PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2050386

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2050386

Solid-state Transformers Market for US Data Centers, by Semiconductor Device Type (SiC-based, GaN-based), Deployment Type (New Installation, Retrofit/Replacement), Power Rating, Data Center Type, and Application - Forecast to 2030

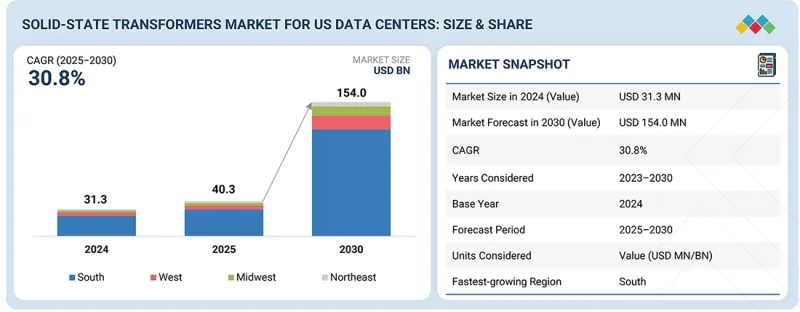

The solid-state transformers market for US data centers was valued at USD 40.3 million in 2025 and is projected to reach USD 154.0 million by 2030, growing at a CAGR of 30.8% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2019-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) |

| Segments | By Device Type, Depolyment and Region |

| Regions covered | North America, Europe, APAC, RoW |

"Based on semiconductor device type, the silicon carbide (SiC)-based segment is expected to witness the highest CAGR during the forecast period."

The silicon carbide (SiC)-based SST segment is expected to witness the highest CAGR in the solid-state transformers market for US data centers due to the increasing demand for high-efficiency power conversion systems. SiC-based devices support higher switching frequencies, lower energy losses, and improved thermal performance in high-density computing environments. These characteristics make SiC-based SSTs suitable for AI-driven hyperscale data centers requiring compact and energy-efficient electrical infrastructure. SiC technology also enables higher power density and supports fast voltage regulation across medium-voltage power distribution architectures. Increasing deployment of liquid-cooled AI clusters and high-capacity GPU servers is further accelerating the adoption of SiC-based solid-state transformers. In addition, growing investments in advanced power electronics and intelligent energy management systems are supporting segment growth across modern US data center facilities.

"Based on deployment type, the new installation segment is expected to account for the largest market share during the forecast period."

The new installation segment is expected to account for the largest share of the solid-state transformers market for US data centers due to the rapid construction of hyperscale and AI-driven facilities. Large data center operators are investing in next-generation electrical infrastructure to support increasing computing power demand. New installations allow operators to integrate medium-voltage SST architectures, intelligent power management systems, and modular electrical infrastructure from the initial design stage. These deployments also support higher energy efficiency, lower power losses, and improved space utilization across high-density environments. The growing development of liquid-cooled AI data centers and renewable-powered facilities is further accelerating demand for new SST deployments. In addition, increasing investment in scalable, grid-connected power infrastructure is supporting the adoption of solid-state transformers across newly constructed US data center campuses.

"The South region holds the largest market size during the forecast period."

The Southern US region is expected to hold the largest share of the solid-state transformers market for US data centers due to rapid hyperscale and AI infrastructure expansion. States such as Texas, Virginia, Georgia, and North Carolina are seeing significant investment in large-scale data center development projects. Growing availability of low-cost power, renewable energy capacity, and large land areas is supporting hyperscale data center construction across the region. Increasing deployment of AI clusters and high-density server environments is also accelerating demand for advanced medium-voltage power distribution systems. Additionally, rising integration of solar power, battery energy storage systems, and grid-connected backup infrastructure is creating demand for intelligent solid-state transformer technologies. Expanding investments in liquid-cooled AI facilities and modular electrical infrastructure are further supporting SST adoption across the Southern US data centers market.

Extensive primary interviews were conducted with key industry experts in the solid-state transformers market for US data centers to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is shown below.

