PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2058128

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2058128

Data Center Storage Market By Storage Medium (SSDs, HDDs), Interface (SATA, SAS, NVMe), End User (Hyperscale/Cloud Service Providers, Enterprises, Government & Public Sector), Form Factor (3.5-inch, 2.5-inch, M.2), and Capacity - Global Forecast to 2032

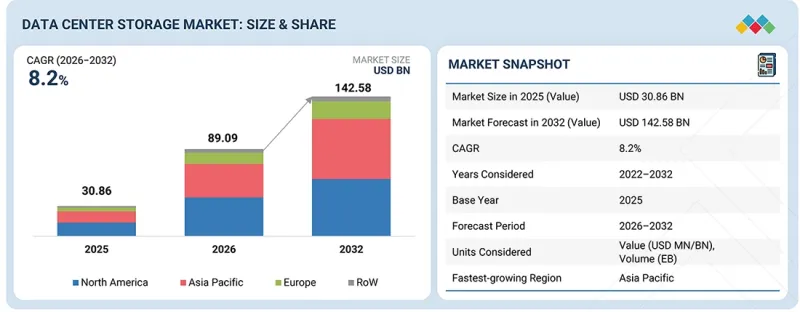

The data center storage market is projected to reach USD 142.58 billion by 2032 from an estimated USD 89.09 billion in 2026, growing at a CAGR of 8.2% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Storage Medium, End User and Region |

| Regions covered | North America, Europe, APAC, RoW |

"Based on end user, the hyperscale/cloud service providers segment is expected to witness the highest CAGR during the forecast period."

The hyperscale/cloud service providers segment is expected to witness the highest CAGR in the data center storage market, driven by increasing investments in hyperscale facilities, AI infrastructure, and large-scale cloud computing environments. These operators require high-capacity HDDs and high-performance SSDs to support massive data generation, AI training workloads, virtualization, and real-time analytics applications. Their growing focus on scalable, low-latency, and energy-efficient storage architectures is accelerating the deployment of advanced NVMe SSDs and ultra-high-capacity nearline HDDs. Additionally, expanding cloud adoption and increasing enterprise migration toward digital platforms are further driving storage infrastructure expansion across hyperscale environments.

"Based on deployment type, the cloud-based segment is expected to account for the largest market share during the forecast period."

The cloud-based segment accounts for the largest share of the data center storage market due to the increasing adoption of cloud computing platforms, hyperscale infrastructure expansion, and rising enterprise migration toward digital workloads. Cloud-based storage environments require scalable, high-capacity, and low-latency HDD and SSD solutions to support AI applications, virtualization, analytics, and real-time data processing workloads. The growing presence of hyperscale cloud providers and the increasing demand for flexible, remotely accessible storage infrastructure are accelerating the deployment of advanced data center storage technologies. Additionally, rising enterprise demand for cost-efficient and scalable storage architectures is further strengthening the adoption of cloud-based storage deployments globally.

"Asia Pacific is expected to account for the largest market share during the forecast period."

The Asia Pacific region accounts for the largest share of the data center storage market due to rapid hyperscale data center expansion, increasing cloud computing adoption, and rising AI infrastructure investments across major economies in the region. Growing enterprise digitalization and increasing internet penetration are accelerating demand for high-capacity HDDs and high-performance SSDs across cloud and enterprise environments. The strong presence of semiconductor manufacturing ecosystems and increasing investments by global cloud service providers are further supporting the large-scale deployment of advanced data center storage solutions across the Asia Pacific.

Extensive primary interviews were conducted with key industry experts in the data center storage market to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is shown below.

The study contains insights from various industry experts, including component suppliers, Tier 1 companies, and OEMs. The break-up of the primaries is as follows:

- By Company Type - Tier 1 - 40%, Tier 2 - 35%, and Tier 3 - 25%

- By Designation - C-level Executives - 35%, Directors - 40%, and Others - 25%

- By Region - North America - 30%, Europe - 20%, Asia Pacific - 40%, and RoW - 10%

The data center storage market is characterized by the presence of several established SSD and HDD manufacturers, such as Samsung (South Korea), SK HYNIX INC. (South Korea), Micron Technology, Inc. (US), KIOXIA Corporation (Japan), Sandisk Corporation (US), Seagate Technology LLC (Ireland), Western Digital Corporation (US), and Toshiba Electronic Devices & Storage Corporation (Japan), among others.

The study includes an in-depth competitive analysis of these key players in the data center storage market, covering their company profiles, recent developments, product innovations, storage technology advancements, and key market strategies.

Study Coverage:

The report segments the data center storage market and forecasts its size by storage medium (hard disk drives (HDDs), solid-state drives (SSDs)), interface (SATA, SAS, NVMe), capacity (low capacity (<2 TB), mid capacity (2-10 TB), high capacity (10-20 TB), ultra-high capacity (>20 TB)), form factor (3.5-inch, 2.5-inch, M.2, U.2/ U.3, EDSFF, Add-in-Cards (AICs)), deployment type (on-premises, cloud-based, hybrid), and end user (hyperscale/cloud service providers, enterprises, government & public sector). The report also analyses key market drivers, restraints, opportunities, and challenges influencing industry growth. It provides a detailed regional assessment across Asia Pacific, North America, Europe, and the RoW, along with country-level insights for major markets. In addition, the study includes a value chain analysis and a competitive landscape assessment of leading players in the global data center storage ecosystem.

Key Benefits of Buying the Report:

- Analysis of key drivers (increasing hyperscale data center deployments, rising adoption of AI and high-performance computing workloads, expanding cloud computing infrastructure, growing enterprise data generation, increasing demand for low-latency and high-capacity storage solutions), restraints (high capital investment requirements for advanced storage infrastructure, supply chain fluctuations in NAND flash and storage components, increasing power consumption and cooling requirements in large-scale data centers, pricing volatility in memory and storage devices), opportunities (growing AI server deployments, increasing adoption of edge computing infrastructure, rising demand for NVMe SSDs and ultra-high-capacity nearline HDDs, expansion of hyperscale and colocation data centers, increasing enterprise migration toward cloud-based storage architectures), challenges (thermal management and power efficiency concerns in high-density storage deployments, maintaining data reliability and endurance in AI-intensive workloads, complexities associated with scaling storage infrastructure for hyperscale environments, managing latency and performance requirements across data-intensive applications).

- Product Development/Innovation: Detailed insights on emerging storage technologies, advancements in NAND flash architectures, PCIe Gen5 and NVMe interface developments, ongoing research and development activities, and new product launches in the data center storage market.

- Market Development: Comprehensive information about high-growth markets-the report analyzes the data center storage market across North America, Europe, Asia Pacific, and the RoW.

- Market Diversification: Exhaustive information about new storage technologies, untapped application areas, strategic investments, and expansion opportunities in the data center storage market.

- Competitive Assessment: In-depth assessment of market shares and growth strategies of leading players, such as Samsung (South Korea), SK HYNIX INC. (South Korea), Micron Technology, Inc. (US), KIOXIA Corporation (Japan), Sandisk Corporation (US), Seagate Technology LLC(Ireland), Western Digital Corporation (US), and Toshiba Electronic Devices & Storage Corporation (Japan).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN DATA CENTER STORAGE MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DATA CENTER STORAGE MARKET

- 3.2 DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM

- 3.3 DATA CENTER STORAGE MARKET, BY INTERFACE

- 3.4 DATA CENTER STORAGE MARKET, BY CAPACITY

- 3.5 DATA CENTER STORAGE MARKET, BY FORM FACTOR

- 3.6 DATA CENTER STORAGE MARKET, BY DEPLOYMENT TYPE

- 3.7 DATA CENTER STORAGE MARKET, BY END USER

- 3.8 DATA CENTER STORAGE MARKET, BY REGION

- 3.9 DATA CENTER STORAGE MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing use of AI-, ML-, generative AI-driven workloads

- 4.2.1.2 Rapid expansion of hyperscale and cloud data centers

- 4.2.1.3 Pressing need to increase data storage capacity in data centers

- 4.2.1.4 Elevating demand for data storage systems with high throughput and low latency

- 4.2.2 RESTRAINTS

- 4.2.2.1 Requirement for high investment to modernize storage infrastructure

- 4.2.2.2 Substantial operating cost of storage infrastructure due to high power consumption

