PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1685860

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1685860

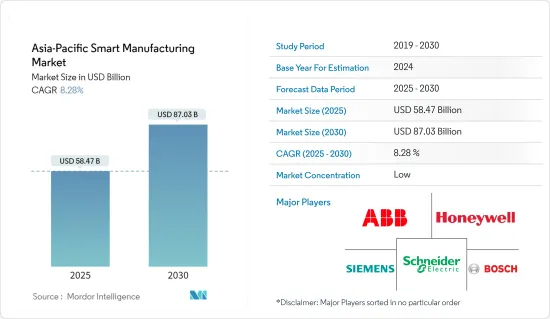

Asia-Pacific Smart Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Asia-Pacific Smart Manufacturing Market size is estimated at USD 58.47 billion in 2025, and is expected to reach USD 87.03 billion by 2030, at a CAGR of 8.28% during the forecast period (2025-2030).

Manufacturing is one of the most significant contributors to Asia-Pacific's economy and is undergoing a rapid transformation. As the population ages, along with rising labor costs in Europe and North America, the legacy model based on inexpensive workers is no longer sustainable. Due to such factors, low-end manufacturing firms are increasingly moving their operations to Southeast Asia to cut costs.

Key Highlights

- Industry 4.0 is the latest revolution in the manufacturing landscape. Factories integrate production machines, wireless connectivity, and sensors and link them to a system platform ecosystem that oversees the production line process and executes decisions autonomously. With the help of smart manufacturing, regional manufacturers can transform businesses and achieve significant value by leveraging the Industrial Internet of Things (IIoT), cloud, and analytics solutions.

- Big data analytics can refine complicated processes and support new business models, like mass customization and product-as-a-service (which can be made possible by smart manufacturing), apart from the traditional operational models like "on-demand." As big data analytics allows an enterprise to use smart manufacturing to shift from reactionary practices to predictive ones, The increase in industrial 4.0 practices across various manufacturing industries provides more scope for accepting big data analytics in the region.

- Manufacturing has emerged as one of the high-growth sectors in India. The "Make in India" program places India on the world map as a manufacturing hub and provides global recognition to the Indian economy. In order to succeed in the "Make in India" program, manufacturers in India need to manufacture more efficiently and deploy innovation to stay competitive. Smart manufacturing solutions can help with that. Manufacturers can focus more on enhancing competitiveness by streamlining supply chains, reducing costs, and improving safety in the workplace. Simultaneously, solutions like robotics, analytics, and cybersecurity strengthen their ability to meet quality norms.

- Further, the automated industrial economy has opened in Japan, and the development of Industrial Version 4.0 is speeding up. Japan has become a manufacturing hub for factory automation products, supplying them to other regional markets in the Asia-Pacific region and making factory automation more affordable. Products from Japan are prone to lower shipment costs and have better after-sales support networks in the region.

- With the Made in China 2025 initiative allowing the relocation of manufacturing back to China, Southeast Asian countries are under pressure to ascertain and minimize the risk of labor issues, and Industry 4.0 is currently impacting smart manufacturing development in the region. Moreover, most regional companies need to become more familiar with the benefits of Industry 4.0 on productivity and growth. It is estimated that if adopted and implemented correctly, Industry 4.0 has the potential to increase productivity by 30-40%.

APAC Smart Manufacturing Market Trends

Oil and Gas is Expected to Hold Significant Share

- The oil and gas end-user industry is one of the earliest pioneers of predictive maintenance due to the need to lower the cost of maintenance while mitigating the risks of environmental disasters due to sensors that can now be easily installed into and onto machinery. These sensors can easily feed the data into specially developed predictive algorithms that warn them about potential failures. Long-term growth in the need for energy means that the oil and gas industry faces many problems along its entire value chain and needs a lot of new technology.

- A lot of data is being generated in the oil and gas sector. A large part of this data consists of exploration, production, and reservoir data logs, such as well logs, seismic surveys, conventional and special core analyses, static and flowing pressure measurements, fluid analyses, pressure-transient tests, and periodic functional production tests, among others. Due to such factors, an enormous opportunity has been created for the vendors to offer a solution for data management and advanced analytical tools.

- Vendors in the region have been offering solutions that allow companies to use AI technologies, such as natural language processing and computer vision, to extract data from these documents automatically. Such demands for real-time analysis and data visualization have driven partnerships with analytics solution providers. The ongoing shift to becoming smart is expected to present even more significant potential, given the strategic push by many companies to expand their downstream operations in the oil and gas value chain, especially petrochemicals.

- Asia Pacific is third in terms of the region with the most oil and gas rigs after North America and the Middle East. For instance, according to Baker Hughes, there are around 86 offshore and 120 onshore oil and gas rigs, making a total of 206 in the cording to Baker Hughes, there are around 86 offshore and 120 onshore oil and gas rigs, making a total of 206 in the Asia-Pacific region as of October 2022.

- Moreover, according to British Petroleum (BP), the oil production in Asia-Pacific amounted to roughly 7.34 million barrels per day in 2021 and is expected to increase more in the near future. The vendor of smart manufacturing can take advantage of this opportunity to increase their revenue.