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

- By Company Type - Tier 1 - 30%, Tier 2 - 35%, and Tier 3 - 35%

- By Designation - C-level Executives - 40%, Directors - 30%, and Others - 30%

- By Region - South - 40%, West - 28%, Midwest - 18%, and Northeast - 14%

The solid-state transformers market for US data centers is characterized by the presence of advanced power infrastructure providers and emerging power electronics companies. Key players include Hitachi Energy (Switzerland), Eaton (Ireland), DG Matrix (US), Heron Power (US), and Amperesand Technologies (Singapore), among others.

The study includes an in-depth competitive analysis of these key players in the solid-state transformers market for US data centers, covering company profiles, technology developments, power conversion innovations, strategic partnerships, and key growth strategies.

Study Coverage:

The report segments the solid-state transformers market for data centers and forecasts its size by Power Rating (<1 MVA, 1-5 MVA, 5-20 MVA, >20 MVA), Voltage Level (Low Voltage (<1 kV), Medium Voltage (1-35 kV), High Voltage (>35 kV)), Data Center Type (Hyperscale, Colocation, Enterprise & Edge), Semiconductor Device Type (Silicon Carbide (SiC)-based SST, Gallium Nitride (GaN)-based SST, Hybrid SST (SiC+GaN)), Deployment Type (New Installation, Retrofit/Replacement), Application (Power Distribution, Voltage Conversion/Conditioning, Renewable Integration, EV/Grid Integration), and Electrical Architecture (AC-based Architecture, Hybrid AC-DC Architecture, Fully DC Architecture). The report also analyses key market drivers, restraints, opportunities, and challenges influencing industry growth. It provides a detailed regional assessment across US regions, including the South, West, the Midwest, and the Northeast, along with country-level insights for major markets. In addition, the study includes value chain analysis and competitive landscape assessment of leading players operating in the solid-state transformer ecosystem.

Key Benefits of Buying the Report:

- Analysis of key drivers (increasing adoption of medium-voltage SST architectures in US AI-driven hyperscale data centers, rising demand for direct medium-voltage power distribution to high-density GPU clusters, growing need to reduce power conversion stages inside large-scale US facilities, increasing integration of battery energy storage systems with SST-enabled power routing platforms, and rising focus on improving power efficiency and reducing electrical infrastructure footprint across US data centers), restraints (high capital costs of SST deployment compared to conventional transformers and UPS systems in US data centers, limited commercial-scale SST implementation across operational US hyperscale facilities, complex replacement of legacy low-voltage electrical infrastructure, thermal stress in high-frequency SST power modules under continuous AI workloads, and limited availability of high-power SiC semiconductor components for large US data center applications), opportunities (growing construction of AI-focused liquid-cooled data centers in the US, increasing investments in software-defined power infrastructure, expansion of modular medium-voltage data center architectures, rising deployment of grid-interactive US data center campuses, and increasing interest in SST-enabled direct power distribution for next-generation US AI facilities), challenges (maintaining voltage stability during rapid AI workload fluctuations in US hyperscale environments, integration of SST systems with existing UPS and backup generator infrastructure, cooling requirements for high-frequency power electronics, ensuring long-term reliability under continuous high-load operations, and lack of standardized SST deployment frameworks across US hyperscale data centers).

- Product Development/Innovation: Detailed insights on emerging technologies, power semiconductor advancements such as silicon carbide (SiC) and gallium nitride (GaN), ongoing research and development activities, and new product developments in the solid-state transformers market for US data centers.

- Market Development: Comprehensive information about high-growth markets-the report analyzes the solid-state transformers market for US data centers across the South, West, Midwest, and Northeast.

- Market Diversification: Exhaustive information about emerging deployment models, renewable-integrated power systems, liquid-cooled AI facility infrastructure, modular electrical architectures, and expansion opportunities in the solid-state transformers market for US data centers.

- Competitive Assessment: In-depth assessment of market shares, technology positioning, and growth strategies of leading players such as DG Matrix (US), Heron Power Electronics Company (US), Amperesand Pte. Ltd. (Singapore), Hitachi Energy (Switzerland), and Eaton (Ireland), among others.

TABLE OF CONTENTS

1 INTRODUCTION

2 EXECUTIVE SUMMARY

3 PREMIUM INSIGHTS

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.2 RESTRAINTS

- 4.2.3 OPPORTUNITIES

- 4.2.4 CHALLENGES

- 4.3 PRICING ANALYSIS

- 4.3.1 AVERAGE SELLING PRICE ANALYSIS

- 4.3.2 COST STRUCTURE ANALYSIS OF SST

- 4.4 TECHNOLOGY TRENDS IN SST

- 4.5 SUPPLY CHAIN ANALYSIS OF SST

- 4.6 REGIONAL REGULATIONS AND COMPLIANCE

5 SST MARKET FOR US DATA CENTERS, BY VOLTAGE LEVEL (MARKET SIZE & FORECAST TO 2030 - USD MILLION)

- 5.1 INTRODUCTION

- 5.2 LOW VOLTAGE (<1 KV)

- 5.3 MEDIUM VOLTAGE (1-35 KV)

- 5.4 HIGH VOLTAGE (>35 KV)

6 SST MARKET FOR US DATA CENTERS, BY POWER RATING (MARKET SIZE & FORECAST TO 2030 - USD MILLION)

- 6.1 INTRODUCTION

- 6.2 <1 MVA

- 6.3 1-5 MVA

- 6.4 >5-20 MVA

- 6.5 >20 MVA

7 SST MARKET FOR US DATA CENTERS, BY DATA CENTER TYPE (MARKET SIZE & FORECAST TO 2030 - USD MILLION)

- 7.1 INTRODUCTION

- 7.2 HYPERSCALE

- 7.3 COLOCATION

- 7.4 ENTERPRISE & EDGE

8 SST MARKET FOR US DATA CENTERS, BY SEMICONDUCTOR DEVICE TYPE (MARKET SIZE & FORECAST TO 2030 - USD MILLION)

- 8.1 INTRODUCTION

- 8.2 SILICON CARBIDE (SIC)-BASED SST

- 8.3 GALLIUM NITRIDE (GAN)-BASED SST

- 8.4 HYBRID SST (SIC + GAN)

9 SST MARKET FOR US DATA CENTERS, BY APPLICATION (MARKET SIZE & FORECAST TO 2030 - USD MILLION)

- 9.1 INTRODUCTION

- 9.2 POWER DISTRIBUTION

- 9.3 VOLTAGE CONVERSION/CONDITIONING

- 9.4 RENEWABLE INTEGRATION

- 9.5 EV/GRID INTERACTION

10 SST MARKET FOR US DATA CENTERS, BY ELECTRICAL ARCHITECTURE (MARKET SIZE & FORECAST TO 2030 - USD MILLION)

- 10.1 INTRODUCTION

- 10.2 AC-BASED ARCHITECTURE

- 10.3 HYBRID AC-DC ARCHITECTURE

- 10.4 FULLY DC ARCHITECTURE

11 SST MARKET FOR US DATA CENTERS, BY REGION (MARKET SIZE & FORECAST TO 2030 - USD MILLION)

- 11.1 INTRODUCTION

- 11.2 US

- 11.2.1 SOUTH

- 11.2.2 WEST

- 11.2.3 MIDWEST

- 11.2.4 NORTHEAST

12 SST MARKET FOR US DATA CENTERS, COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 COMPETITOR ANALYSIS OF SST

- 12.3 MARKET SHARE ANALYSIS, 2024

- 12.4 COMPETITIVE SCENARIO

13 SST MARKET FOR US DATA CENTERS, COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 DG MATRIX

- 13.1.2 AMPERESAND PTE LTD

- 13.1.3 HERON POWER ELECTRONICS

- 13.2 OTHER PLAYERS

14 RESEARCH METHODOLOGY

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGE STORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS