PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2081124

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 2081124

EV Charging Station Market by DC Fast Charging, Application, Level of Charging, Charging Point, Charging Infrastructure, Operation, Charge Point Operator, Connection Phase, Service, Installation, and Region - Global Forecast to 2033

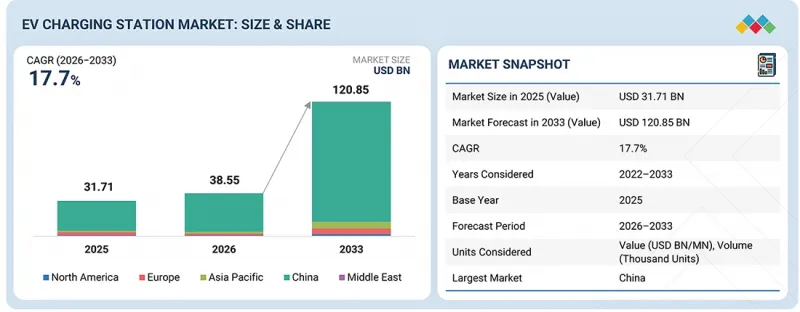

The global EV charging station market is projected to grow from USD 38.55 billion in 2026 to USD 120.85 billion by 2033 at a CAGR of 17.7%. Market expansion is increasingly being shaped by the convergence of vehicle platform evolution, charging ecosystem integration, and utility grid modernization.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | USD Billion |

| Segments | DC Fast Charging, Application, Level of Charging, Charging, Connection Phase, Service, Installation, and Region |

| Regions covered | China, Asia Pacific, Europe, North America, Middle East, and Rest of the World |

OEMs are moving beyond vehicle sales to establish end-to-end charging ecosystems through strategic partnerships with charge point operators, energy providers, and technology companies. In March 2025, BYD introduced its Super e Platform featuring megawatt-class charging capability designed to significantly reduce charging duration for next-generation EVs, while several OEMs accelerated the rollout of 800V and 1,000V architectures to support higher charging throughput. Simultaneously, advancements in power semiconductors, energy management software, and bidirectional charging technologies are improving charger utilization and grid interaction capabilities. Sustaining long-term growth will depend on the industry's ability to scale high-power charging infrastructure, secure grid connectivity, and develop interoperable charging networks that can support the next phase of passenger and commercial vehicle electrification.

"By installation type, fixed charger is expected to be the largest segment of the market during the forecast period."

Fixed charging stations are estimated to account for the largest share of the EV charging station market by installation type, driven by their extensive deployment across public charging hubs, highway corridors, commercial properties, and fleet charging depots. Their dominance is reinforced by government infrastructure programs, utility investments, and long-term commitments from charging network operators to expand permanent charging assets. By the end of 2025, public charging infrastructure had reached a scale where charging availability increasingly shifted from a deployment challenge to a network optimization challenge, with operators focusing on charger reliability, utilization, and power delivery capacity. Most newly commissioned charging sites continue to be fixed installations integrated into urban mobility networks, destination charging locations, and strategic transport corridors. Additionally, the growing deployment of high-power DC fast chargers exceeding 150 kW is primarily concentrated within fixed charging infrastructure, strengthening its role as the backbone of public charging ecosystems and supporting its market leadership.

"The DC charging station segment is expected to capture the largest share of the EV charging station market during the forecast period."

The global DC fast chargers market, accounting for approximately 46% of total market share in 2026, is supported by strong government policies, extensive infrastructure investments, and the presence of major EV markets such as China and South Korea. Public charging stations are leading the global DC fast chargers market in 2026, accounting for approximately 60% of total market share, driven by the rapid expansion of highway fast-charging corridors and urban charging hubs, supported by initiatives such as BYD's 1,000 kW supercharging plans, Huawei's ongoing rollout of 100,000 ultrafast stations, and the Mercedes-Benz-BMW joint venture working toward 7,000 stations by year-end 2026. As 1,000-volt vehicle architectures become mainstream and consumer demand for sub-10-minute charging accelerates, DC infrastructure is structurally positioned to capture the largest share of incremental station deployments globally through 2033.

"Asia Pacific (excluding China) is expected to account for a significant market share during the forecast period."

India is predicted to account for the largest share of the Asia Pacific EV charging station market, excluding China, during the forecast period. The country's leadership is increasingly driven by a coordinated approach that combines vehicle electrification targets, charging infrastructure deployment, and domestic manufacturing initiatives. In September 2024, the Government of India launched the PM E DRIVE scheme, allocating substantial funding to accelerate the rollout of public charging infrastructure and strengthen the national EV ecosystem. In 2025, India accelerated charging infrastructure deployment across metropolitan areas, intercity corridors, and fleet charging locations, strengthening the foundation for long-term EV adoption and network utilization. Public and private sector investments by charging operators, oil marketing companies, utilities, and OEMs continue to expand charging coverage across urban centers, highways, and logistics corridors. In August 2025, NITI Aayog introduced the India Electric Mobility Index, providing a state-level framework to benchmark EV readiness and infrastructure development. These initiatives position India as the primary growth engine for EV charging infrastructure expansion across Asia Pacific through 2033, supported by strong policy alignment, accelerating vehicle adoption, and sustained infrastructure investment.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: OEMs - 24%, Tier I - 67%, and Others - 9%

- By Designation: CXOs - 33%, Managers - 52%, and Executives - 15%

- By Region: North America - 40%, Europe - 20%, Asia Pacific (Excluding China) - 28%, China - 6%, Middle East - 3%, and Rest of the World - 3%

The EV charging station market is dominated by major players, including ABB (Switzerland), BYD (China), ChargePoint (US), Tesla (US), and Siemens (Germany). These companies have strong product portfolios as well as strong distribution networks at the global level.

Research Coverage:

This research report categorizes EV charging station market by level of charging (Level 1, Level 2, and Level 3), application (private, semi-public, and public), based on charging point type (AC charging, DC charging), charging infrastructure type (CCS, CHAdeMO, Type 1, Tesla SC (NACS), GB/T Fast, and Type 2), electric bus charging type (off-board top-down pantographs, on-board bottom-up pantographs, and charging via connectors), charging service type (EV charging services and battery swapping services), charge point operator (Asia Pacific, Europe, and North America), DC fast charging type [Slow DC (<49 kW), Fast DC (50-149 kW) and DC Ultra-Fast 1 (150-349 KW), and DC Ultra-Fast 2 (>349 kW)], installation type (portable chargers and fixed chargers), operation (mode 1, mode 2, mode 3, and mode 4), connection phase (single phase and three phase), and Region/Geography (China, Asia Pacific, Europe, North America, the Middle East, and the Rest of the World). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities influencing the growth of the EV charging station market. A detailed analysis of the key industry players was done to provide insights into their business overview, solutions, and services; key strategies; Contracts, partnerships, agreements, product & service launches, mergers & acquisitions, and other developments. This report covers the competitive analysis of upcoming startups in the EV charging station market ecosystem.

Key Benefits of Buying the Report:

- The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall EV charging station market and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

- The report will also help stakeholders understand the market pulse and provide information on key market drivers, restraints, challenges, and opportunities.

- The report will help stakeholders understand the current and future pricing trends of different EV charging systems based on their capacity.

The report provides insights into the following pointers:

Analysis of key drivers (surge in electric vehicle adoption, financial incentives offered by governments to promote charging networks, advancements in battery chemistry improving driving range, and fleet electrification accelerates EV charging market growth), restraints (fragmented charging standards limiting EV adoption, high capital investment required for ultrafast charging infrastructure, underdeveloped power infrastructure for EV charging, and retrofitting challenges in multistorey residential buildings), opportunities (advancements in V2G technology and bidirectional charging, adoption of IoT-enabled smart charging networks, expansion of green and sustainable EV charging solutions, battery-swapping emerging as a viable charging alternative, integration of EV charging in smart city initiatives, market shift towards smart chargers, and expansion of Charging-as-a-Service business model), and challenges (cost gap between ICE vehicles and EVs, regulatory hurdles in EV charger installation, high reliance on non-renewable energy sources for charging, scarcity of lithium resources challenging EV sector growth, and low utilization rates and profitability challenges for CPOs)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the EV charging station market

- Market Development: Comprehensive information about lucrative markets (the report analyzes the EV charging station market across varied regions)

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the EV charging station market

- Competitive Assessment: In-depth assessment of market ranking, growth strategies, and service offerings of leading players like ABB (Switzerland), EVBox (Netherlands), BYD (China), ChargePoint (US), Tesla (US), and Charge Point Operators, including BP (UK), Shell (UK), ENGIE (France), Total Energies (France), and Enel X (Italy), among others in EV charging station market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN EV CHARGING STATION MARKET

- 3.2 EV CHARGING STATION MARKET, BY LEVEL OF CHARGING

- 3.3 EV CHARGING STATION MARKET, BY CHARGING POINT TYPE

- 3.4 EV CHARGING STATION MARKET, BY CHARGING INFRASTRUCTURE TYPE

- 3.5 EV CHARGING STATION MARKET, BY APPLICATION

- 3.6 EV CHARGING STATION MARKET, BY DC FAST CHARGING TYPE

- 3.7 EV CHARGING STATION MARKET, BY INSTALLATION TYPE

- 3.8 EV CHARGING STATION MARKET, BY OPERATION

- 3.9 EV CHARGING STATION MARKET, BY CONNECTION PHASE

- 3.10 EV CHARGING STATION MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Financial incentives by government to promote charging networks

- 4.2.1.2 Ongoing fleet electrification

- 4.2.1.3 Strategic partnerships between OEMs to secure charging access

- 4.2.2 RESTRAINTS

- 4.2.2.1 Fragmented charging standards globally

- 4.2.2.2 High capital investment for ultrafast charging infrastructure

- 4.2.2.3 Retrofitting constraints in multistory residential buildings

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Advancements in V2G technology and bidirectional charging

- 4.2.3.2 Rapid adoption of IoT-enabled smart charging networks

- 4.2.3.3 Rise of green EV charging solutions

- 4.2.3.4 Emerging trend of battery swapping

- 4.2.3.5 Expansion of charging-as-a-service business model

- 4.2.3.6 Zero infrastructure revenue stream for CPOs

- 4.2.4 CHALLENGES

- 4.2.4.1 Regulatory hurdles in EV charger installation

- 4.2.4.2 Over-reliance on non-renewable energy sources

- 4.2.4.3 Low utilization rates and profitability challenges for CPOs

- 4.2.4.4 High power requirement for ultrafast chargers

- 4.2.1 DRIVERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 GDP TRENDS AND FORECAST

- 5.1.2 TRENDS IN GLOBAL EV CHARGING MARKET

- 5.1.3 TRENDS IN GLOBAL ELECTRIC VEHICLE INDUSTRY

- 5.2 ECOSYSTEM ANALYSIS

- 5.2.1 OEMS

- 5.2.2 CHARGING POINT MANUFACTURERS

- 5.2.3 CHARGING POINT OPERATORS

- 5.2.4 PAYMENT PROCESSING COMPANIES

- 5.2.5 NAVIGATION AND MAPPING PROVIDERS

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 BILL OF MATERIALS

- 5.4.1 AC (LEVEL 2) CHARGING POINTS, 2026 VS. 2033

- 5.4.2 DC SLOW CHARGING POINTS, 2026 VS. 2033

- 5.4.3 DC FAST CHARGING POINTS, 2026 VS. 2033

- 5.4.4 DC ULTRAFAST 1 CHARGING POINTS, 2026 VS. 2033

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF CHARGING POINTS OFFERED BY KEY PLAYERS, 2025

- 5.5.2 AVERAGE SELLING PRICE TREND, BY DC CHARGING POINT TYPE, 2023-2025

- 5.5.3 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 8504)

- 5.6.2 EXPORT SCENARIO (HS CODE 8504)

- 5.7 CASE STUDY ANALYSIS

- 5.7.1 CHARGING STATION SIZE OPTIMIZATION BY SHELL

- 5.7.2 LOAD-BALANCING SYSTEM BY POD POINT

- 5.7.3 EV CHARGING NETWORK BY CHARGEPOINT

- 5.7.4 FAST-CHARGING NETWORK BY EVGO

- 5.7.5 EV CHARGING NETWORK IN CITY OF BOULDER

- 5.7.6 CHARGING NETWORK BY ELECTRIFY AMERICA

- 5.7.7 EV CHARGING NETWORK IN CHINA BY MERCEDES-BENZ AND BMW

- 5.7.8 DC FAST CHARGING IN UK BY CHARGEPOINT AND RAW CHARGING

- 5.7.9 SCALABLE FLEET CHARGING INFRASTRUCTURE IN CALIFORNIA BY ABB AND PG&E

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 PERFORMANCE INDICATORS FOR EV CHARGING

- 5.11 FUTURE OF CHARGING

- 5.11.1 FAST-CHARGING HUBS

- 5.11.2 CURBSIDE CHARGING

- 5.11.3 SOFTWARE DEFINED CHARGING NETWORKS

- 5.11.4 AI AND SMART ENERGY MANAGEMENT

- 5.11.5 INDUCTION CHARGING

- 5.12 POWER BOOSTER IN CHARGING SYSTEMS

- 5.13 KEY CONFERENCES AND EVENTS, 2026-2027

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 WIRELESS CHARGING

- 6.1.2 BIDIRECTIONAL CHARGING

- 6.1.3 MEGAWATT CHARGING

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 OVERHEAD CHARGING

- 6.2.2 PLUG-AND-PAY CHARGING

- 6.2.3 ROBOTIC AND MOBILE CHARGING

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 TURBOCHARGING

- 6.3.2 SMART CHARGING

- 6.3.3 IOT INTEGRATION

- 6.4 IMPACT OF AI/GEN AI

- 6.5 PATENT ANALYSIS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2 REGULATORY FRAMEWORK

- 7.2.1 NETHERLANDS

- 7.2.2 GERMANY

- 7.2.3 FRANCE

- 7.2.4 UK

- 7.2.5 CHINA

- 7.2.6 US

- 7.2.7 CANADA

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.1.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.1.2 BUYING CRITERIA

9 OEM ANALYSIS AND FUTURE ROADMAP

- 9.1 OEM EV CHARGING STATION STRATEGY AND ROADMAP ANALYSIS

- 9.1.1 OEM CHARGING INFRASTRUCTURE ROADMAP

- 9.1.1.1 Tesla

- 9.1.1.2 Volkswagen

- 9.1.1.3 Ford Motor Company

- 9.1.1.4 General Motors

- 9.1.1.5 Hyundai Motor Group

- 9.1.1.6 BMW/Mercedes-Benz

- 9.1.1.7 Rivian

- 9.1.1.8 Lucid Motors

- 9.1.2 OEM PARTNERSHIPS WITH CHARGING OPERATORS

- 9.1.3 PROPRIETARY CHARGING NETWORK STRATEGIES

- 9.1.4 NACS ADOPTION IMPACT ON OEM ECOSYSTEM

- 9.1.5 KEY OEM EV CHARGING ROADMAP

- 9.1.1 OEM CHARGING INFRASTRUCTURE ROADMAP

- 9.2 BUSINESS MODELS

- 9.2.1 EV CHARGING BUSINESS MODEL FRAMEWORK

- 9.2.2 CHARGE POINT OPERATOR (CPO) MODEL

- 9.2.2.1 Cost structure and economics

- 9.2.2.1.1 CAPEX breakdown

- 9.2.2.1.2 OPEX breakdown

- 9.2.2.1.3 Revenue per charger

- 9.2.2.1.4 Utilization economic

- 9.2.2.1.5 Payback assumptions for CPOs

- 9.2.2.1 Cost structure and economics

- 9.2.3 CHARGING AS A SERVICE (CAAS) MODEL

- 9.2.4 OEM INTEGRATED CHARGING ECOSYSTEM MODEL

- 9.2.5 FLEET CHARGING BUSINESS MODEL

- 9.2.6 SUBSCRIPTION AND SERVICE REVENUE MODEL

- 9.2.7 SOFTWARE AND BACKEND REVENUE MODEL

- 9.2.8 MAINTENANCE AND UPTIME CONTRACTS

- 9.3 FUTURE REVENUE POOLS AND EMERGING OPPORTUNITIES

- 9.3.1 MEGAWATT CHARGING FOR COMMERCIAL VEHICLES

- 9.3.2 FLEET CHARGING INFRASTRUCTURE

- 9.3.3 RENEWABLE INTEGRATED CHARGING STATIONS

- 9.3.4 BATTERY SWAPPING AND HYBRID INFRASTRUCTURE MODELS

- 9.3.5 AUTONOMOUS EV CHARGING SYSTEMS

10 EV CHARGING STATION MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 CHARGING STATION OFFERINGS, BY APPLICATION

- 10.3 PRIVATE

- 10.3.1 GOVERNMENT SUPPORT FOR INSTALLATIONS AND EMERGENCE OF BIDIRECTIONAL CHARGING TO DRIVE MARKET

- 10.4 SEMI-PUBLIC

- 10.4.1 ONGOING EFFORTS TO SET UP SEMI-PUBLIC CHARGING STATIONS TO DRIVE MARKET

- 10.5 PUBLIC

- 10.5.1 SURGE IN DEMAND FOR DESTINATION AND HIGHWAY CHARGING TO DRIVE MARKET

- 10.6 PRIMARY INSIGHTS

11 EV CHARGING STATION MARKET, BY CHARGE POINT OPERATOR

- 11.1 INTRODUCTION

- 11.2 ASIA PACIFIC: CHARGE POINT OPERATORS

- 11.2.1 CHINA

- 11.2.2 INDIA

- 11.2.3 JAPAN

- 11.2.4 SOUTH KOREA

- 11.3 EUROPE: CHARGE POINT OPERATORS

- 11.3.1 GERMANY

- 11.3.2 FRANCE

- 11.3.3 UK

- 11.3.4 DENMARK

- 11.3.5 NETHERLANDS

- 11.3.6 NORWAY

- 11.3.7 WITZERLAND

- 11.3.8 SPAIN

- 11.4 NORTH AMERICA: CHARGE POINT OPERATORS

- 11.4.1 US

- 11.4.2 CANADA

12 EV CHARGING STATION MARKET, BY CHARGING INFRASTRUCTURE TYPE

- 12.1 INTRODUCTION

- 12.2 PRIMARY CHARGING INFRASTRUCTURE, BY COUNTRY/REGION

- 12.3 TYPE 1

- 12.3.1 HIGH DEMAND FOR AC CHARGING IN NORTH AMERICA TO DRIVE MARKET

- 12.4 TYPE 2

- 12.4.1 RAPID ADOPTION OF AC CHARGING IN EUROPE AND ASIA PACIFIC TO DRIVE MARKET

- 12.5 CHADEMO

- 12.5.1 STRONG V2G CAPABILITIES AND CONTINUED BACKING FROM JAPANESE OEMS TO DRIVE MARKET

- 12.6 CCS

- 12.6.1 UNIFIED INTERFACE WITH ABILITY TO CHARGE VIA BOTH AC AND DC POWER TO DRIVE MARKET

- 12.7 NACS/TESLA SUPERCHARGER

- 12.7.1 EXPANDING TESLA SUPERCHARGER NETWORK TO DRIVE MARKET

- 12.8 GB/T FAST

- 12.8.1 INCREASING DC CHARGING SETUPS IN CHINA TO DRIVE MARKET

- 12.9 PRIMARY INSIGHTS

13 EV CHARGING STATION MARKET, BY CHARGING POINT TYPE

- 13.1 INTRODUCTION

- 13.2 CHARGING POINT COMPARISON, BY KEY PLAYER

- 13.3 AC CHARGING

- 13.3.1 RESIDENTIAL AND WORKPLACE INSTALLATIONS TO DRIVE MARKET

- 13.4 DC CHARGING

- 13.4.1 HIGHWAY AND FLEET ELECTRIFICATION TO DRIVE MARKET

- 13.5 PRIMARY INSIGHTS

14 EV CHARGING STATION MARKET, BY CHARGING SERVICE TYPE

- 14.1 INTRODUCTION

- 14.2 EV CHARGING SERVICES

- 14.3 BATTERY SWAPPING SERVICES

15 EV CHARGING STATION MARKET, BY CONNECTION PHASE

- 15.1 INTRODUCTION

- 15.2 EV CHARGING STATIONS, BY CONNECTION PHASE

- 15.3 SINGLE PHASE

- 15.3.1 STEADY GROWTH IN RESIDENTIAL APPLICATIONS TO DRIVE MARKET

- 15.4 THREE PHASE

- 15.4.1 EXPANSION OF PUBLIC AND COMMERCIAL CHARGING HUBS TO DRIVE MARKET

- 15.5 PRIMARY INSIGHTS

16 EV CHARGING STATION MARKET, BY DC FAST CHARGING TYPE

- 16.1 INTRODUCTION

- 16.2 DC FAST CHARGING OFFERINGS, BY KEY PLAYER

- 16.3 SLOW DC

- 16.3.1 FLEXIBLE DEPLOYMENT THROUGH SEMI-PUBLIC CHARGING POINTS TO DRIVE MARKET

- 16.4 FAST DC

- 16.4.1 INCREASING DEMAND FOR QUICK TURNAROUND CHARGING TO DRIVE MARKET

- 16.5 DC ULTRAFAST 1

- 16.5.1 EXPANDING HIGH-CAPACITY CHARGING INFRASTRUCTURE TO DRIVE MARKET

- 16.6 DC ULTRAFAST 2

- 16.6.1 RISING ELECTRIFICATION OF COMMERCIAL VEHICLE FLEETS TO DRIVE MARKET

- 16.7 400 KW

- 16.8 MEGAWATT CHARGING SYSTEMS

- 16.9 PRIMARY INSIGHTS

17 EV CHARGING STATION MARKET, BY ELECTRIC BUS CHARGING TYPE

- 17.1 INTRODUCTION

- 17.2 OFF-BOARD TOP-DOWN PANTOGRAPHS

- 17.3 ON-BOARD BOTTOM-UP PANTOGRAPHS

- 17.4 CHARGING VIA CONNECTORS

18 EV CHARGING STATION MARKET, BY INSTALLATION TYPE

- 18.1 INTRODUCTION

- 18.2 PORTABLE CHARGERS, BY KEY PLAYER

- 18.3 PORTABLE CHARGERS

- 18.3.1 FLEXIBLE OFF-GRID SOLUTIONS TO DRIVE MARKET

- 18.4 FIXED CHARGERS

- 18.4.1 STRATEGIC ALLIANCES, PUBLIC-PRIVATE INVESTMENTS, AND GOVERNMENT SUBSIDIES TO DRIVE MARKET

- 18.5 PRIMARY INSIGHTS

19 EV CHARGING STATION MARKET, BY LEVEL OF CHARGING

- 19.1 INTRODUCTION

- 19.2 EV CHARGER OFFERINGS, BY LEVEL OF CHARGING

- 19.3 LEVEL 1

- 19.3.1 COST-EFFECTIVE RESIDENTIAL SOLUTIONS TO DRIVE MARKET

- 19.4 LEVEL 2

- 19.4.1 EXPANDING COMMERCIAL AND PUBLIC NETWORKS TO DRIVE MARKET

- 19.5 LEVEL 3

- 19.5.1 DEMAND FOR DESTINATION CHARGES AND GROWING FLEET ELECTRIFICATION TO DRIVE MARKET

- 19.6 PRIMARY INSIGHTS

20 EV CHARGING STATION MARKET, BY OPERATION

- 20.1 INTRODUCTION

- 20.2 EV CHARGING STATIONS, BY OPERATION

- 20.3 MODE 1

- 20.3.1 GROWTH IN EMERGING ECONOMIES TO DRIVE MARKET

- 20.4 MODE 2

- 20.4.1 EXPANSION OF PUBLIC CHARGING NETWORKS TO DRIVE MARKET

- 20.5 MODE 3

- 20.5.1 FOCUS ON SAFETY AND USER EXPERIENCE TO DRIVE MARKET

- 20.6 MODE 4

- 20.6.1 NEED FOR LONG-RANGE EV CAPABILITIES TO DRIVE MARKET

- 20.7 PRIMARY INSIGHTS

21 EV CHARGING STATION MARKET, BY REGION

- 21.1 INTRODUCTION

- 21.2 ASIA PACIFIC

- 21.2.1 INDIA

- 21.2.1.1 FAME-II scheme and state EV policies to drive market

- 21.2.2 JAPAN

- 21.2.2.1 Energy security and 2050 carbon neutrality goals to drive market

- 21.2.3 SOUTH KOREA

- 21.2.3.1 Rapid EV infrastructure supported by government policies to drive market

- 21.2.4 SINGAPORE

- 21.2.4.1 Increasing investment in EV adoption to meet 2040 ICE phase-out target to drive market

- 21.2.5 THAILAND

- 21.2.5.1 Accelerating EV charging network growth to drive market

- 21.2.6 TAIWAN

- 21.2.6.1 EV charging infrastructure supported by government incentives to drive market

- 21.2.7 INDONESIA

- 21.2.7.1 Strategic public-private partnerships for EV Infrastructure to drive market

- 21.2.1 INDIA

- 21.3 CHINA

- 21.4 EUROPE

- 21.4.1 FRANCE

- 21.4.1.1 Deployment of fast & ultrafast charging stations to drive market

- 21.4.2 GERMANY

- 21.4.2.1 Private investment with Green Financing to drive market

- 21.4.3 NETHERLANDS

- 21.4.3.1 Investment in ultrafast charging hubs to drive market

- 21.4.4 NORWAY

- 21.4.4.1 Innovation in EV charging infrastructure to drive market

- 21.4.5 SWEDEN

- 21.4.5.1 Freight electrification goals to drive market

- 21.4.6 UK

- 21.4.6.1 Government initiatives backed by rising investments in ultra-low emission vehicles to drive market

- 21.4.7 DENMARK

- 21.4.7.1 Government support for EV infrastructure adoption to drive market

- 21.4.8 AUSTRIA

- 21.4.8.1 Rapid EV adoption and growth of EV charging infrastructure to drive market

- 21.4.9 SPAIN

- 21.4.9.1 Installation of EV charging infrastructure to drive market

- 21.4.10 SWITZERLAND

- 21.4.10.1 Partnerships between OEMs and electric energy distributors for EV charging station deployment to drive market

- 21.4.1 FRANCE

- 21.5 NORTH AMERICA

- 21.5.1 CANADA

- 21.5.1.1 Partnerships between CPOs and financial bodies to drive market

- 21.5.2 US

- 21.5.2.1 Large-scale deployment of public EV charging infrastructure to drive market

- 21.5.1 CANADA

- 21.6 MIDDLE EAST

- 21.6.1 ISRAEL

- 21.6.1.1 Integration of wireless charging technology in public infrastructure to drive market

- 21.6.2 UAE

- 21.6.2.1 Government initiatives and technological advancements in EV charging infrastructure to drive market

- 21.6.3 SAUDI ARABIA

- 21.6.3.1 Partnerships and large-scale investments in EV charging stations to drive market

- 21.6.1 ISRAEL

- 21.7 REST OF THE WORLD

- 21.7.1 BRAZIL

- 21.7.1.1 Public-private investments between utility providers and CPOs to drive market

- 21.7.2 MEXICO

- 21.7.2.1 Increased adoption of zero-emission cars to drive market

- 21.7.3 SOUTH AFRICA

- 21.7.3.1 Government funding for EV charging infrastructure to drive market

- 21.7.4 OTHERS

- 21.7.1 BRAZIL

22 COMPETITIVE LANDSCAPE

- 22.1 INTRODUCTION

- 22.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- 22.3 MARKET SHARE ANALYSIS, 2025

- 22.3.1 CHARGE POINT MANUFACTURERS

- 22.3.2 CHARGE POINT OPERATORS

- 22.4 REVENUE ANALYSIS, 2021-2025

- 22.5 COMPANY VALUATION AND FINANCIAL METRICS

- 22.6 BRAND/PRODUCT COMPARISON

- 22.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 22.7.1 STARS

- 22.7.2 EMERGING LEADERS

- 22.7.3 PERVASIVE PLAYERS

- 22.7.4 PARTICIPANTS

- 22.7.5 COMPANY FOOTPRINT

- 22.7.5.1 Company footprint

- 22.7.5.2 Country/Region footprint

- 22.7.5.3 Charging point footprint

- 22.7.5.4 Level of charging footprint

- 22.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 22.8.1 PROGRESSIVE COMPANIES

- 22.8.2 RESPONSIVE COMPANIES

- 22.8.3 DYNAMIC COMPANIES

- 22.8.4 STARTING BLOCKS

- 22.8.5 COMPETITIVE BENCHMARKING

- 22.8.5.1 List of startups/SMEs

- 22.8.5.2 Competitive benchmarking of startups/SMEs

- 22.9 COMPETITIVE SCENARIO

- 22.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 22.9.2 DEALS

- 22.9.3 EXPANSIONS

- 22.9.4 OTHER DEVELOPMENTS

23 COMPANY PROFILES

- 23.1 CHARGE POINT MANUFACTURERS

- 23.1.1 ABB

- 23.1.1.1 Business overview

- 23.1.1.2 Products/Solutions/Services offered

- 23.1.1.3 Recent developments

- 23.1.1.3.1 Product launches/developments

- 23.1.1.3.2 Deals

- 23.1.1.3.3 Expansions

- 23.1.1.3.4 Other developments

- 23.1.1.4 MnM view

- 23.1.2 BYD COMPANY LTD.

- 23.1.2.1 Business overview

- 23.1.2.2 Products/Solutions/Services offered

- 23.1.2.3 Recent developments

- 23.1.2.3.1 Product launches/developments

- 23.1.2.3.2 Deals

- 23.1.2.3.3 Expansions

- 23.1.2.3.4 Other Developments

- 23.1.2.4 MnM view

- 23.1.3 CHARGEPOINT, INC.

- 23.1.3.1 Business overview

- 23.1.3.2 Products/Solutions/Services offered

- 23.1.3.3 Recent developments

- 23.1.3.3.1 Product launches/developments

- 23.1.3.3.2 Deals

- 23.1.3.3.3 Other developments

- 23.1.3.4 MnM view

- 23.1.4 TESLA

- 23.1.4.1 Business overview

- 23.1.4.2 Products/Solutions/Services offered

- 23.1.4.3 Recent developments

- 23.1.4.3.1 Product Launches/Developments

- 23.1.4.3.2 Deals

- 23.1.4.3.3 Other developments

- 23.1.4.4 MnM view

- 23.1.5 SIEMENS

- 23.1.5.1 Business overview

- 23.1.5.2 Products/Solutions/Services offered

- 23.1.5.3 Recent developments

- 23.1.5.3.1 Product launches/developments

- 23.1.5.3.2 Deals

- 23.1.5.3.3 Other developments

- 23.1.5.4 MnM view

- 23.1.6 EVBOX

- 23.1.6.1 Business overview

- 23.1.6.2 Products/Solutions/Services offered

- 23.1.6.3 Recent developments

- 23.1.6.3.1 Product launches/developments

- 23.1.6.3.2 Deals

- 23.1.6.3.3 Other Developments

- 23.1.7 DELTA ELECTRONICS, INC.

- 23.1.7.1 Business overview

- 23.1.7.2 Products/Solutions/Services offered

- 23.1.7.3 Recent developments

- 23.1.7.3.1 Product launches/developments

- 23.1.7.3.2 Deals

- 23.1.8 STARCHARGE

- 23.1.8.1 Business overview

- 23.1.8.2 Products/Solutions/Services offered

- 23.1.8.3 Recent developments

- 23.1.8.3.1 Product launches/developments

- 23.1.8.3.2 Deals

- 23.1.8.3.3 Expansions

- 23.1.8.3.4 Other developments

- 23.1.9 SCHNEIDER ELECTRIC

- 23.1.9.1 Business overview

- 23.1.9.2 Products/Solutions/Services offered

- 23.1.9.3 Recent developments

- 23.1.9.3.1 Product launches/developments

- 23.1.9.3.2 Deals

- 23.1.9.3.3 Expansions

- 23.1.10 KEMPOWER OYJ

- 23.1.10.1 Business overview

- 23.1.10.2 Products/Solutions/Services offered

- 23.1.10.3 Recent developments

- 23.1.10.3.1 Product launches/developments

- 23.1.10.3.2 Deals

- 23.1.10.3.3 Expansions

- 23.1.10.3.4 Other developments

- 23.1.11 EFACEC

- 23.1.11.1 Business overview

- 23.1.11.2 Products/Solutions/Services offered

- 23.1.11.3 Recent developments

- 23.1.11.3.1 Product launches/developments

- 23.1.11.3.2 Deals

- 23.1.11.3.3 Expansions

- 23.1.11.3.4 Other Developments

- 23.1.1 ABB

- 23.2 CHARGING POINT OPERATORS

- 23.2.1 SHELL PLC

- 23.2.1.1 Business overview

- 23.2.1.2 Products/Solutions/Services offered

- 23.2.1.3 Recent developments

- 23.2.1.3.1 Deals

- 23.2.1.3.2 Expansions

- 23.2.1.3.3 Other developments

- 23.2.1.4 MnM view

- 23.2.2 TOTALENERGIES

- 23.2.2.1 Business overview

- 23.2.2.2 Products/Solutions/Services offered

- 23.2.2.3 Recent developments

- 23.2.2.3.1 Product launches/developments

- 23.2.2.3.2 Deals

- 23.2.2.3.3 Other developments

- 23.2.2.4 MnM view

- 23.2.3 BP P.L.C.

- 23.2.3.1 Business overview

- 23.2.3.2 Products/Solutions/Services offered

- 23.2.3.3 Recent developments

- 23.2.3.3.1 Deals

- 23.2.3.3.2 Expansions

- 23.2.3.3.3 Other developments

- 23.2.3.4 MnM view

- 23.2.4 ENEL X S.R.L.

- 23.2.4.1 Business overview

- 23.2.4.2 Products/Solutions/Services offered

- 23.2.4.3 Recent developments

- 23.2.4.3.1 Deals

- 23.2.4.3.2 Expansions

- 23.2.4.3.3 Other developments

- 23.2.4.4 MnM view

- 23.2.5 VIRTA GLOBAL

- 23.2.5.1 Business overview

- 23.2.5.2 Products/Solutions/Services offered

- 23.2.5.3 Recent developments

- 23.2.5.3.1 Deals

- 23.2.5.3.2 Other developments

- 23.2.6 ALLEGO B.V.

- 23.2.6.1 Business overview

- 23.2.6.2 Products/Solutions/Services offered

- 23.2.6.3 Recent developments

- 23.2.6.3.1 Deals

- 23.2.6.3.2 Expansions

- 23.2.6.3.3 Other developments

- 23.2.7 TGOOD ELECTRIC CO., LTD.

- 23.2.7.1 Business overview

- 23.2.7.2 Products/Solutions/Services offered

- 23.2.7.3 Recent developments

- 23.2.7.3.1 Deals

- 23.2.7.3.2 Other Developments

- 23.2.8 STATE GRID CORPORATION CHINA

- 23.2.8.1 Business overview

- 23.2.8.2 Recent developments

- 23.2.8.2.1 Deals

- 23.2.8.2.2 Expansions

- 23.2.9 VATTENFALL AB

- 23.2.9.1 Business overview

- 23.2.9.2 Products/Solutions/Services offered

- 23.2.9.3 Recent developments

- 23.2.9.3.1 Deals

- 23.2.9.3.2 Expansions

- 23.2.9.3.3 Other developments

- 23.2.1 SHELL PLC

- 23.3 OTHER PLAYERS

- 23.3.1 BLINK CHARGING CO.

- 23.3.2 ENPHASE ENERGY

- 23.3.3 ELECTRIFY AMERICA

- 23.3.4 OPCONNECT

- 23.3.5 EV SAFE CHARGE INC.

- 23.3.6 IONITY

- 23.3.7 WALLBOX

- 23.3.8 SPARK HORIZON

- 23.3.9 DBT

- 23.3.10 CHARGE+

- 23.3.11 ALFEN NV

- 23.3.12 IES SYNERGY

- 23.3.13 MADIC GROUP

- 23.3.14 BEEV

- 23.3.15 INSTAVOLT

- 23.3.16 FRESHMILE

- 23.3.17 POD POINT

- 23.3.18 BE CHARGE

- 23.3.19 MER

- 23.3.20 ENBW

- 23.3.21 RWE

- 23.3.22 POWERDOT

- 23.3.23 SPARKCHARGE

- 23.3.24 JOLT

- 23.3.25 INSTALLER

- 23.3.26 NUMBAT

- 23.3.27 ITSELECTRIC INC

24 RESEARCH METHODOLOGY

- 24.1 RESEARCH DATA

- 24.1.1 SECONDARY DATA

- 24.1.1.1 Secondary sources

- 24.1.1.2 Key data from secondary sources

- 24.1.2 PRIMARY DATA

- 24.1.2.1 Primary participants

- 24.1.2.2 Breakdown of primary interviews

- 24.1.2.3 Primary interviewees from demand and supply sides

- 24.1.1 SECONDARY DATA

- 24.2 MARKET SIZE ESTIMATION

- 24.2.1 BOTTOM-UP APPROACH

- 24.2.2 TOP-DOWN APPROACH

- 24.3 DATA TRIANGULATION

- 24.4 FACTOR ANALYSIS

- 24.5 RESEARCH ASSUMPTIONS

- 24.6 RESEARCH LIMITATIONS

- 24.7 RISK ASSESSMENT

25 APPENDIX

- 25.1 DISCUSSION GUIDE

- 25.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 25.3 CUSTOMIZATION OPTIONS

- 25.3.1 BREAKDOWN OF EV CHARGING STATION MARKET, BY CHARGING LEVEL, AT COUNTRY LEVEL (FOR COUNTRIES COVERED IN REPORT)

- 25.3.2 BREAKDOWN OF EV CHARGING STATION MARKET, BY DC CHARGING TYPE, AT COUNTRY LEVEL (FOR COUNTRIES COVERED IN REPORT)

- 25.3.3 COMPANY INFORMATION

- 25.3.3.1 Profiles of additional market players (up to five)

- 25.4 RELATED REPORTS

- 25.5 AUTHOR DETAILS

List of Tables

- TABLE 1 MARKET DEFINITION, BY CHARGING POINT TYPE

- TABLE 2 MARKET DEFINITION, BY APPLICATION

- TABLE 3 MARKET DEFINITION, BY CHARGING INFRASTRUCTURE TYPE

- TABLE 4 MARKET DEFINITION, BY CHARGING SERVICE TYPE

- TABLE 5 MARKET DEFINITION, BY DC FAST CHARGING TYPE

- TABLE 6 MARKET DEFINITION, BY INSTALLATION TYPE

- TABLE 7 MARKET DEFINITION, BY CHARGE POINT OPERATOR

- TABLE 8 MARKET DEFINITION, BY LEVEL OF CHARGING

- TABLE 9 MARKET DEFINITION, BY OPERATION

- TABLE 10 MARKET DEFINITION, BY CONNECTION PHASE

- TABLE 11 USD EXCHANGE RATES, 2021-2025

- TABLE 12 EV CHARGING SOLUTIONS

- TABLE 13 EV CHARGING INCENTIVES BY KEY COUNTRIES

- TABLE 14 UTILITY MAKE-READY PROGRAMS COVERAGE AND FUNDING, 2025-2026

- TABLE 15 BIDIRECTIONAL EV CHARGERS

- TABLE 16 US: EV SALES WITH BIDIRECTIONAL CHARGING, 2025

- TABLE 17 SMART CHARGING ELEMENTS

- TABLE 18 EV CHARGER TYPES AND UTILIZATION TRENDS

- TABLE 19 CHARGING SUPPLIERS SUPPORTING MEGAWATT CHARGING, 2025-26

- TABLE 20 IMPACT OF MARKET DYNAMICS

- TABLE 21 GDP PERCENTAGE CHANGE, BY COUNTRY, 2021-2030

- TABLE 22 ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 23 AVERAGE SELLING PRICE OF CHARGING POINTS OFFERED BY KEY PLAYERS, 2025 (USD)

- TABLE 24 AVERAGE SELLING PRICE TREND, BY DC CHARGING POINT TYPE, 2023-2025 (USD)

- TABLE 25 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025 (USD)

- TABLE 26 IMPORT DATA FOR HS CODE 8504-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD BILLION)

- TABLE 27 EXPORT DATA FOR HS CODE 8504-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD BILLION)

- TABLE 28 PERFORMANCE INDICATORS FOR EV CHARGING

- TABLE 29 KEY STRATEGIC DEVELOPMENTS IN SOFTWARE DEFINED CHARGING

- TABLE 30 KEY STRATEGIC DEVELOPMENTS IN AI BASED ENERGY MANAGEMENT

- TABLE 31 FEATURES OF BATTERY VS. FLYWHEEL POWER BOOSTERS

- TABLE 32 FEATURES OF FLYWHEEL POWER BOOSTERS

- TABLE 33 KEY CONFERENCES AND EVENTS, 2026-2027

- TABLE 34 PATENT ANALYSIS

- TABLE 35 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 36 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 37 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 38 NETHERLANDS: EV INCENTIVES

- TABLE 39 NETHERLANDS: EV CHARGING STATION INCENTIVES

- TABLE 40 GERMANY: EV INCENTIVES

- TABLE 41 GERMANY: EV CHARGING STATION INCENTIVES

- TABLE 42 FRANCE: EV INCENTIVES

- TABLE 43 FRANCE: EV CHARGING STATION INCENTIVES

- TABLE 44 UK: EV INCENTIVES

- TABLE 45 UK: EV CHARGING STATION INCENTIVES

- TABLE 46 CHINA: EV INCENTIVES

- TABLE 47 CHINA: EV CHARGING STATION INCENTIVES

- TABLE 48 US: EV INCENTIVES

- TABLE 49 US: EV CHARGING STATION INCENTIVES

- TABLE 50 CANADA: EV INCENTIVES

- TABLE 51 CANADA: EV CHARGING STATION INCENTIVES

- TABLE 52 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY LEVEL OF CHARGING (%)

- TABLE 53 KEY BUYING CRITERIA, BY LEVEL OF CHARGING

- TABLE 54 OEM CHARGING INFRASTRUCTURE ROADMAP, 2025-2030+

- TABLE 55 OEM ANALYSIS OF CHARGING INFRASTRUCTURE ECOSYSTEM

- TABLE 56 STRATEGIC IMPACT OF NACS ADOPTION ON EV CHARGING ECOSYSTEM

- TABLE 57 BENCHMARKING OF OEM CHARGING INFRASTRUCTURE STRATEGIES, 2023-2026+

- TABLE 58 CAPEX BREAKDOWN FOR EV CHARGING STATION DEPLOYMENT

- TABLE 59 ESTIMATED REVENUE GENERATION BY CHARGER UTILIZATION SCENARIO

- TABLE 60 FINANCIAL VIABILITY ANALYSIS OF EV CHARGING STATIONS BY UTILIZATION SCENARIO

- TABLE 61 KEY EV CHARGE OPERATORS, BY SUBSCRIPTION AND SERVICE REVENUE MODELS

- TABLE 62 EV CHARGING SOFTWARE PLATFORM BUSINESS MODELS

- TABLE 63 SERVICE AND MAINTENANCE MODELS OFFERED BY EV CHARGING EQUIPMENT SUPPLIERS

- TABLE 64 EV CHARGING FUTURE REVENUE POOLS

- TABLE 65 EV CHARGING STATION MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 66 EV CHARGING STATION MARKET, BY APPLICATION, 2026-2033 (THOUSAND UNITS)

- TABLE 67 PRIVATE: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 68 PRIVATE: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 69 SEMI-PUBLIC: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 70 SEMI-PUBLIC: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 71 PUBLIC: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 72 PUBLIC: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 73 CHINA: CHARGE POINT OPERATORS, 2019-2025 (UNITS)

- TABLE 74 INDIA: CHARGE POINT OPERATORS, 2019-2025 (UNITS)

- TABLE 75 JAPAN: CHARGE POINT OPERATORS, 2019-2025 (UNITS)

- TABLE 76 SOUTH KOREA: CHARGE POINT OPERATORS, 2019-2025 (UNITS)

- TABLE 77 GERMANY: CHARGE POINT OPERATORS, 2019-2025 (UNITS)

- TABLE 78 FRANCE: CHARGE POINT OPERATORS, 2019-2025 (UNITS)

- TABLE 79 UK: CHARGE POINT OPERATORS, 2019-2025 (UNITS)

- TABLE 80 DENMARK: CHARGE POINT OPERATORS, 2019-2025 (UNITS)

- TABLE 81 NETHERLANDS: CHARGE POINT OPERATORS, 2019-2025 (UNITS)

- TABLE 82 NORWAY: CHARGE POINT OPERATORS, 2019-2025 (UNITS)

- TABLE 83 SWITZERLAND: CHARGE POINT OPERATORS, 2019-2025 (UNITS)

- TABLE 84 SPAIN: CHARGE POINT OPERATORS, 2019-2025 (UNITS)

- TABLE 85 US: CHARGE POINT OPERATORS, 2019-2025 (UNITS)

- TABLE 86 CANADA: CHARGE POINT OPERATORS, 2019-2025 (UNITS)

- TABLE 87 EV CHARGING STATION MARKET, BY CHARGING INFRASTRUCTURE TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 88 EV CHARGING STATION MARKET, BY CHARGING INFRASTRUCTURE TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 89 TYPE 1: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 90 TYPE 1: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 91 TYPE 2: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 92 TYPE 2: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 93 CHADEMO: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 94 CHADEMO: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 95 CCS: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 96 CCS: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 97 NACS/TESLA SUPERCHARGER: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 98 NACS/TESLA SUPERCHARGER: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 99 GB/T FAST: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 100 GB/T FAST: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 101 EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 102 EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 103 AC CHARGING: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 104 AC CHARGING: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 105 DC CHARGING: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 106 DC CHARGING: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 107 EV CHARGING POINTS, BY COUNTRY, 2025 (THOUSAND UNITS)