- 4.2.2.3 Volatile pricing of memory modules impacting large-scale procurement planning

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing adoption of AI-optimized storage infrastructure

- 4.2.3.2 Surging demand for distributed data center storage due to rising adoption of edge AI and real-time applications

- 4.2.3.3 Increasing adoption of software-defined storage architectures

- 4.2.3.4 Next-generation HDD innovations sustaining large-scale capacity expansion

- 4.2.4 CHALLENGES

- 4.2.4.1 Managing exponential growth of unstructured data

- 4.2.4.2 Scaling storage infrastructure without performance degradation

- 4.2.4.3 Increasing regulatory and cybersecurity pressures complicating storage operations

- 4.2.4.4 Component supply instability affecting storage manufacturing and deployment timelines

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.3.1 INTERCONNECTED MARKETS

- 4.3.2 CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 THREAT OF NEW ENTRANTS

- 5.2.2 THREAT OF SUBSTITUTES

- 5.2.3 BARGAINING POWER OF SUPPLIERS

- 5.2.4 BARGAINING POWER OF BUYERS

- 5.2.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.3 MACROECONOMIC OUTLOOK

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.3.3 TRENDS IN NAND FLASH MEMORY AND SEMICONDUCTOR INDUSTRIES

- 5.3.4 TRENDS IN DATA CENTER INFRASTRUCTURE AND STORAGE TECHNOLOGY MARKET

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF DATA CENTER STORAGE SOLTUIONS, BY STORAGE MEDIUM, 2022-2025

- 5.6.2 AVERAGE SELLING PRICE TREND OF DATA CENTER STORAGE MEDIUMS, BY REGION, 2022-2025

- 5.6.2.1 Average selling price trend of HDDs, by region, 2022-2025

- 5.6.2.2 Average selling price trend of SSDs, by region, 2022-2025

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 847170)

- 5.7.2 EXPORT SCENARIO (HS CODE 847170)

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO, 2022-2026

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 HYPERSCALE STORAGE DEPLOYMENTS FOR AI AND CLOUD WORKLOADS

- 5.11.2 CLOUD STORAGE MODERNIZATION FOR ENTERPRISE APPLICATIONS

- 5.11.3 HIGH-DENSITY STORAGE ARCHITECTURES FOR CONTENT DELIVERY AND AI APPLICATIONS

- 5.12 IMPACT OF US TARIFFS - DATA CENTER STORAGE MARKET

- 5.12.1 KEY TARIFF RATES

- 5.12.2 PRICE IMPACT ANALYSIS

- 5.12.3 IMPACT ON COUNTRIES/REGIONS

- 5.12.3.1 US

- 5.12.3.2 Europe

- 5.12.3.3 Asia Pacific

- 5.12.4 IMPACT ON END USERS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 3D NAND SCALING AND LAYER INNOVATIONS

- 6.1.2 AI-OPTIMIZED DATA CENTER SSD ARCHITECTURES

- 6.1.3 ZONED STORAGE TECHNOLOGIES

- 6.1.4 COMPUTATIONAL STORAGE AND IN-STORAGE PROCESSING

- 6.1.5 NEXT-GENERATION HDD TECHNOLOGIES

- 6.1.6 NVME AND PCIE GEN5/GEN6 STORAGE INTERFACES

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 DATA PROCESSING UNITS AND SMARTNICS

- 6.2.2 NVME-OVER-FABRICS AND RDMA NETWORKING

- 6.2.3 ADVANCED COOLING AND THERMAL MANAGEMENT TECHNOLOGIES

- 6.2.4 DATA SECURITY, ENCRYPTION, AND RANSOMWARE PROTECTION TECHNOLOGIES

- 6.2.5 STORAGE VIRTUALIZATION AND COMPOSABLE INFRASTRUCTURE

- 6.2.6 STORAGE POWER OPTIMIZATION AND ENERGY-EFFICIENT ARCHITECTURES

- 6.3 TECHNOLOGY ROADMAP

- 6.3.1 SHORT-TERM (2025-2027): PERFORMANCE OPTIMIZATION AND AI INFRASTRUCTURE SCALING

- 6.3.2 MID-TERM (2027-2030): COMPOSABLE STORAGE AND DISAGGREGATED INFRASTRUCTURE

- 6.3.3 LONG-TERM (2030-2035+): INTELLIGENT STORAGE INFRASTRUCTURE AND AUTONOMOUS DATA MANAGEMENT

- 6.4 PATENT ANALYSIS

- 6.5 IMPACT OF AI ON DATA CENTER STORAGE MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS/OEMS IN DATA CENTER STORAGE MARKET

- 6.5.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN DATA CENTER STORAGE MARKET

- 6.5.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED DATA CENTER STORAGE

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 INTRODUCTION

- 7.2 REGIONAL REGULATIONS AND COMPLIANCE

- 7.2.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2.2 INDUSTRY STANDARDS

- 7.2.2.1 Storage interface and performance standards (NVMe, PCIe, SATA, SAS)

- 7.2.2.2 Data security and cybersecurity standards (ISO/IEC 27001, NIST)

- 7.2.2.3 Energy efficiency and sustainability standards (ENERGY STAR, ISO 50001)

- 7.2.2.4 Storage interoperability and form factor standards (SNIA, OCP, EDSFF)

- 7.3 SUSTAINABILITY INITIATIVES

- 7.3.1 USE OF DATA CENTER STORAGE SOLUTIONS TO REDUCE ENVIRONMENTAL IMPACT

- 7.3.2 ENERGY-EFFICIENT STORAGE ARCHITECTURES AND POWER OPTIMIZATION

- 7.3.3 ELECTRONIC WASTE MANAGEMENT AND RECYCLING INITIATIVES

- 7.3.4 SUSTAINABLE DATA CENTER INFRASTRUCTURE AND CARBON REDUCTION INITIATIVES

- 7.4 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4.1 IMPACT OF ENVIRONMENTAL REGULATIONS ON DATA CENTER STORAGE DESIGN

- 7.4.2 IMPACT OF ENERGY EFFICIENCY POLICIES ON DATA CENTER OPERATIONS

- 7.4.3 IMPACT OF ELECTRONIC WASTE AND RECYCLING REGULATIONS

- 7.4.4 IMPACT OF DATA SECURITY AND DATA LOCALIZATION POLICIES

- 7.5 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

- 7.5.1 PRODUCT SAFETY AND REGULATORY CERTIFICATION

- 7.5.2 ENVIRONMENTAL COMPLIANCE AND HAZARDOUS SUBSTANCE REGULATIONS

- 7.5.3 ENERGY EFFICIENCY AND ENVIRONMENTAL LABELING PROGRAMS

- 7.5.4 ELECTRONIC WASTE MANAGEMENT AND RECYCLING COMPLIANCE

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.5 UNMET NEEDS OF VARIOUS END USERS

9 DATA CENTER STORAGE LANDSCAPE, BY WORKLOAD TYPE

- 9.1 INTRODUCTION

- 9.2 AI/ML WORKLOADS

- 9.2.1 TRAINING

- 9.2.2 INFERENCE

- 9.3 GENERAL-PURPOSE WORKLOADS

10 STORAGE ARCHITECTURES IN DATA CENTERS

- 10.1 INTRODUCTION

- 10.2 DIRECT-ATTACHED STORAGE (DAS)

- 10.3 NETWORK-ATTACHED STORAGE (NAS)

- 10.4 STORAGE AREA NETWORK (SAN)

11 STORAGE SYSTEM CONFIGURATIONS IN DATA CENTERS

- 11.1 INTRODUCTION

- 11.2 ALL-FLASH ARRAYS

- 11.3 ALL-HDD ARRAYS

- 11.4 HYBRID ARRAYS (HDD + SSD)

12 DATA STORAGE TYPES IN DATA CENTERS

- 12.1 INTRODUCTION

- 12.2 BLOCK STORAGE

- 12.3 FILE STORAGE

- 12.4 OBJECT STORAGE

13 DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM

- 13.1 INTRODUCTION

- 13.2 HARD DISK DRIVES

- 13.2.1 CONVENTIONAL MAGNETIC RECORDING

- 13.2.1.1 Increasing demand for reliable large-scale storage to accelerate adoption

- 13.2.2 SHINGLED MAGNETIC RECORDING

- 13.2.2.1 Higher storage density and archival data expansion to support segmental growth

- 13.2.1 CONVENTIONAL MAGNETIC RECORDING

- 13.3 SOLID-STATE DRIVES

- 13.3.1 SINGLE-LEVEL CELL

- 13.3.1.1 High endurance and ultra-low latency features to drive adoption

- 13.3.2 MULTI-LEVEL CELL

- 13.3.2.1 Suitability for performance-sensitive enterprise applications to stimulate demand

- 13.3.3 TRIPLE-LEVEL CELL

- 13.3.3.1 Potential to improve application responsiveness and reduce storage latency to spike demand

- 13.3.4 QUAD-LEVEL CELL

- 13.3.4.1 Increasing demand for high-capacity flash storage with improved energy efficiency to contribute to segmental growth

- 13.3.1 SINGLE-LEVEL CELL

14 DATA CENTER STORAGE MARKET, BY INTERFACE

- 14.1 INTRODUCTION

- 14.2 SATA

- 14.2.1 MATURE ECOSYSTEM AND LOWER IMPLEMENTATION COST TO BOOST DEMAND

- 14.3 SAS

- 14.3.1 RISING USE IN MISSION-CRITICAL STORAGE ARRAYS AND TRANSACTIONAL DATABASES TO SUPPORT SEGMENTAL GROWTH

- 14.4 NVME

- 14.4.1 ABILITY TO HANDLE MASSIVE PARALLEL INPUT/OUTPUT OPERATIONS WITH MINIMAL PROTOCOL OVERHEAD TO PROPEL MARKET

15 DATA CENTER STORAGE MARKET, BY CAPACITY

- 15.1 INTRODUCTION

- 15.2 LOW CAPACITY (<2 TB)

- 15.2.1 BOOT INFRASTRUCTURE AND EDGE DEPLOYMENTS TO SUSTAIN DEMAND FOR LOW-CAPACITY DATA CENTER STORAGE SOLUTIONS

- 15.3 MID CAPACITY (2-10 TB)

- 15.3.1 ENTERPRISE VIRTUALIZATION AND MIXED-WORKLOAD INFRASTRUCTURE TO DRIVE DEPLOYMENT

- 15.4 HIGH CAPACITY (10-20 TB)

- 15.4.1 CONTINUED EXPANSION OF CLOUD-NATIVE APPLICATIONS TO ACCELERATE DEMAND

- 15.5 ULTRA-HIGH CAPACITY (>20 TB)

- 15.5.1 HYPERSCALE DATA EXPANSION AND AI STORAGE CONSOLIDATION TO DRIVE ADOPTION

16 DATA CENTER STORAGE MARKET, BY FORM FACTOR

- 16.1 INTRODUCTION

- 16.2 3.5 INCH

- 16.2.1 BULK DATA RETENTION AND HYPERSCALE CLOUD EXPANSION TO SUSTAIN SEGMENTAL GROWTH

- 16.3 2.5 INCH

- 16.3.1 ENTERPRISE SSD EXPANSION AND SPACE-EFFICIENT SERVER DESIGN TO ACCELERATE DEMAND

- 16.4 M.2

- 16.4.1 COMPACT SERVER ARCHITECTURES AND CONTINUED GROWTH OF EDGE INFRASTRUCTURE TO BOOST DEMAND

- 16.5 U.2/U.3

- 16.5.1 NEED FOR CONTINUOUS UPTIME AND SIMPLIFIED MAINTENANCE IN ENTERPRISES TO SPUR DEMAND

- 16.6 EDSFF

- 16.6.1 AI SERVER DENSITY REQUIREMENTS TO CONTRIBUTE TO SEGMENTAL GROWTH

- 16.7 ADD-IN CARDS (AICS)

- 16.7.1 ULTRA-LOW LATENCY COMPUTING AND GPU-CENTRIC INFRASTRUCTURE TO SUPPORT SEGMENTAL GROWTH

17 DATA CENTER STORAGE MARKET, BY DEPLOYMENT TYPE

- 17.1 INTRODUCTION

- 17.2 ON-PREMISES

- 17.2.1 REGULATORY COMPLIANCE AND OPERATIONAL SECURITY REQUIREMENTS TO SPIKE DEMAND

- 17.3 CLOUD-BASED

- 17.3.1 ENTERPRISE CLOUD MIGRATION AND HYPERSCALE DATA CENTER INVESTMENTS TO EXPEDITE SEGMENTAL GROWTH

- 17.4 HYBRID

- 17.4.1 ENTERPRISE WORKLOAD FLEXIBILITY AND MULTI-CLOUD STRATEGIES TO ELEVATE HYBRID DEPLOYMENTS

18 DATA CENTER STORAGE MARKET, BY END USER

- 18.1 INTRODUCTION

- 18.2 HYPERSCALE/CLOUD SERVICE PROVIDERS

- 18.2.1 RAPID EXPANSION OF AI SERVICES, CLOUD-NATIVE APPLICATIONS, AND HYPERSCALE INFRASTRUCTURE TO PROPEL MARKET

- 18.3 ENTERPRISES

- 18.3.1 BFSI

- 18.3.1.1 Rising use of AI models in fraud monitoring, risk analysis, and credit scoring applications to drive market

- 18.3.2 IT & TELECOM

- 18.3.2.1 Elevating adoption of AI for network optimization, predictive maintenance, and customer analytics to support market growth

- 18.3.3 HEALTHCARE

- 18.3.3.1 Increasing digitalization of patient care, clinical workflows, diagnostics, and healthcare analytics to fuel market growth

- 18.3.4 RETAIL & E-COMMERCE

- 18.3.4.1 Rising focus of retailers on analyzing customer behavior and purchasing patterns to create growth opportunities

- 18.3.5 MANUFACTURING

- 18.3.5.1 Escalating use of AI models in equipment monitoring, production optimization, and defect detection applications to fuel market growth

- 18.3.6 ENERGY & UTILITIES

- 18.3.6.1 Growing adoption of smart grid infrastructure and connected utility networks to facilitate market growth

- 18.3.7 AUTOMOTIVE

- 18.3.7.1 Increasing deployment of AI and ML models across automotive operations to foster market growth

- 18.3.8 OTHER ENTERPRISES

- 18.3.1 BFSI

- 18.4 GOVERNMENT & PUBLIC SECTOR

- 18.4.1 SOVEREIGN DATA INFRASTRUCTURE AND NATIONAL DIGITALIZATION PROGRAMS TO SPUR DEMAND

19 DATA CENTER STORAGE MARKET, BY REGION

- 19.1 INTRODUCTION

- 19.2 NORTH AMERICA

- 19.2.1 US

- 19.2.1.1 Rising investments in hyperscale data center expansion initiatives to drive market

- 19.2.2 CANADA

- 19.2.2.1 Expansion of sustainable data centers and cloud infrastructure to spike demand

- 19.2.3 MEXICO

- 19.2.3.1 Increasing colocation investments and nearshore digital expansion to accelerate adoption

- 19.2.1 US

- 19.3 EUROPE

- 19.3.1 GERMANY

- 19.3.1.1 Elevating adoption of Industry 4.0, IIOT, and AI-driven manufacturing systems to contribute to market growth

- 19.3.2 UK

- 19.3.2.1 Increasing deployment of edge computing infrastructure for 5G networks and low-latency applications to fuel market growth

- 19.3.3 FRANCE

- 19.3.3.1 Government-led digital infrastructure initiatives to foster market growth

- 19.3.4 NETHERLANDS

- 19.3.4.1 Escalating adoption of AI-enabled analytics platforms to create growth opportunities

- 19.3.5 RUSSIA

- 19.3.5.1 Focus on enhancing domestic semiconductor and IT ecosystem development to strengthen demand

- 19.3.6 ITALY

- 19.3.6.1 Shift from legacy IT to integrated digital operations to contribute to market expansion

- 19.3.7 POLAND

- 19.3.7.1 Expanding role in fintech operations and e-commerce fulfillment to create lucrative growth opportunities

- 19.3.8 SPAIN

- 19.3.8.1 Increasing data generation from digital banking, OTT, and mobile applications to facilitate market growth

- 19.3.9 SWITZERLAND

- 19.3.9.1 Large volumes of transactional records, encrypted datasets, and real-time financial processing workloads to propel market

- 19.3.10 SWEDEN

- 19.3.10.1 High-volume data generation due to rising use of gaming and engineering simulation platforms to stimulate demand

- 19.3.11 BELGIUM

- 19.3.11.1 Cross-border enterprise activity to support storage infrastructure expansion

- 19.3.12 REST OF EUROPE

- 19.3.1 GERMANY

- 19.4 ASIA PACIFIC

- 19.4.1 CHINA

- 19.4.1.1 Continuous growth in e-commerce, online entertainment, and smart manufacturing platforms to accelerate market growth

- 19.4.2 AUSTRALIA

- 19.4.2.1 Renewable energy expansion and enterprise cloud migration to support market expansion

- 19.4.3 JAPAN

- 19.4.3.1 Pressing need for highly stable and predictable data processing architectures in automated factories to create growth momentum

- 19.4.4 INDIA

- 19.4.4.1 Rapidly expanding digital economy and large-scale internet consumption patterns to boost demand

- 19.4.5 SINGAPORE

- 19.4.5.1 Limited land availability and regional data exchange density to drive demand for high-value storage deployments

- 19.4.6 INDONESIA

- 19.4.6.1 Surging demand for e-commerce applications, digital wallets, online gaming, and video streaming services to fuel market growth

- 19.4.7 NEW ZEALAND

- 19.4.7.1 Transition from fragmented systems to cohesive cloud solutions to foster market growth

- 19.4.8 SOUTH KOREA

- 19.4.8.1 Strong semiconductor manufacturing base to create market expansion opportunities

- 19.4.9 REST OF ASIA PACIFIC

- 19.4.1 CHINA

- 19.5 ROW

- 19.5.1 SOUTH AMERICA

- 19.5.1.1 Brazil

- 19.5.1.1.1 Growing importance of digital transactions in financial services, retail, and telecommunications sectors to propel market

- 19.5.1.2 Rest of South America

- 19.5.1.1 Brazil

- 19.5.2 MIDDLE EAST & AFRICA

- 19.5.2.1 GCC

- 19.5.2.1.1 National digital diversification programs and sovereign cloud investments to accelerate demand

- 19.5.2.2 South Africa

- 19.5.2.2.1 Financial services expansion and regional connectivity infrastructure to fuel market growth

- 19.5.2.3 Rest of Middle East & Africa

- 19.5.2.1 GCC

- 19.5.1 SOUTH AMERICA

20 COMPETITIVE LANDSCAPE

- 20.1 OVERVIEW

- 20.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2022-2026

- 20.3 REVENUE ANALYSIS, 2021-2025

- 20.4 MARKET SHARE ANALYSIS, 2025

- 20.5 COMPANY VALUATION AND FINANCIAL METRICS, 2025

- 20.6 COMPANY EVALUATION MATRIX, 2025

- 20.6.1 COMPANY EVALUATION MATRIX: PUREPLAY SSD VENDORS, 2025

- 20.6.1.1 Stars

- 20.6.1.2 Emerging leaders

- 20.6.1.3 Pervasive players

- 20.6.1.4 Participants

- 20.6.2 COMPANY EVALUATION MATRIX: NAND-INDEPENDENT SSD VENDORS, 2025

- 20.6.2.1 Stars

- 20.6.2.2 Emerging leaders

- 20.6.2.3 Pervasive players

- 20.6.2.4 Participants

- 20.6.3 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 20.6.3.1 Company footprint

- 20.6.3.2 Region footprint

- 20.6.3.3 Interface footprint

- 20.6.3.4 Capacity footprint

- 20.6.3.5 Deployment type footprint

- 20.6.3.6 End user footprint

- 20.6.1 COMPANY EVALUATION MATRIX: PUREPLAY SSD VENDORS, 2025

- 20.7 BRAND COMPARISON

- 20.7.1 SAMSUNG (SOUTH KOREA)

- 20.7.2 MICRON TECHNOLOGY, INC. (US)

- 20.7.3 SK HYNIX INC. (SOUTH KOREA)

- 20.7.4 KIOXIA HOLDINGS CORPORATION (JAPAN)

- 20.7.5 SANDISK CORPORATION (US)

- 20.8 COMPETITIVE SCENARIO

- 20.8.1 PRODUCT LAUNCHES

- 20.8.2 DEALS

21 COMPANY PROFILES

- 21.1 INTRODUCTION

- 21.2 KEY PLAYERS

- 21.2.1 SAMSUNG

- 21.2.1.1 Business overview

- 21.2.1.2 Products offered

- 21.2.1.3 Recent developments

- 21.2.1.3.1 Product launches

- 21.2.1.4 MnM view

- 21.2.1.4.1 Key strengths/Right to win

- 21.2.1.4.2 Strategic choices

- 21.2.1.4.3 Weaknesses/Competitive threats

- 21.2.2 MICRON TECHNOLOGY, INC.

- 21.2.2.1 Business overview

- 21.2.2.2 Products offered

- 21.2.2.3 Recent developments

- 21.2.2.3.1 Product launches

- 21.2.2.4 MnM view

- 21.2.2.4.1 Key strengths/Right to win

- 21.2.2.4.2 Strategic choices

- 21.2.2.4.3 Weaknesses/Competitive threats

- 21.2.3 KIOXIA HOLDINGS CORPORATION

- 21.2.3.1 Business overview

- 21.2.3.2 Products offered

- 21.2.3.3 Recent developments

- 21.2.3.3.1 Product launches

- 21.2.3.4 MnM view

- 21.2.3.4.1 Key strengths/Right to win

- 21.2.3.4.2 Strategic choices

- 21.2.3.4.3 Weaknesses/Competitive threats

- 21.2.4 SK HYNIX INC.

- 21.2.4.1 Business overview

- 21.2.4.2 Products offered

- 21.2.4.3 Recent developments

- 21.2.4.3.1 Product launches

- 21.2.4.4 MnM view

- 21.2.4.4.1 Key strengths/Right to win

- 21.2.4.4.2 Strategic choices

- 21.2.4.4.3 Weaknesses/Competitive threats

- 21.2.5 SANDISK CORPORATION

- 21.2.5.1 Business overview

- 21.2.5.2 Products offered

- 21.2.5.3 Recent developments

- 21.2.5.3.1 Deals

- 21.2.5.4 MnM view

- 21.2.5.4.1 Key strengths/Right to win

- 21.2.5.4.2 Strategic choices

- 21.2.5.4.3 Weaknesses/Competitive threats

- 21.2.6 SEAGATE TECHNOLOGY LLC

- 21.2.6.1 Business overview

- 21.2.6.2 Products offered

- 21.2.6.3 Recent developments

- 21.2.6.3.1 Product launches

- 21.2.6.4 MnM view

- 21.2.6.4.1 Key strengths/Right to win

- 21.2.6.4.2 Strategic choices

- 21.2.6.4.3 Weaknesses/Competitive threats

- 21.2.7 WESTERN DIGITAL CORPORATION

- 21.2.7.1 Business overview

- 21.2.7.2 Products offered

- 21.2.7.3 Recent developments

- 21.2.7.3.1 Product launches

- 21.2.7.3.2 Other developments

- 21.2.7.4 MnM view

- 21.2.7.4.1 Key strengths/Right to win

- 21.2.7.4.2 Strategic choices

- 21.2.7.4.3 Weaknesses/Competitive threats

- 21.2.8 TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION

- 21.2.8.1 Business overview

- 21.2.8.2 Products offered

- 21.2.8.3 Recent developments

- 21.2.8.3.1 Product launches

- 21.2.8.4 MnM view

- 21.2.8.4.1 Key strengths/Right to win

- 21.2.8.4.2 Strategic choices

- 21.2.8.4.3 Weaknesses/Competitive threats

- 21.2.1 SAMSUNG

- 21.3 OTHER PLAYERS

- 21.3.1 BEIJING MEMBLAZE TECHNOLOGY CO., LTD.

- 21.3.2 DAPUSTOR CORPORATION

- 21.3.3 SCALEFLUX, INC.

- 21.3.4 SHENZHEN UNIONMEMORY INFORMATION SYSTEM LIMITED

- 21.3.5 NIMBUS DATA

- 21.3.6 KINGSTON TECHNOLOGY

- 21.3.7 PENGUIN SOLUTIONS

- 21.3.8 ATP ELECTRONICS, INC.

- 21.3.9 INNODISK CORPORATION

- 21.3.10 APACER TECHNOLOGY INC.

- 21.3.11 VIRTIUM

- 21.3.12 SWISSBIT AG

- 21.3.13 BIWIN STORAGE TECHNOLOGY CO., LTD.

- 21.3.14 FADU INC.

- 21.3.15 YMTC

- 21.3.16 VIKING ENTERPRISE SOLUTIONS

- 21.3.17 PHISON ELECTRONICS

22 RESEARCH METHODOLOGY

- 22.1 RESEARCH DATA

- 22.1.1 SECONDARY AND PRIMARY RESEARCH

- 22.1.2 SECONDARY DATA

- 22.1.2.1 List of key secondary sources

- 22.1.2.2 Key data from secondary sources

- 22.1.3 PRIMARY DATA

- 22.1.3.1 List of primary interview participants

- 22.1.3.2 Breakdown of primaries

- 22.1.3.3 Key data from primary sources

- 22.1.3.4 Key industry insights

- 22.2 MARKET SIZE ESTIMATION

- 22.2.1 BOTTOM-UP APPROACH

- 22.2.1.1 Approach to estimate market size using bottom-up analysis (demand side)

- 22.2.2 TOP-DOWN APPROACH

- 22.2.2.1 Approach to estimate market size using top-down analysis (supply side)

- 22.2.1 BOTTOM-UP APPROACH

- 22.3 DATA TRIANGULATION

- 22.4 RESEARCH ASSUMPTIONS

- 22.5 RESEARCH LIMITATIONS

- 22.6 RISK ASSESSMENT

23 APPENDIX

- 23.1 INSIGHTS FROM INDUSTRY EXPERTS

- 23.2 DISCUSSION GUIDE

- 23.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 23.4 CUSTOMIZATION OPTIONS

- 23.5 RELATED REPORTS

- 23.6 AUTHOR DETAILS

List of Tables

- TABLE 1 REPORT INCLUSIONS AND EXCLUSIONS

- TABLE 2 KEY STRATEGIC MOVES, BY COMPANY TYPE

- TABLE 3 DATA CENTER STORAGE MARKET: IMPACT OF PORTER'S FIVE FORCES

- TABLE 4 GDP PERCENTAGE CHANGE, BY KEY COUNTRY, 2021-2029

- TABLE 5 ROLE OF PLAYERS IN DATA CENTER STORAGE ECOSYSTEM

- TABLE 6 AVERAGE SELLING PRICE TREND OF DATA CENTER STORAGE SOLUTIONS, BY STORAGE MEDIUM, 2022-2025 (USD/TB)

- TABLE 7 AVERAGE SELLING PRICE TREND OF HDDS, BY REGION, 2022-2025 (USD/TB)

- TABLE 8 AVERAGE SELLING PRICE TREND OF SSDS, BY REGION, 2022-2025 (USD/TB)

- TABLE 9 IMPORT DATA FOR HS CODE 847170-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 10 EXPORT DATA FOR HS CODE 847170-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 11 DATA CENTER STORAGE MARKET: KEY CONFERENCES AND EVENTS, 2026-2027

- TABLE 12 GOOGLE DEPLOYS AI-OPTIMIZED STORAGE INFRASTRUCTURE TO SUPPORT LARGE-SCALE AI AND CLOUD WORKLOADS

- TABLE 13 MICROSOFT EXPANDS CLOUD STORAGE INFRASTRUCTURE TO SUPPORT ENTERPRISE AND AI WORKLOADS

- TABLE 14 META ADOPTS HIGH-DENSITY STORAGE INFRASTRUCTURE FOR AI AND CONTENT DELIVERY WORKLOADS

- TABLE 15 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 16 DATA CENTER STORAGE MARKET: LIST OF GRANTED PATENTS, JANUARY 2021-DECEMBER 2025

- TABLE 17 TOP USE CASES AND MARKET POTENTIAL

- TABLE 18 BEST PRACTICES ADOPTED BY MARKET PLAYERS

- TABLE 19 DATA CENTER STORAGE MARKET: CASE STUDIES RELATED TO AI IMPLEMENTATION

- TABLE 20 INTERCONNECTED ECOSYSTEM AND INFLUENCE ON MARKET PLAYERS

- TABLE 21 CLIENTS' READINESS TO ADOPT AI-POWERED DATA CENTER STORAGE SOLUTIONS

- TABLE 22 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 23 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 24 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 25 ROW: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 26 CERTIFICATIONS, LABELING, AND ECO-STANDARDS IN DATA CENTER STORAGE MARKET

- TABLE 27 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR END USERS (%)

- TABLE 28 KEY BUYING CRITERIA FOR END USERS

- TABLE 29 UNMET NEEDS IN DATA CENTER STORAGE MARKET, BY END USER

- TABLE 30 DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2022-2025 (USD MILLION)

- TABLE 31 DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2026-2032 (USD MILLION)

- TABLE 32 DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2022-2025 (EB)

- TABLE 33 DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2026-2032 (EB)

- TABLE 34 HARD DISK DRIVES: DATA CENTER STORAGE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 35 HARD DISK DRIVES: DATA CENTER STORAGE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 36 HARD DISK DRIVES: DATA CENTER STORAGE MARKET, BY INTERFACE, 2022-2025 (USD MILLION)

- TABLE 37 HARD DISK DRIVES: DATA CENTER STORAGE MARKET, BY INTERFACE, 2026-2032 (USD MILLION)

- TABLE 38 HARD DISK DRIVES: DATA CENTER STORAGE MARKET, BY CAPACITY, 2022-2025 (USD MILLION)

- TABLE 39 HARD DISK DRIVES: DATA CENTER STORAGE MARKET, BY CAPACITY, 2026-2032 (USD MILLION)

- TABLE 40 HARD DISK DRIVES: DATA CENTER STORAGE MARKET, BY FORM FACTOR, 2022-2025 (USD MILLION)

- TABLE 41 HARD DISK DRIVES: DATA CENTER STORAGE MARKET, BY FORM FACTOR, 2026-2032 (USD MILLION)

- TABLE 42 SOLID-STATE DRIVES: DATA CENTER STORAGE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 43 SOLID-STATE DRIVES: DATA CENTER STORAGE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 44 SOLID-STATE DRIVES: DATA CENTER STORAGE MARKET, BY INTERFACE, 2022-2025 (USD MILLION)

- TABLE 45 SOLID-STATE DRIVES: DATA CENTER STORAGE MARKET, BY INTERFACE, 2026-2032 (USD MILLION)

- TABLE 46 SOLID-STATE DRIVES: DATA CENTER STORAGE MARKET, BY CAPACITY, 2022-2025 (USD MILLION)

- TABLE 47 SOLID-STATE DRIVES: DATA CENTER STORAGE MARKET, BY CAPACITY, 2026-2032 (USD MILLION)

- TABLE 48 SOLID-STATE DRIVES: DATA CENTER STORAGE MARKET, BY FORM FACTOR, 2022-2025 (USD MILLION)

- TABLE 49 SOLID-STATE DRIVES: DATA CENTER STORAGE MARKET, BY FORM FACTOR, 2026-2032 (USD MILLION)

- TABLE 50 DATA CENTER STORAGE MARKET, BY INTERFACE, 2022-2025 (USD MILLION)

- TABLE 51 DATA CENTER STORAGE MARKET, BY INTERFACE, 2026-2032 (USD MILLION)

- TABLE 52 SATA: DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2022-2025 (USD MILLION)

- TABLE 53 SATA: DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2026-2032 (USD MILLION)

- TABLE 54 SAS: DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2022-2025 (USD MILLION)

- TABLE 55 SAS: DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2026-2032 (USD MILLION)

- TABLE 56 NVME: DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2022-2025 (USD MILLION)

- TABLE 57 NVME: DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2026-2032 (USD MILLION)

- TABLE 58 DATA CENTER STORAGE MARKET, BY CAPACITY, 2022-2025 (USD MILLION)

- TABLE 59 DATA CENTER STORAGE MARKET, BY CAPACITY, 2026-2032 (USD MILLION)

- TABLE 60 LOW CAPACITY (<2 TB): DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2022-2025 (USD MILLION)

- TABLE 61 LOW CAPACITY (<2 TB): DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2026-2032 (USD MILLION)

- TABLE 62 MID CAPACITY (2-10 TB): DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2022-2025 (USD MILLION)

- TABLE 63 MID CAPACITY (2-10 TB): DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2026-2032 (USD MILLION)

- TABLE 64 HIGH CAPACITY (10-20 TB): DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2022-2025 (USD MILLION)

- TABLE 65 HIGH CAPACITY (10-20 TB): DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2026-2032 (USD MILLION)

- TABLE 66 ULTRA-HIGH CAPACITY (>20 TB): DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2022-2025 (USD MILLION)

- TABLE 67 ULTRA-HIGH CAPACITY (>20 TB): DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2026-2032 (USD MILLION)

- TABLE 68 DATA CENTER STORAGE MARKET, BY FORM FACTOR, 2022-2025 (USD MILLION)

- TABLE 69 DATA CENTER STORAGE MARKET, BY FORM FACTOR, 2026-2032 (USD MILLION)

- TABLE 70 3.5 INCH: DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2022-2025 (USD MILLION)

- TABLE 71 3.5 INCH: DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2026-2032 (USD MILLION)

- TABLE 72 2.5 INCH: DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2022-2025 (USD MILLION)

- TABLE 73 2.5 INCH: DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2026-2032 (USD MILLION)

- TABLE 74 M.2: DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2022-2025 (USD MILLION)

- TABLE 75 M.2: DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2026-2032 (USD MILLION)

- TABLE 76 U.2/U.3: DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2022-2025 (USD MILLION)

- TABLE 77 U.2/U.3: DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2026-2032 (USD MILLION)

- TABLE 78 EDSFF: DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2022-2025 (USD MILLION)

- TABLE 79 EDSFF: DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2026-2032 (USD MILLION)

- TABLE 80 ADD-IN CARDS (AICS): DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2022-2025 (USD MILLION)

- TABLE 81 ADD-IN CARDS (AICS): DATA CENTER STORAGE MARKET, BY STORAGE MEDIUM, 2026-2032 (USD MILLION)

- TABLE 82 DATA CENTER STORAGE MARKET, BY DEPLOYMENT TYPE, 2022-2025 (USD MILLION)

- TABLE 83 DATA CENTER STORAGE MARKET, BY DEPLOYMENT TYPE, 2026-2032 (USD MILLION)

- TABLE 84 ON-PREMISES: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 85 ON-PREMISES: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 86 CLOUD-BASED: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 87 CLOUD-BASED: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 88 HYBRID: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 89 HYBRID: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 90 DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 91 DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 92 HYPERSCALE/CLOUD SERVICE PROVIDERS: DATA CENTER STORAGE MARKET, BY DEPLOYMENT TYPE, 2022-2025 (USD MILLION)

- TABLE 93 HYPERSCALE/CLOUD SERVICE PROVIDERS: DATA CENTER STORAGE MARKET, BY DEPLOYMENT TYPE, 2026-2032 (USD MILLION)

- TABLE 94 HYPERSCALE/CLOUD SERVICE PROVIDERS: DATA CENTER STORAGE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 95 HYPERSCALE/CLOUD SERVICE PROVIDERS: DATA CENTER STORAGE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 96 HYPERSCALE/CLOUD SERVICE PROVIDERS: DATA CENTER STORAGE MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 97 HYPERSCALE/CLOUD SERVICE PROVIDERS: DATA CENTER STORAGE MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 98 HYPERSCALE/CLOUD SERVICE PROVIDERS: DATA CENTER STORAGE MARKET IN EUROPE, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 99 HYPERSCALE/CLOUD SERVICE PROVIDERS: DATA CENTER STORAGE MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 100 HYPERSCALE/CLOUD SERVICE PROVIDERS: DATA CENTER STORAGE MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 101 HYPERSCALE/CLOUD SERVICE PROVIDERS: DATA CENTER STORAGE MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 102 HYPERSCALE/CLOUD SERVICE PROVIDERS: DATA CENTER STORAGE MARKET IN ROW, BY REGION, 2022-2025 (USD MILLION)

- TABLE 103 HYPERSCALE/CLOUD SERVICE PROVIDERS: DATA CENTER STORAGE MARKET IN ROW, BY REGION, 2026-2032 (USD MILLION)

- TABLE 104 HYPERSCALE/CLOUD SERVICE PROVIDERS: DATA CENTER STORAGE MARKET IN SOUTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 105 HYPERSCALE/CLOUD SERVICE PROVIDERS: DATA CENTER STORAGE MARKET IN SOUTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 106 HYPERSCALE/CLOUD SERVICE PROVIDERS: DATA CENTER STORAGE MARKET IN MIDDLE EAST & AFRICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 107 HYPERSCALE/CLOUD SERVICE PROVIDERS: DATA CENTER STORAGE MARKET IN MIDDLE EAST & AFRICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 108 ENTERPRISES: DATA CENTER STORAGE MARKET, BY DEPLOYMENT TYPE, 2022-2025 (USD MILLION)

- TABLE 109 ENTERPRISES: DATA CENTER STORAGE MARKET, BY DEPLOYMENT TYPE, 2026-2032 (USD MILLION)

- TABLE 110 ENTERPRISES: DATA CENTER STORAGE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 111 ENTERPRISES: DATA CENTER STORAGE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 112 ENTERPRISES: DATA CENTER STORAGE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 113 ENTERPRISES: DATA CENTER STORAGE MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 114 ENTERPRISES: DATA CENTER STORAGE MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 115 ENTERPRISES: DATA CENTER STORAGE MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 116 ENTERPRISES: DATA CENTER STORAGE MARKET IN EUROPE, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 117 ENTERPRISES: DATA CENTER STORAGE MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 118 ENTERPRISES: DATA CENTER STORAGE MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 119 ENTERPRISES: DATA CENTER STORAGE MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 120 ENTERPRISES: DATA CENTER STORAGE MARKET IN ROW, BY REGION, 2022-2025 (USD MILLION)

- TABLE 121 ENTERPRISES: DATA CENTER STORAGE MARKET IN ROW, BY REGION, 2026-2032 (USD MILLION)

- TABLE 122 ENTERPRISES: DATA CENTER STORAGE MARKET IN SOUTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 123 ENTERPRISES: DATA CENTER STORAGE MARKET IN SOUTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 124 ENTERPRISES: DATA CENTER STORAGE MARKET IN MIDDLE EAST & AFRICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 125 ENTERPRISES: DATA CENTER STORAGE MARKET IN MIDDLE EAST & AFRICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 126 GOVERNMENT & PUBLIC SECTOR: DATA CENTER STORAGE MARKET, BY DEPLOYMENT TYPE, 2022-2025 (USD MILLION)

- TABLE 127 GOVERNMENT & PUBLIC SECTOR: DATA CENTER STORAGE MARKET, BY DEPLOYMENT TYPE, 2026-2032 (USD MILLION)

- TABLE 128 GOVERNMENT & PUBLIC SECTOR: DATA CENTER STORAGE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 129 GOVERNMENT & PUBLIC SECTOR: DATA CENTER STORAGE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 130 GOVERNMENT & PUBLIC SECTOR: DATA CENTER STORAGE MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 131 GOVERNMENT & PUBLIC SECTOR: DATA CENTER STORAGE MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 132 GOVERNMENT & PUBLIC SECTOR: DATA CENTER STORAGE MARKET IN EUROPE, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 133 GOVERNMENT & PUBLIC SECTOR: DATA CENTER STORAGE MARKET IN EUROPE, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 134 GOVERNMENT & PUBLIC SECTOR: DATA CENTER STORAGE MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 135 GOVERNMENT & PUBLIC SECTOR: DATA CENTER STORAGE MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 136 GOVERNMENT & PUBLIC SECTOR: DATA CENTER STORAGE MARKET IN ROW, BY REGION, 2022-2025 (USD MILLION)

- TABLE 137 GOVERNMENT & PUBLIC SECTOR: DATA CENTER STORAGE MARKET IN ROW, BY REGION, 2026-2032 (USD MILLION)

- TABLE 138 GOVERNMENT & PUBLIC SECTOR: DATA CENTER STORAGE MARKET IN SOUTH AMERICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 139 GOVERNMENT & PUBLIC SECTOR: DATA CENTER STORAGE MARKET IN SOUTH AMERICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 140 GOVERNMENT & PUBLIC SECTOR: DATA CENTER STORAGE MARKET IN MIDDLE EAST & AFRICA, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 141 GOVERNMENT & PUBLIC SECTOR: DATA CENTER STORAGE MARKET IN MIDDLE EAST & AFRICA, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 142 DATA CENTER STORAGE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 143 DATA CENTER STORAGE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 144 NORTH AMERICA: DATA CENTER STORAGE MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 145 NORTH AMERICA: DATA CENTER STORAGE MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 146 NORTH AMERICA: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 147 NORTH AMERICA: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 148 US: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 149 US: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 150 CANADA: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 151 CANADA: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 152 MEXICO: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 153 MEXICO: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 154 EUROPE: DATA CENTER STORAGE MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 155 EUROPE: DATA CENTER STORAGE MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 156 EUROPE: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 157 EUROPE: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 158 GERMANY: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 159 GERMANY: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 160 UK: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 161 UK: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 162 FRANCE: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 163 FRANCE: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 164 NETHERLANDS: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 165 NETHERLANDS: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 166 RUSSIA: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 167 RUSSIA: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 168 ITALY: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 169 ITALY: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 170 POLAND: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 171 POLAND: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 172 SPAIN: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 173 SPAIN: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 174 SWITZERLAND: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 175 SWITZERLAND: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 176 SWEDEN: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 177 SWEDEN: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 178 BELGIUM: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 179 BELGIUM: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 180 REST OF EUROPE: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 181 REST OF EUROPE: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 182 ASIA PACIFIC: DATA CENTER STORAGE MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 183 ASIA PACIFIC: DATA CENTER STORAGE MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 184 ASIA PACIFIC: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 185 ASIA PACIFIC: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 186 CHINA: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 187 CHINA: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 188 AUSTRALIA: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 189 AUSTRALIA: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 190 JAPAN: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 191 JAPAN: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 192 INDIA: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 193 INDIA: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 194 SINGAPORE: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 195 SINGAPORE: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 196 INDONESIA: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 197 INDONESIA: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 198 NEW ZEALAND: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 199 NEW ZEALAND: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 200 SOUTH KOREA: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 201 SOUTH KOREA: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 202 REST OF ASIA PACIFIC: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 203 REST OF ASIA PACIFIC: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 204 ROW: DATA CENTER STORAGE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 205 ROW: DATA CENTER STORAGE MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 206 ROW: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 207 ROW: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 208 SOUTH AMERICA: DATA CENTER STORAGE MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 209 SOUTH AMERICA: DATA CENTER STORAGE MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 210 SOUTH AMERICA: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 211 SOUTH AMERICA: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 212 BRAZIL: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 213 BRAZIL: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 214 REST OF SOUTH AMERICA: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 215 REST OF SOUTH AMERICA: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 216 MIDDLE EAST & AFRICA: DATA CENTER STORAGE MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 217 MIDDLE EAST & AFRICA: DATA CENTER STORAGE MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 218 MIDDLE EAST & AFRICA: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 219 MIDDLE EAST & AFRICA: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 220 GCC: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 221 GCC: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 222 SOUTH AFRICA: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 223 SOUTH AFRICA: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 224 REST OF MIDDLE EAST & AFRICA: DATA CENTER STORAGE MARKET, BY END USER, 2022-2025 (USD MILLION)

- TABLE 225 REST OF MIDDLE EAST & AFRICA: DATA CENTER STORAGE MARKET, BY END USER, 2026-2032 (USD MILLION)

- TABLE 226 DATA CENTER STORAGE MARKET: KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- TABLE 227 DATA CENTER STORAGE MARKET: MARKET SHARE ANALYSIS OF TOP 5 PLAYERS, 2025

- TABLE 228 DATA CENTER STORAGE MARKET: REGION FOOTPRINT

- TABLE 229 DATA CENTER STORAGE MARKET: INTERFACE FOOTPRINT

- TABLE 230 DATA CENTER STORAGE MARKET: CAPACITY FOOTPRINT

- TABLE 231 DATA CENTER STORAGE MARKET: DEPLOYMENT TYPE FOOTPRINT

- TABLE 232 DATA CENTER STORAGE MARKET: END USER FOOTPRINT

- TABLE 233 DATA CENTER STORAGE MARKET: PRODUCT LAUNCHES, JANUARY 2022-DECEMBER 2025

- TABLE 234 DATA CENTER STORAGE MARKET: DEALS, JANUARY 2022-DECEMBER 2025

- TABLE 235 SAMSUNG: COMPANY OVERVIEW

- TABLE 236 SAMSUNG: PRODUCTS OFFERED

- TABLE 237 SAMSUNG: PRODUCT LAUNCHES

- TABLE 238 MICRON TECHNOLOGY, INC.: COMPANY OVERVIEW

- TABLE 239 MICRON TECHNOLOGY, INC.: PRODUCTS OFFERED

- TABLE 240 MICRON TECHNOLOGY, INC.: PRODUCT LAUNCHES

- TABLE 241 KIOXIA HOLDINGS CORPORATION: COMPANY OVERVIEW

- TABLE 242 KIOXIA HOLDINGS CORPORATION: PRODUCTS OFFERED

- TABLE 243 KIOXIA HOLDINGS CORPORATION: PRODUCT LAUNCHES

- TABLE 244 SK HYNIX INC.: COMPANY OVERVIEW

- TABLE 245 SK HYNIX INC.: PRODUCTS OFFERED

- TABLE 246 SK HYNIX INC.: PRODUCT LAUNCHES

- TABLE 247 SANDISK CORPORATION: COMPANY OVERVIEW

- TABLE 248 SANDISK CORPORATION: PRODUCTS OFFERED

- TABLE 249 SANDISK CORPORATION: DEALS

- TABLE 250 SEAGATE TECHNOLOGY LLC: COMPANY OVERVIEW

- TABLE 251 SEAGATE TECHNOLOGY LLC: PRODUCTS OFFERED

- TABLE 252 SEGATE TECHNOLOGY LLC: PRODUCT LAUNCHES

- TABLE 253 WESTERN DIGITAL CORPORATION: COMPANY OVERVIEW

- TABLE 254 WESTERN DIGITAL CORPORATION: PRODUCTS OFFERED

- TABLE 255 WESTERN DIGITAL CORPORATION: PRODUCT LAUNCHES

- TABLE 256 WESTERN DIGITAL CORPORATION: DEALS

- TABLE 257 TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION: COMPANY OVERVIEW

- TABLE 258 TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION: PRODUCTS OFFERED

- TABLE 259 TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION: PRODUCT LAUNCHES

- TABLE 260 BEIJING MEMBLAZE TECHNOLOGY CO., LTD.: COMPANY OVERVIEW

- TABLE 261 DAPUSTOR CORPORATION: COMPANY OVERVIEW

- TABLE 262 SCALEFLUX, INC.: COMPANY OVERVIEW

- TABLE 263 SHENZHEN UNIONMEMORY INFORMATION SYSTEM LIMITED: COMPANY OVERVIEW

- TABLE 264 NIMBUS DATA: COMPANY OVERVIEW

- TABLE 265 KINGSTON TECHNOLOGY: COMPANY OVERVIEW

- TABLE 266 PENGUIN SOLUTIONS: COMPANY OVERVIEW

- TABLE 267 ATP ELECTRONICS, INC.: COMPANY OVERVIEW

- TABLE 268 INNODISK CORPORATION: COMPANY OVERVIEW

- TABLE 269 APACER TECHNOLOGY INC.: COMPANY OVERVIEW

- TABLE 270 VIRTIUM: COMPANY OVERVIEW

- TABLE 271 SWISSBIT AG: COMPANY OVERVIEW

- TABLE 272 BIWIN STORAGE TECHNOLOGY CO., LTD.: COMPANY OVERVIEW

- TABLE 273 FADU INC.: COMPANY OVERVIEW

- TABLE 274 YMTC: COMPANY OVERVIEW

- TABLE 275 VIKING ENTERPRISE SOLUTIONS: COMPANY OVERVIEW

- TABLE 276 PHISON ELECTRONICS: COMPANY OVERVIEW

- TABLE 277 MAJOR SECONDARY SOURCES

- TABLE 278 KEY PARTICIPANTS IN PRIMARY INTERVIEWS

- TABLE 279 DATA OBTAINED FROM PRIMARY SOURCES

- TABLE 280 DATA CENTER STORAGE MARKET: RESEARCH ASSUMPTIONS

- TABLE 281 DATA CENTER STORAGE MARKET: RISK ASSESSMENT

List of Figures

- FIGURE 1 MARKETS COVERED AND REGIONAL SCOPE

- FIGURE 2 DURATION COVERED

- FIGURE 3 MARKET SCENARIO

- FIGURE 4 GLOBAL DATA CENTER STORAGE MARKET, 2022-2032

- FIGURE 5 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN DATA CENTER STORAGE MARKET, 2022-2025

- FIGURE 6 DISRUPTIONS INFLUENCING GROWTH OF DATA CENTER STORAGE MARKET

- FIGURE 7 HIGH-GROWTH SEGMENTS IN DATA CENTER STORAGE MARKET, 2026-2032

- FIGURE 8 ASIA PACIFIC TO CAPTURE LARGEST SHARE AND RECORD HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 9 INCLINATION TOWARD AI- AND CLOUD-DRIVEN STORAGE TO CREATE GROWTH OPPORTUNITIES FOR PLAYERS IN DATA CENTER STORAGE MARKET

- FIGURE 10 SOLID-STATE DRIVES SEGMENT TO LEAD DATA CENTER STORAGE MARKET IN 2032

- FIGURE 11 NVME SEGMENT TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 12 ULTRA-HIGH CAPACITY (>20 TB) SEGMENT TO COMMAND MARKET IN 2032

- FIGURE 13 EDSFF SEGMENT TO DOMINATE MARKET IN 2032

- FIGURE 14 CLOUD-BASED SEGMENT TO CAPTURE MAJORITY OF MARKET SHARE THROUGHOUT FORECAST PERIOD

- FIGURE 15 HYPERSCALE/CLOUD SERVICE PROVIDERS TO REMAIN PRIMARY REVENUE CONTRIBUTORS THROUGHOUT FORECAST PERIOD

- FIGURE 16 ASIA PACIFIC TO LEAD DATA CENTER STORAGE MARKET IN 2032

- FIGURE 17 INDIA TO REGISTER HIGHEST CAGR IN GLOBAL MARKET FROM 2026 TO 2032

- FIGURE 18 DATA CENTER STORAGE MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 19 IMPACT ANALYSIS: DRIVERS

- FIGURE 20 IMPACT ANALYSIS: RESTRAINTS

- FIGURE 21 IMPACT ANALYSIS: OPPORTUNITIES

- FIGURE 22 IMPACT ANALYSIS: CHALLENGES

- FIGURE 23 DATA CENTER STORAGE MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 24 DATA CENTER STORAGE VALUE CHAIN ANALYSIS

- FIGURE 25 DATA CENTER STORAGE ECOSYSTEM ANALYSIS

- FIGURE 26 AVERAGE SELLING PRICE TREND OF DATA CENTER STORAGE SOLUTIONS BASED ON DIFFERENT STORAGE MEDIUMS, 2022-2025

- FIGURE 27 AVERAGE SELLING PRICE TREND OF HDDS, BY REGION, 2022-2025

- FIGURE 28 AVERAGE SELLING PRICE TREND OF SSDS, BY REGION, 2022-2025

- FIGURE 29 IMPORT SCENARIO FOR HS CODE 847170-COMPLIANT PRODUCTS IN TOP 5 COUNTRIES, 2021-2025

- FIGURE 30 EXPORT SCENARIO FOR HS CODE 847170-COMPLIANT PRODUCTS IN TOP 5 COUNTRIES, 2021-2025

- FIGURE 31 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 32 INVESTMENT AND FUNDING SCENARIO, 2022-2026

- FIGURE 33 DATA CENTER STORAGE MARKET: PATENT ANALYSIS, 2016-2025

- FIGURE 34 DECISION-MAKING FACTORS IN DATA CENTER STORAGE MARKET

- FIGURE 35 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR END USERS

- FIGURE 36 KEY BUYING CRITERIA FOR END USERS

- FIGURE 37 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- FIGURE 38 SOLID-STATE DRIVES SEGMENT TO CAPTURE MAJORITY OF MARKET SHARE IN 2026

- FIGURE 39 NVME SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 40 ULTRA-HIGH CAPACITY (>20 TB) SEGMENT TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 41 EDSFF SEGMENT TO WITNESS FASTEST GROWTH IN DATA CENTER STORAGE MARKET FROM 2026 TO 2032

- FIGURE 42 CLOUD-BASED SEGMENT TO RECORD HIGHEST CAGR IN DATA CENTER STORAGE MARKET DURING FORECAST PERIOD

- FIGURE 43 HYPERSCALE/CLOUD SERVICE PROVIDERS TO HOLD MAJORITY OF MARKET SHARE IN 2032

- FIGURE 44 ASIA PACIFIC TO REGISTER HIGHEST CAGR IN DATA CENTER STORAGE MARKET BETWEEN 2026 AND 2032

- FIGURE 45 NORTH AMERICA: DATA CENTER STORAGE MARKET SNAPSHOT

- FIGURE 46 EUROPE: DATA CENTER STORAGE MARKET SNAPSHOT

- FIGURE 47 ASIA PACIFIC: DATA CENTER STORAGE MARKET SNAPSHOT

- FIGURE 48 ROW: DATA CENTER STORAGE MARKET SNAPSHOT

- FIGURE 49 REVENUE ANALYSIS OF KEY PLAYERS IN DATA CENTER STORAGE MARKET, 2021-2025

- FIGURE 50 DATA CENTER STORAGE MARKET SHARE ANALYSIS, 2025

- FIGURE 51 COMPANY VALUATION, 2025

- FIGURE 52 FINANCIAL METRICS, 2025

- FIGURE 53 DATA CENTER STORAGE MARKET: COMPANY EVALUATION MATRIX (PUREPLAY SSD VENDORS), 2025

- FIGURE 54 DATA CENTER STORAGE MARKET: COMPANY EVALUATION MATRIX (NAND-INDEPENDENT SSD VENDORS), 2025

- FIGURE 55 DATA CENTER STORAGE MARKET: COMPANY FOOTPRINT

- FIGURE 56 DATA CENTER STORAGE MARKET: BRAND COMPARISON

- FIGURE 57 SAMSUNG: COMPANY SNAPSHOT

- FIGURE 58 MICRON TECHNOLOGY, INC.: COMPANY SNAPSHOT

- FIGURE 59 KIOXIA HOLDINGS CORPORATION: COMPANY SNAPSHOT

- FIGURE 60 SK HYNIX INC.: COMPANY SNAPSHOT

- FIGURE 61 SANDISK CORPORATION: COMPANY SNAPSHOT

- FIGURE 62 SEAGATE TECHNOLOGY LLC: COMPANY SNAPSHOT

- FIGURE 63 WESTERN DIGITAL CORPORATION: COMPANY SNAPSHOT

- FIGURE 64 DATA CENTER STORAGE MARKET: RESEARCH DESIGN

- FIGURE 65 DATA CENTER STORAGE MARKET: RESEARCH APPROACH

- FIGURE 66 DATA OBTAINED FROM SECONDARY SOURCES

- FIGURE 67 PRIMARY BREAKDOWN: BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 68 INSIGHTS GATHERED FROM EXPERTS

- FIGURE 69 DATA CENTER STORAGE MARKET: BOTTOM-UP APPROACH

- FIGURE 70 DATA CENTER STORAGE MARKET: TOP-DOWN APPROACH

- FIGURE 71 DATA CENTER STORAGE MARKET: DATA TRIANGULATION