China is Expected to Hold Major Share

- China is an integral part of Asia's growing shift to intelligent applications. The Chinese government has strengthened the design of smart manufacturing by implementing various schemes and demonstrations in developing standard systems. China aims to create 40 manufacturing innovations by 2025. The focus areas include automated machine tools and robotics, new advanced information technology, aerospace and aeronautical equipment, marine equipment, high-tech shipping, modern rail transport equipment, new-energy vehicles and equipment, power equipment, agricultural equipment, new materials, and biopharma and advanced medical products.

- The Chinese government has built a roadmap to become the leading AI superpower by 2030. Considering AI development and proliferation, the government focuses on integrating AI technology in China's factories to harness and adopt the techniques of integrated intelligent systems, which possess networked vehicles, service robots, drones, video image identification systems, voice interaction systems, smart sensors, neural networks, and chips.

- Many medium and large manufacturers in China are initiating the use of data analytics to optimize factory operations, boost equipment utilization and product quality, and simultaneously reduce energy consumption and production costs. With the latest supply-network management tools, factory operational managers have a clearer view of raw materials and manufactured parts flowing through a manufacturing network that can help them schedule manufacturing operations and product deliveries to reduce costs and improve efficiency. With the active use of data mining technology, engineers and technicians are acquiring new insight into machine failure to enhance reliability.

- Moreover, in November 2022, China's Ministry of Industry and Information Technology announced that it had approved the establishment of three new national manufacturing innovation centers. In addition, they said that these centers would concentrate on key generic technologies and enhance technological research and development in these industries. Furthermore, the ministry said it would guide the new manufacturing innovation centers to strengthen their capabilities to seek technological innovation to deliver strong support for the high-quality development of primary fields in manufacturing.

- According to the National Bureau of Statistics of China, industrial robots' production volume amounted to over 363,000 units in China in 2021, an increase of more than 50% compared to 2020. As China's production capability grows, the demand for industrial robots also increases.

APAC Smart Manufacturing Industry Overview

The Asia-Pacific Smart Manufacturing Market is quite fragmented, as there are numerous international companies such as ABB Ltd., Honeywell International Inc., Siemens AG, Schneider Electric, and Robert Bosch offering various solutions related to control systems, robotics, machine vision systems, and analytics to enhance the productivity of manufacturing processes across the end-user verticals. The companies in the market are undergoing various partnerships and product innovations to increase their market share.

In March 2022, Honeywell and Oriental Energy Company Ltd. reported that a sustainable aviation fuel (SAF) production facility would be built in Maoming, Guangdong Province, in China, with an annual output capacity of 1 million tons. The new building will help meet the growing demand for SAF, make it easier to reduce greenhouse gas emissions in the production of aviation fuel through the use of new technologies, and help China reach its goal of being carbon neutral by 2060.

Siemens and NVIDIA announced in June 2022 that they would change their partnership to make the industrial metaverse possible and increase the use of AI-driven digital twin technology, which will help take industrial automation to a new level. This partnership also lets them connect Siemens Xcelerator, an open digital business platform, and NVIDIA Omniverse, a platform for 3D design and collaboration. This will create an industrial metaverse with physics-based digital models from Siemens and real-time AI from NVIDIA, which will help organizations make decisions faster and with more confidence.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the Overall Manufacturing Industry and Their Spending on Digital Initiatives

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Diversification Strategies being Adopted by the Manufacturing Companies

- 5.1.2 Initiatives Undertaken by the Government to Increase Growth in Manufacturing Sector

- 5.2 Market Challenges

- 5.2.1 Lack of Awareness, Skilled Workforce and Complexity in Implementation

- 5.2.2 Huge Capital Investments for Transformations

6 MARKET SEGMENTATION

- 6.1 Enabling Technologies

- 6.1.1 Industrial Control Systems

- 6.1.1.1 Programmable Logic Controller (PLC)

- 6.1.1.2 Supervisory Controller and Data Acquisition (SCADA)

- 6.1.1.3 Distributed Control System (DCS)

- 6.1.1.4 Human Machine Interface (HMI)

- 6.1.1.5 Product Lifecycle Management (PLM)

- 6.1.1.6 Manufacturing Execution System (MES)

- 6.1.2 Industrial Robotics

- 6.1.3 Machine Vision Systems

- 6.1.4 Cloud, Analytics and Platforms

- 6.1.5 Cybersecurity

- 6.1.6 Sensors & Transmitters

- 6.1.7 Connectivity/Communication

- 6.1.8 Other Field, Control and Safety Solutions

- 6.1.1 Industrial Control Systems

- 6.2 End-user Industry

- 6.2.1 Automotive

- 6.2.2 Semiconductor

- 6.2.3 Oil and Gas

- 6.2.4 Chemical and Petrochemical

- 6.2.5 Pharmaceutical

- 6.2.6 Aerospace and Defense

- 6.2.7 Food and Beverages

- 6.2.8 Other End-user Industries

- 6.3 Country

- 6.3.1 China

- 6.3.2 India

- 6.3.3 Japan

- 6.3.4 South Korea

- 6.3.5 Rest of Asia-Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd

- 7.1.2 Honeywell International Inc.

- 7.1.3 Fanuc Corporation

- 7.1.4 Mitsubishi Electric Corporation

- 7.1.5 Emerson Electric Company

- 7.1.6 Rockwell Automation Inc.

- 7.1.7 Schneider Electric SE

- 7.1.8 Robert Bosch GmbH

- 7.1.9 Siemens AG

- 7.1.10 Yokogawa Electric Corporation

- 7.1.11 Cisco Systems Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET