARM SCIENCES: OTHER DEVELOPMENTS

- TABLE 256 MICROBIOLOGICS, INC.: BUSINESS OVERVIEW

- TABLE 257 MICROBIOLOGICS, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 258 MICROBIOLOGICS, INC.: DEALS

- TABLE 259 R-BIOPHARM: BUSINESS OVERVIEW

- TABLE 260 R-BIOPHARM: PRODUCT/SOLUTION/SERVICES OFFERED

- TABLE 261 R-BIOPHARM: DEALS

- TABLE 262 CONDALAB: BUSINESS OVERVIEW

- TABLE 263 CONDALAB: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 264 CHROMAGAR: BUSINESS OVERVIEW

- TABLE 265 CHROMAGAR: PRODUCT/SOLUTION/SERVICES OFFERED

- TABLE 266 GOLD STANDARD DIAGNOSTICS: BUSINESS OVERVIEW

- TABLE 267 CLEAR LABS, INC.: BUSINESS OVERVIEW

- TABLE 268 RING BIOTECHNOLOGY CO LTD.: BUSINESS OVERVIEW

- TABLE 269 NEMIS TECHNOLOGIES AG: BUSINESS OVERVIEW

- TABLE 270 PATHOGENDX CORPORATION: BUSINESS OVERVIEW

- TABLE 271 KEY DATA FROM PRIMARY SOURCES

- TABLE 272 RESEARCH ASSUMPTIONS

- TABLE 273 RESEARCH LIMITATIONS AND RISK ASSESSMENT

- TABLE 274 MARKETS ADJACENT TO FOOD PATHOGEN SAFETY TESTING EQUIPMENT AND SUPPLIES MARKET

- TABLE 275 FOOD SAFETY TESTING MARKET, BY TARGET TESTED, 2017-2021 (USD MILLION)

- TABLE 276 FOOD SAFETY TESTING MARKET, BY TARGET TESTED, 2022-2027 (USD MILLION)

- TABLE 277 FOOD DIAGNOSTICS MARKET, BY TYPE, 2018-2025 (USD MILLION)

List of Figures

2022-2031 2025 2026-2031 Value (USD million) and volume (no. of units) By Type, food tested, site, and technology (qualitative), and region North America, Europe, Asia Pacific, South America, and Rest of the World (RoW)