PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1640357

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1640357

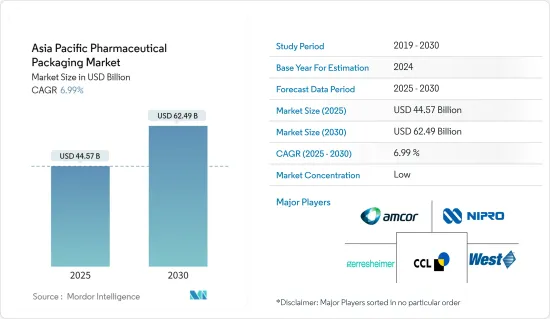

Asia Pacific Pharmaceutical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Asia Pacific Pharmaceutical Packaging Market size is estimated at USD 44.57 billion in 2025, and is expected to reach USD 62.49 billion by 2030, at a CAGR of 6.99% during the forecast period (2025-2030).

Key Highlights

- Pharmaceutical packaging involves the assembly of elements required to enclose, maintain, safeguard, and distribute a secure and effective medicinal product, ensuring that a secure and effective dosage form is accessible at any given time prior to the drug product's expiration date. Appropriate packaging materials are essential for offering tamper-evident security, which aids in deterring the consumption of counterfeit medications. Furthermore, premium packaging materials must comply with rigorous regulatory guidelines.

- The pharmaceutical packaging manufacturers are anticipated to witness significant opportunities in Asia-Pacific, thanks to the increasing investments in the pharmaceutical sector. The rising demand for pharmaceutical drugs and advancements in pharmaceutical technology are directly contributing to the demand for glass bottles, ampules, and other glass packaging solutions. As chronic illnesses continue to rise and the production of COVID-19 vaccine doses remains substantial, the demand for primary packaging is expected to surge, specifically for glass containers.

- Glass packaging is expected to drive the market's growth in the region's pharma packaging sector. Pharmaceutical companies utilize glass containers to package a diverse array of pharmaceutical products, including injectable medications, solid oral pills, liquid formulations, and biologics. The rapid growth of glass packaging is driven by factors such as pharmaceutical manufacturing operations, the rising demand for specialty pharmaceuticals, and the expansion of healthcare infrastructure. This trend is particularly evident in countries like China, India, Japan, and South Korea, where pharmaceutical industries are experiencing significant growth, leading to a surge in demand for glass packaging solutions.

- The plastic bottles industry is projected to experience substantial growth in the coming years. The utilization of PET is steadily increasing in the region, resulting in a weight reduction of up to 90% compared to glass, thus enabling a more cost-effective transportation procedure. Presently, plastic bottles crafted from PET are extensively substituting bulky and delicate glass bottles in the pharmaceutical sector, providing reusable packaging for different liquids. The rising advancements in plastic PET technology for the pharmaceutical industry are anticipated to boost market prospects.

- Additionally, the government's initiatives to enhance the pharmaceutical sector in the area are anticipated to propel the market's expansion. For example, the measures implemented by the Chinese government to expedite the modernization of the nation's healthcare system are projected to stimulate the advancement of the pharmaceutical packaging industry. Moreover, China is proactively improving its pharmaceutical packaging infrastructure and resources while broadening its range of pharmaceutical products, potentially opening up new avenues for pharmaceutical packaging companies.

- China's presence in the global pharmaceutical market has been steadily growing, serving as both a major consumer and a vital component in the global pharmaceutical industry and supply chains. The rapid expansion of the pharmaceutical sector in recent years, driven by scientific and technological advancements, is projected to continue in the future. In December 2023, Danish pharmaceutical firm Novo Nordisk revealed its plan to invest CNY 400 million (USD 59.6 million) in a newly established company in the region by June 2026. These substantial developments are anticipated to drive the demand for pharmaceutical packaging services.

- The packaging industry experienced significant effects due to the COVID-19 pandemic. With a shift in focus toward infectious diseases and vaccines, there was a decrease in successful clinical trials and research and development activities in therapeutic areas like diabetes and hypertension. However, the pharmaceutical industry witnessed a surge in drug demand for various diseases during the pandemic, leading to substantial investments in the packaging business. Fortunately, the pharmaceutical industry quickly recovered by emphasizing the need for safe and hygienic packaging in response to the pandemic.