- TABLE 108 BATTERY SWAPPING SERVICES, BY KEY PLAYER

- TABLE 109 EV CHARGING STATION MARKET, BY CONNECTION PHASE, 2022-2025 (THOUSAND UNITS)

- TABLE 110 EV CHARGING STATION MARKET, BY CONNECTION PHASE, 2026-2033 (THOUSAND UNITS)

- TABLE 111 SINGLE-PHASE EV CHARGING STATIONS

- TABLE 112 SINGLE PHASE: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 113 SINGLE PHASE: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 114 THREE-PHASE EV CHARGING STATIONS

- TABLE 115 THREE PHASE: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 116 THREE PHASE: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 117 EV CHARGING STATION MARKET, BY DC FAST CHARGING TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 118 EV CHARGING STATION MARKET, BY DC FAST CHARGING TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 119 SLOW DC CHARGER OFFERINGS, BY KEY PLAYER

- TABLE 120 SLOW DC: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 121 SLOW DC: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 122 FAST DC: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 123 FAST DC: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 124 DC ULTRAFAST 1: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 125 DC ULTRAFAST 1: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 126 DC ULTRAFAST 2: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 127 DC ULTRAFAST 2: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 128 400 KW: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 129 400 KW: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 130 MEGAWATT CHARGING SYSTEMS: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 131 MEGAWATT CHARGING SYSTEMS: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 132 PANTOGRAPH BUS CHARGING

- TABLE 133 OFF-BOARD TOP-DOWN PANTOGRAPH OFFERINGS, BY KEY PLAYER

- TABLE 134 ON-BOARD BOTTOM-UP PANTOGRAPH OFFERINGS, BY KEY PLAYER

- TABLE 135 ELECTRIC BUS CHARGER OFFERINGS, BY KEY PLAYER

- TABLE 136 COMPARISON OF INSTALLATION TYPES

- TABLE 137 EV CHARGING STATION MARKET, BY INSTALLATION TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 138 EV CHARGING STATION MARKET, BY INSTALLATION TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 139 PORTABLE CHARGERS: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 140 PORTABLE CHARGERS: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 141 FIXED CHARGERS: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 142 FIXED CHARGERS: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 143 PARC DATA: EV CHARGING STATION MARKET, BY LEVEL OF CHARGING, 2022-2025 (THOUSAND UNITS)

- TABLE 144 PARC DATA: EV CHARGING STATION MARKET, BY LEVEL OF CHARGING, 2026-2033 (THOUSAND UNITS)

- TABLE 145 NEW SALES: EV CHARGING STATION MARKET, BY LEVEL OF CHARGING, 2022-2025 (THOUSAND UNITS)

- TABLE 146 NEW SALES: EV CHARGING STATION MARKET, BY LEVEL OF CHARGING, 2026-2033 (THOUSAND UNITS)

- TABLE 147 NEW SALES: EV CHARGING STATION MARKET, BY LEVEL OF CHARGING, 2022-2025 (USD MILLION)

- TABLE 148 NEW SALES: EV CHARGING STATION MARKET, BY LEVEL OF CHARGING, 2026-2033 (USD MILLION)

- TABLE 149 LEVEL 1 EV CHARGING STATIONS

- TABLE 150 PARC DATA LEVEL 1: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 151 PARC DATA LEVEL 1: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 152 NEW SALES LEVEL 1: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 153 NEW SALES LEVEL 1: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 154 NEW SALES LEVEL 1: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (USD MILLION)

- TABLE 155 NEW SALES LEVEL 1: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (USD MILLION)

- TABLE 156 LEVEL 2 EV CHARGING STATIONS

- TABLE 157 PARC DATA LEVEL 2: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 158 PARC DATA LEVEL 2: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 159 NEW SALES LEVEL 2: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 160 NEW SALES LEVEL 2: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 161 NEW SALES LEVEL 2: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (USD MILLION)

- TABLE 162 NEW SALES LEVEL 2: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (USD MILLION)

- TABLE 163 LEVEL 3 EV CHARGING STATIONS

- TABLE 164 PARC DATA LEVEL 3: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 165 PARC DATA LEVEL 3: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 166 NEW SALES LEVEL 3: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 167 NEW SALES LEVEL 3: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 168 NEW SALES LEVEL 3: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (USD MILLION)

- TABLE 169 NEW SALES LEVEL 3: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (USD MILLION)

- TABLE 170 EV CHARGING STATION MARKET, BY OPERATION, 2022-2025 (THOUSAND UNITS)

- TABLE 171 EV CHARGING STATION MARKET, BY OPERATION, 2026-2033 (THOUSAND UNITS)

- TABLE 172 MODE 1: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 173 MODE 1: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 174 MODE 2 CHARGING STATISTICS

- TABLE 175 MODE 2: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 176 MODE 2: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 177 MODE 3 CHARGING STATISTICS

- TABLE 178 MODE 3: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 179 MODE 3: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 180 MODE 4 CHARGING STATISTICS

- TABLE 181 MODE 4: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 182 MODE 4: EV CHARGING STATION MARKET, BY COUNTRY/REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 183 EV CHARGING STATION MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 184 EV CHARGING STATION MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 185 EV CHARGING STATION MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 186 EV CHARGING STATION MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 187 ASIA PACIFIC: EV CHARGING STATION MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 188 ASIA PACIFIC: EV CHARGING STATION MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 189 INDIA: EV CHARGING STANDARDS

- TABLE 190 INDIA: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 191 INDIA: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 192 JAPAN: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 193 JAPAN: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 194 SOUTH KOREA: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 195 SOUTH KOREA: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 196 SINGAPORE: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 197 SINGAPORE: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 198 THAILAND: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 199 THAILAND: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 200 TAIWAN: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 201 TAIWAN: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 202 INDONESIA: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 203 INDONESIA: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 204 CHINA: EV CHARGING STATION MARKET HIGHLIGHTS

- TABLE 205 CHINA: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 206 CHINA: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 207 EUROPE: EV CHARGING STATION MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 208 EUROPE: EV CHARGING STATION MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 209 FRANCE: EV CHARGING STATION MARKET HIGHLIGHTS

- TABLE 210 FRANCE: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 211 FRANCE: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 212 GERMANY: EV CHARGING STATION MARKET HIGHLIGHTS

- TABLE 213 GERMANY: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 214 GERMANY: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 215 NETHERLANDS: EV CHARGING STATION MARKET HIGHLIGHTS

- TABLE 216 NETHERLANDS: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 217 NETHERLANDS: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 218 NORWAY: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 219 NORWAY: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 220 SWEDEN: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 221 SWEDEN: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 222 UK: EV CHARGING STATION MARKET HIGHLIGHTS

- TABLE 223 UK: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 224 UK: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 225 DENMARK: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 226 DENMARK: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 227 AUSTRIA: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 228 AUSTRIA: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 229 SPAIN: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 230 SPAIN: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 231 SWITZERLAND: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 232 SWITZERLAND: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 233 NORTH AMERICA: LEADING CHARGING POINT OPERATORS

- TABLE 234 NORTH AMERICA: EV CHARGING STATION MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 235 NORTH AMERICA: EV CHARGING STATION MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 236 CANADA: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 237 CANADA: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 238 US: EV CHARGING STATION MARKET HIGHLIGHTS

- TABLE 239 US: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 240 US: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 241 MIDDLE EAST: EV CHARGING STATION MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 242 MIDDLE EAST: EV CHARGING STATION MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 243 ISRAEL: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (UNITS)

- TABLE 244 ISRAEL: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (UNITS)

- TABLE 245 UAE: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (UNITS)

- TABLE 246 UAE: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (UNITS)

- TABLE 247 SAUDI ARABIA: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (UNITS)

- TABLE 248 SAUDI ARABIA: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (UNITS)

- TABLE 249 REST OF THE WORLD: EV CHARGING STATION MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 250 REST OF THE WORLD: EV CHARGING STATION MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 251 BRAZIL: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (UNITS)

- TABLE 252 BRAZIL: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (UNITS)

- TABLE 253 MEXICO: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 254 MEXICO: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 255 SOUTH AFRICA: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (UNITS)

- TABLE 256 SOUTH AFRICA: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (UNITS)

- TABLE 257 OTHERS: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2022-2025 (UNITS)

- TABLE 258 OTHERS: EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026-2033 (UNITS)

- TABLE 259 KEY PLAYER STRATEGIES/RIGHT TO WIN, JANUARY 2022-MAY 2026

- TABLE 260 CHARGE POINT MANUFACTURERS: DEGREE OF COMPETITION, 2025

- TABLE 261 CHARGE POINT OPERATORS: DEGREE OF COMPETITION, 2025

- TABLE 262 COUNTRY/REGION FOOTPRINT

- TABLE 263 CHARGING POINT FOOTPRINT

- TABLE 264 LEVEL OF CHARGING FOOTPRINT

- TABLE 265 DC FAST CHARGING FOOTPRINT

- TABLE 266 LIST OF STARTUPS/SMES

- TABLE 267 COMPETITIVE BENCHMARKING OF STARTUPS/SMES (1/3)

- TABLE 268 COMPETITIVE BENCHMARKING OF STARTUPS/SMES (2/3)

- TABLE 269 COMPETITIVE BENCHMARKING OF STARTUPS/SMES (3/3)

- TABLE 270 EV CHARGING STATION MARKET: PRODUCT LAUNCHES/DEVELOPMENTS, 2022-2026

- TABLE 271 EV CHARGING STATION MARKET: DEALS, 2022-2026

- TABLE 272 EV CHARGING STATION MARKET: EXPANSIONS, 2022-2026

- TABLE 273 EV CHARGING STATION MARKET: OTHER DEVELOPMENTS, 2022-2026

- TABLE 274 ABB: COMPANY OVERVIEW

- TABLE 275 ABB: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 276 ABB: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 277 ABB: DEALS

- TABLE 278 ABB: EXPANSIONS

- TABLE 279 ABB: OTHER DEVELOPMENTS

- TABLE 280 BYD COMPANY LTD.: COMPANY OVERVIEW

- TABLE 281 BYD COMPANY LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 282 BYD COMPANY LTD.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 283 BYD COMPANY LTD.: DEALS

- TABLE 284 BYD COMPANY LTD.: EXPANSIONS

- TABLE 285 BYD: OTHER DEVELOPMENTS

- TABLE 286 CHARGEPOINT, INC.: COMPANY OVERVIEW

- TABLE 287 CHARGEPOINT, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 288 CHARGPOINT, INC.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 289 CHARGPOINT, INC.: DEALS

- TABLE 290 CHARGPOINT, INC.: OTHER DEVELOPMENTS

- TABLE 291 TESLA: COMPANY OVERVIEW

- TABLE 292 TESLA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 293 TESLA: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 294 TESLA: DEALS

- TABLE 295 TESLA: OTHER DEVELOPMENTS

- TABLE 296 SIEMENS: COMPANY OVERVIEW

- TABLE 297 SIEMENS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 298 SIEMENS: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 299 SIEMENS: DEALS

- TABLE 300 SIEMENS: OTHER DEVELOPMENTS

- TABLE 301 EVBOX: COMPANY OVERVIEW

- TABLE 302 EVBOX: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 303 EVBOX: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 304 EVBOX: DEALS

- TABLE 305 EVBOX: OTHER DEVELOPMENTS

- TABLE 306 DELTA ELECTRONICS, INC.: COMPANY OVERVIEW

- TABLE 307 DELTA ELECTRONICS, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 308 DELTA ELECTRONICS, INC.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 309 DELTA ELECTRONICS, INC.: DEALS

- TABLE 310 STARCHARGE: COMPANY OVERVIEW

- TABLE 311 STARCHARGE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 312 STARCHARGE: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 313 STARCHARGE: DEALS

- TABLE 314 STARCHARGE: EXPANSIONS

- TABLE 315 STARCHARGE: OTHER DEVELOPMENTS

- TABLE 316 SCHNEIDER ELECTRIC: COMPANY OVERVIEW

- TABLE 317 SCHNEIDER ELECTRIC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 318 SCHNEIDER ELECTRIC: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 319 SCHNEIDER ELECTRIC: DEALS

- TABLE 320 SCHNEIDER ELECTRIC: EXPANSIONS

- TABLE 321 KEMPOWER OYJ: COMPANY OVERVIEW

- TABLE 322 KEMPOWER OYJ: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 323 KEMPOWER OYJ.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 324 KEMPOWER OYJ: DEALS

- TABLE 325 KEMPOWER OYJ: EXPANSIONS

- TABLE 326 KEMPOWER OYJ: OTHER DEVELOPMENTS

- TABLE 327 EFACEC: COMPANY OVERVIEW

- TABLE 328 EFACEC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 329 EFACEC: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 330 EFACEC: DEALS

- TABLE 331 EFACEC: EXPANSIONS

- TABLE 332 EFACEC: OTHER DEVELOPMENTS

- TABLE 333 SHELL PLC: COMPANY OVERVIEW

- TABLE 334 SHELL PLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 335 SHELL PLC: DEALS

- TABLE 336 SHELL PLC: EXPANSIONS

- TABLE 337 SHELL PLC: OTHER DEVELOPMENTS

- TABLE 338 TOTALENERGIES: COMPANY OVERVIEW

- TABLE 339 TOTALENERGIES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 340 TOTALENERGIES: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 341 TOTALENERGIES: DEALS

- TABLE 342 TOTALENERGIES: OTHER DEVELOPMENTS

- TABLE 343 BP P.L.C.: COMPANY OVERVIEW

- TABLE 344 BP P.L.C.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 345 BP P.L.C.: DEALS

- TABLE 346 BP P.L.C.: EXPANSIONS

- TABLE 347 BP P.L.C.: OTHER DEVELOPMENTS

- TABLE 348 ENEL X S.R.L.: COMPANY OVERVIEW

- TABLE 349 ENEL X S.R.L.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 350 ENEL X S.R.L.: DEALS

- TABLE 351 ENEL X S.R.L.: EXPANSIONS

- TABLE 352 ENEL X S.R.L.: OTHER DEVELOPMENTS

- TABLE 353 VIRTA GLOBAL: COMPANY OVERVIEW

- TABLE 354 VIRTA GLOBAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 355 VIRTA GLOBAL: DEALS

- TABLE 356 VIRTA GLOBAL: OTHER DEVELOPMENTS

- TABLE 357 ALLEGO B.V.: COMPANY OVERVIEW

- TABLE 358 ALLEGO B.V.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 359 ALLEGO B.V.: DEALS

- TABLE 360 ALLEGO B.V.: EXPANSIONS

- TABLE 361 ALLEGO B.V.: OTHER DEVELOPMENTS

- TABLE 362 TGOOD ELECTRIC CO., LTD.: COMPANY OVERVIEW

- TABLE 363 TGOOD ELECTRIC CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 364 TGOOD ELECTRIC CO., LTD.: DEALS

- TABLE 365 TGOOD ELECTRIC CO. LTD.: OTHER DEVELOPMENTS

- TABLE 366 STATE GRID CORPORATION CHINA: COMPANY OVERVIEW

- TABLE 367 STATE GRID CORPORATION CHINA: DEALS

- TABLE 368 STATE GRID CORPORATION CHINA: EXPANSIONS

- TABLE 369 VATTENFALL AB: COMPANY OVERVIEW

- TABLE 370 VATTENFALL AB: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 371 VATTENFALL AB: DEALS

- TABLE 372 VATTENFALL AB: EXPANSIONS

- TABLE 373 VATTENFALL AB: OTHER DEVELOPMENTS

- TABLE 374 BLINK CHARGING CO.: COMPANY OVERVIEW

- TABLE 375 ENPHASE ENERGY: COMPANY OVERVIEW

- TABLE 376 ELECTRIFY AMERICA: COMPANY OVERVIEW

- TABLE 377 OPCONNECT: COMPANY OVERVIEW

- TABLE 378 EV SAFE CHARGE INC.: COMPANY OVERVIEW

- TABLE 379 IONITY: COMPANY OVERVIEW

- TABLE 380 WALLBOX: COMPANY OVERVIEW

- TABLE 381 SPARK HORIZON: COMPANY OVERVIEW

- TABLE 382 DBT: COMPANY OVERVIEW

- TABLE 383 CHARGE+: COMPANY OVERVIEW

- TABLE 384 ALFEN NV: COMPANY OVERVIEW

- TABLE 385 IES SYNERGY: COMPANY OVERVIEW

- TABLE 386 MADIC GROUP: COMPANY OVERVIEW

- TABLE 387 BEEV: COMPANY OVERVIEW

- TABLE 388 INSTAVOLT: COMPANY OVERVIEW

- TABLE 389 FRESHMILE: COMPANY OVERVIEW

- TABLE 390 POD POINT: COMPANY OVERVIEW

- TABLE 391 BE CHARGE: COMPANY OVERVIEW

- TABLE 392 MER: COMPANY OVERVIEW

- TABLE 393 ENBW: COMPANY OVERVIEW

- TABLE 394 RWE: COMPANY OVERVIEW

- TABLE 395 POWERDOT: COMPANY OVERVIEW

- TABLE 396 SPARKCHARGE: COMPANY OVERVIEW

- TABLE 397 JOLT: COMPANY OVERVIEW

- TABLE 398 INSTALLER: COMPANY OVERVIEW

- TABLE 399 NUMBAT: COMPANY OVERVIEW

- TABLE 400 ITSELECTRIC INC: COMPANY OVERVIEW

List of Figures

- FIGURE 1 MARKET SCENARIO

- FIGURE 2 EV CHARGING STATION MARKET, 2022-2033

- FIGURE 3 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN EV CHARGING STATION MARKET

- FIGURE 4 DISRUPTIONS INFLUENCING GROWTH OF EV CHARGING STATION MARKET

- FIGURE 5 HIGH-GROWTH SEGMENTS IN EV CHARGING STATION MARKET

- FIGURE 6 CHINA TO BE LEADING MARKET DURING FORECAST PERIOD

- FIGURE 7 STRONG GOVERNMENT MANDATES AND HEAVY INVESTMENTS IN EV CHARGING INFRASTRUCTURE TO DRIVE MARKET

- FIGURE 8 LEVEL 3 SEGMENT TO BE DOMINANT DURING FORECAST PERIOD

- FIGURE 9 DC CHARGING TO BE LARGER THAN AC CHARGING DURING FORECAST PERIOD

- FIGURE 10 GB/T FAST TO EXHIBIT FASTEST GROWTH DURING FORECAST PERIOD

- FIGURE 11 PUBLIC TO SURPASS OTHER SEGMENTS DURING FORECAST PERIOD

- FIGURE 12 DC ULTRAFAST 1 TO BE LARGEST SEGMENT DURING FORECAST PERIOD

- FIGURE 13 FIXED CHARGERS TO CAPTURE HIGHER SHARE THAN PORTABLE CHARGERS DURING FORECAST PERIOD

- FIGURE 14 MODE 4 TO SECURE LEADING POSITION DURING FORECAST PERIOD

- FIGURE 15 THREE PHASE SEGMENT TO GROW FASTER THAN SINGLE PHASE SEGMENT DURING FORECAST PERIOD

- FIGURE 16 CHINA TO BE LARGEST MARKET FOR EV CHARGING STATIONS IN 2026

- FIGURE 17 CHARGING INFRASTRUCTURE SOLUTIONS

- FIGURE 18 EV CHARGING STATION MARKET DYNAMICS

- FIGURE 19 TYPES OF EV CHARGING SOCKETS

- FIGURE 20 EV CHARGING STANDARDS

- FIGURE 21 OVERVIEW OF V2G CHARGING STATIONS

- FIGURE 22 BENEFITS OF SMART EV CHARGING

- FIGURE 23 IOT IN EV CHARGING

- FIGURE 24 SERVICE OFFERINGS IN EV CHARGING

- FIGURE 25 EV CHARGING THROUGH SOLAR POWER

- FIGURE 26 BATTERY SWAPPING STATION BUSINESS MODELS

- FIGURE 27 GLOBAL ENERGY CONSUMPTION, 2025

- FIGURE 28 GLOBAL ELECTRIC VEHICLE INDUSTRY, 2022-2035

- FIGURE 29 ECOSYSTEM ANALYSIS

- FIGURE 30 SUPPLY CHAIN ANALYSIS

- FIGURE 31 BILL OF MATERIALS FOR AC (LEVEL 2) CHARGING POINTS, 2026 VS. 2033

- FIGURE 32 BILL OF MATERIALS FOR DC SLOW CHARGING POINTS, 2026 VS. 2033

- FIGURE 33 BILL OF MATERIALS FOR DC FAST CHARGING POINTS, 2026 VS. 2033

- FIGURE 34 BILL OF MATERIALS FOR DC ULTRAFAST 1 CHARGING POINTS, 2026 VS. 2033

- FIGURE 35 AVERAGE SELLING PRICE TREND, BY DC CHARGING POINT TYPE, 2023-2025 (USD)

- FIGURE 36 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025 (USD)

- FIGURE 37 IMPORT DATA FOR HS CODE 8504-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD BILLION)

- FIGURE 38 EXPORT DATA FOR HS CODE 8504-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD BILLION)

- FIGURE 39 INVESTMENT AND FUNDING SCENARIO, 2022-2025

- FIGURE 40 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 41 WIRELESS CHARGING PROJECTS IN EUROPE

- FIGURE 42 BIDIRECTIONAL CHARGING ENERGY FLOW CYCLE

- FIGURE 43 MEGAWATT CHARGING PROJECTS, BY REGION

- FIGURE 44 SMART CHARGING SYSTEMS

- FIGURE 45 ROLE OF IOT IN EV CHARGING STATIONS

- FIGURE 46 PATENT ANALYSIS

- FIGURE 47 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY LEVEL OF CHARGING

- FIGURE 48 KEY BUYING CRITERIA, BY LEVEL OF CHARGING

- FIGURE 49 FRAMEWORK OF EV CHARGING BUSINESS MODELS

- FIGURE 50 CHARGING AS A SERVICE BUSINESS MODEL

- FIGURE 51 OEM INTEGRATED CHARGING ECOSYSTEM MODEL

- FIGURE 52 FLEET CHARGING BUSINESS MODEL

- FIGURE 53 EV CHARGING STATION MARKET, BY APPLICATION, 2026-2033 (THOUSAND UNITS)

- FIGURE 54 PORSCHE TAYCAN CHARGING CONNECTORS

- FIGURE 55 EV CHARGING STATION MARKET, BY CHARGING INFRASTRUCTURE TYPE, 2026 VS 2033 (THOUSAND UNITS)

- FIGURE 56 TYPE 1 CHARGER INSIGHTS

- FIGURE 57 TYPE 2 CHARGER INSIGHTS

- FIGURE 58 CHADEMO CHARGER INSIGHTS

- FIGURE 59 CCS CHARGER INSIGHTS

- FIGURE 60 NACS/TESLA SUPERCHARGER INSIGHTS

- FIGURE 61 GB/T FAST CHARGER INSIGHTS

- FIGURE 62 EV CHARGING STATION MARKET, BY CHARGING POINT TYPE, 2026 VS 2033 (THOUSAND UNITS)

- FIGURE 63 FLOW FIGURE FOR AUTOMATED BATTERY SWAPPING

- FIGURE 64 EV CHARGING STATION MARKET, BY CONNECTION PHASE, 2026 VS 2033 (THOUSAND UNITS)

- FIGURE 65 EV CHARGING STATION MARKET, BY DC FAST CHARGING TYPE, 2026 VS 2033 (THOUSAND UNITS)

- FIGURE 66 MEGAWATT CHARGING SYSTEM ECOSYSTEM

- FIGURE 67 COMPARISON OF ELECTRIC BUS CHARGING TYPES

- FIGURE 68 EV CHARGING STATION MARKET, BY INSTALLATION TYPE, 2026 VS 2033 (THOUSAND UNITS)

- FIGURE 69 EV CHARGING STATION MARKET, BY LEVEL OF CHARGING, 2026 VS 2033 (USD MILLION)

- FIGURE 70 COMPARISON OF EV CHARGING LEVELS

- FIGURE 71 EV CHARGING STATION MARKET, BY OPERATION, 2026 VS 2033 (THOUSAND UNITS)

- FIGURE 72 COMPARISON OF OPERATION MODES

- FIGURE 73 EV CHARGING STATION MARKET, BY REGION, 2026 VS. 2033 (USD MILLION)

- FIGURE 74 ASIA PACIFIC: EV CHARGING STATION MARKET SNAPSHOT

- FIGURE 75 EUROPE: EV CHARGING STATION MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- FIGURE 76 NORTH AMERICA: EV CHARGING STATION MARKET SNAPSHOT

- FIGURE 77 MIDDLE EAST: EV CHARGING STATION MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- FIGURE 78 REST OF THE WORLD: EV CHARGING STATION MARKET, BY COUNTRY, 2026 VS. 2033 (THOUSAND UNITS)

- FIGURE 79 CHARGE POINT MANUFACTURERS: MARKET SHARE ANALYSIS, 2025

- FIGURE 80 CHARGE POINT OPERATORS: MARKET SHARE ANALYSIS, 2025

- FIGURE 81 CHARGE POINT MANUFACTURERS: REVENUE ANALYSIS, 2021-2025 (USD BILLION)

- FIGURE 82 CHARGE POINT OPERATORS: REVENUE ANALYSIS, 2021-2025 (USD BILLION)

- FIGURE 83 COMPANY VALUATION OF KEY CHARGE POINT MANUFACTURERS

- FIGURE 84 FINANCIAL METRICS OF KEY CHARGE POINT MANUFACTURERS

- FIGURE 85 COMPANY VALUATION OF KEY CHARGE POINT OPERATORS

- FIGURE 86 FINANCIAL METRICS OF KEY CHARGE POINT OPERATORS

- FIGURE 87 BRAND/PRODUCT COMPARISON

- FIGURE 88 COMPANY EVALUATION MATRIX (CHARGE POINT MANUFACTURERS), 2025

- FIGURE 89 COMPANY EVALUATION MATRIX (CHARGE POINT OPERATORS), 2025

- FIGURE 90 COMPANY FOOTPRINT

- FIGURE 91 COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2025

- FIGURE 92 ABB: COMPANY SNAPSHOT

- FIGURE 93 BYD COMPANY LTD.: COMPANY SNAPSHOT

- FIGURE 94 CHARGEPOINT, INC.: COMPANY SNAPSHOT

- FIGURE 95 TESLA: COMPANY SNAPSHOT

- FIGURE 96 SIEMENS: COMPANY SNAPSHOT

- FIGURE 97 DELTA ELECTRONICS, INC.: COMPANY SNAPSHOT

- FIGURE 98 SCHNEIDER ELECTRIC: COMPANY SNAPSHOT

- FIGURE 99 KEMPOWER OYJ: COMPANY SNAPSHOT

- FIGURE 100 SHELL PLC: COMPANY SNAPSHOT

- FIGURE 101 TOTALENERGIES: COMPANY SNAPSHOT

- FIGURE 102 BP P.L.C.: COMPANY SNAPSHOT

- FIGURE 103 ENEL X S.R.L.: COMPANY SNAPSHOT

- FIGURE 104 ALLEGO B.V.: COMPANY SNAPSHOT

- FIGURE 105 RESEARCH DESIGN

- FIGURE 106 RESEARCH PROCESS FLOW

- FIGURE 107 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 108 BOTTOM-UP APPROACH

- FIGURE 109 TOP-DOWN APPROACH

- FIGURE 110 DATA TRIANGULATION

- FIGURE 111 FACTORS IMPACTING EV CHARGING STATION MARKET

- FIGURE 112 DEMAND- AND SUPPLY-SIDE FACTOR ANALYSIS