Asia Pacific Pharmaceutical Packaging Market Trends

Glass Packaging is Expected to Witness Significant Growth

- Glass packaging is widely considered the leading choice for pharmaceutical products in the packaging industry. Its popularity stems from its sustainable nature, inertness, impermeability, recyclability, and ability to be reused without compromising quality. The COVID-19 pandemic further fueled the demand for glass packaging as the need for medication significantly increased. With the approval and distribution of new drugs and vaccines by pharmaceutical manufacturers in various countries, the use of glass packaging is expected to continue expanding.

- Glass packaging is primarily provided as the main packaging option for pharmaceutical products and is one of the top choices in the pharmaceutical industry. This is mainly because it offers several advantages, including sustainability, inertness, impermeability, recyclability without any compromise in quality, and reusability. Glass containers have become widely utilized in the pharmaceutical sector as one of the primary packaging materials. As the prevalence of chronic diseases increases and the production of COVID-19 vaccine doses continues to rise, there is an anticipated surge in the demand for primary packaging, specifically glass containers.

- The increasing prevalence of chronic diseases in the APAC region is a major factor driving the expansion of the pharmaceutical packaging market. Conditions such as diabetes, cardiovascular diseases, cancer, and respiratory ailments necessitate continuous medication. As a result, there is a rising need for diverse pharmaceutical packaging solutions to securely store, safeguard, and distribute these medications with optimal efficiency. As per the World Health Organization (WHO), the rise in noncommunicable diseases is contributing to the escalating burden of chronic illnesses in the region, especially in the SEA region.

- The primary packaging glass solutions manufacturer, Stoelzle, unveiled their latest eco-friendly PharmaCos line at the CPHI Barcelona trade show in November 2023. This new line of packaging solutions boasts a high percentage of recycled glass (73% in amber glass and 38% in flint glass) and lightweight bottle design. Additionally, the new line is produced in a pharmaceutical-grade facility to meet the strict standards of the healthcare industry. Such significant innovations by the vendors are expected to drive the market's growth.

- Bormioli Pharma states that currently, various recycled glass products are available specifically designed for type II and type III glass. These products utilize materials sourced from an external supply chain that is certified for pharmaceutical use. Through chemical and mechanical processing, the recycled materials can be transformed into glass powder, which serves as the foundation for the new production cycle. Simultaneously, Bormioli Pharma is actively involved in projects aimed at developing low-emission furnaces. These furnaces incorporate innovative technologies and industrial processes that minimize their environmental footprint.

- Moreover, the market for glass packaging techniques in countries like Japan will be driven by the increasing investments made by pharmaceutical vendors to enhance pharmaceutical production. A notable example is Takeda's announcement in March 2023, stating its plan to invest approximately JPY 100 billion (USD 0.75 billion) in constructing a new manufacturing facility for plasma-derived therapies (PDTs) in Osaka, Japan. This investment represents Takeda's largest-ever expansion of manufacturing capacity in Japan. The upcoming state-of-the-art facility, expected to be operational by 2030, will be the largest of its kind in the country and will significantly increase Takeda's plasma manufacturing capacity.

India is Expected to Witness Significant Growth

- India is expected to be one of the fastest-growing regions in the pharmaceutical packaging market. The pharmaceutical packaging sector has witnessed significant growth in recent years, driven by innovations and the rise of new treatments. The onset of the COVID-19 pandemic underscored the importance of efficient product packaging and distribution. As a result, there's a growing emphasis on accelerating both manufacturing and distribution processes, including packaging. Consequently, packaging firms are under mounting pressure to innovate swiftly, meeting the demand for faster operations.

- India is anticipated to emerge as a key player in the pharmaceutical sector, especially in the production of generic drugs and cost-effective medication. The country plays a vital role as a primary provider of generic medicines to numerous advanced nations. The rising output and international distribution of generic drugs are significant factors driving the expansion of the Indian pharmaceutical packaging industry. Additionally, the surge in chronic illnesses and the rise in investments in drug manufacturing operations will lead to a substantial increase in demand within the market.

- The region is anticipated to experience a notable increase in demand for plastic packaging types. The surge in the need for medical supplies and medications has propelled the expansion of plastic pharma packaging in India. Numerous companies are making substantial investments in this technology to enhance the region's market potential. For instance, in March 2023, Spanish packaging company Inden Pharma intended to broaden its operations in India through a partnership with Austria-based ALPLApharma, which specializes in plastic packaging for pharmaceuticals. These noteworthy advancements are projected to stimulate growth in the market.

- InvestIndia reports that India is the largest global provider of generic medicines, making up 20% of the global supply by volume. Additionally, India is the top producer of vaccines worldwide. Outside of the United States, India has the highest number of pharmaceutical plants that comply with the standards set by the US Food and Drug Administration (US FDA). With over 3,000 pharmaceutical companies and more than 10,500 manufacturing facilities, India possesses a robust network and a highly skilled workforce in the pharmaceutical industry. Moreover, India fulfills approximately 60% of the global demand for vaccines and is a major supplier of DPT, BCG, and Measles vaccines. These extensive capabilities in pharmaceutical manufacturing will undoubtedly stimulate the packaging business market in the region.

- Moreover, InvestIndia states that the Indian pharmaceutical industry experienced an average growth rate of 9.47% from FY18 to FY22, reaching USD 42.34 Billion, mainly due to increased exports and a growing domestic market. Forecasts suggest that the pharma sector is expected to reach a value of USD 65 billion in 2024 and USD 120 billion in 2030. To ensure sustained growth, the government has implemented various initiatives to promote research and innovation. As part of its vision for 2047, the government aims to establish India as a global leader in producing affordable, innovative, and high-quality pharmaceuticals and medical devices, in line with the principle of Vasudhaiva Kutumbakam. Such significant developments will provide market opportunities in the packaging sector.

Asia Pacific Pharmaceutical Packaging Industry Overview

The Asia-Pacific pharmaceutical packaging market is competitive, with many regional and global players. Some major players are Amcor Ltd, West Pharmaceutical Services Inc., West Pharmaceutical Services Inc., CCL Industries Inc., and NIPRO Corporation. Companies are increasing their market share by launching new products and expanding production units. Some of the recent developments are:

- January 2024: Loop Industries Inc., a clean technology company whose mission is to accelerate a circular plastics economy by manufacturing 100% recycled polyethylene terephthalate ("PET") plastic and polyester fiber, and Bormioli Pharma, an international player in pharmaceutical packaging and medical devices, launched an innovative pharmaceutical packaging bottle manufactured with 100% recycled virgin quality Loop PET resin.

- June 2023: CIncorporated partnered with SGD Pharma to establish a state-of-the-art facility for producing pharmaceutical packaging glass in Telangana. It was reported that the two companies would collectively invest more than INR 500 crore in setting up this facility. This collaboration with Corning is a significant move in advancing converting technology within the pharmaceutical sector and ensuring a robust supply chain. By working together, these companies aim to assist pharmaceutical manufacturers in addressing the growing challenges related to capacity and quality, as well as meeting the rising global demand for essential medications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Supplier

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Drivers

- 4.4.1 Increasing Adoption of Pharmaceutical Packaging in Emerging Economies

- 4.5 Market Restraints

- 4.5.1 Fluctuations in Raw Material Cost

5 MARKET SEGMENTATION

- 5.1 By Material

- 5.1.1 Plastic

- 5.1.2 Paper and Paper Board

- 5.1.3 Glass

- 5.1.4 Aluminum Foil

- 5.2 By Type

- 5.2.1 Ampoules

- 5.2.2 Blister Packs

- 5.2.3 Plastic Bottles

- 5.2.4 Syringes

- 5.2.5 Vials

- 5.2.6 IV fluids

- 5.2.7 Other Types

- 5.3 By Drug Delivery Mode

- 5.3.1 Oral Drug packaging

- 5.3.2 Injectable Drug packaging

- 5.3.3 Pulmonary Drug Packaging

- 5.3.4 Other Drug Delivery Modes

- 5.4 By Country

- 5.4.1 India

- 5.4.2 Japan

- 5.4.3 China

- 5.4.4 Australia

- 5.4.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Amcor Ltd

- 6.1.2 CCL Industries Inc.

- 6.1.3 West Pharmaceutical Services Inc.

- 6.1.4 Gerresheimer AG

- 6.1.5 Schott AG

- 6.1.6 NIPRO Corporation

- 6.1.7 Wihuri Group

- 6.1.8 Klockner Pentaplast Group

- 6.1.9 Catalent Pharma Solutions Inc.

- 6.1.10 Berry Global Group Inc.

7 INVESTMENT ANALYSIS

8 FUTURE OF THE MARKET