PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937347

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937347

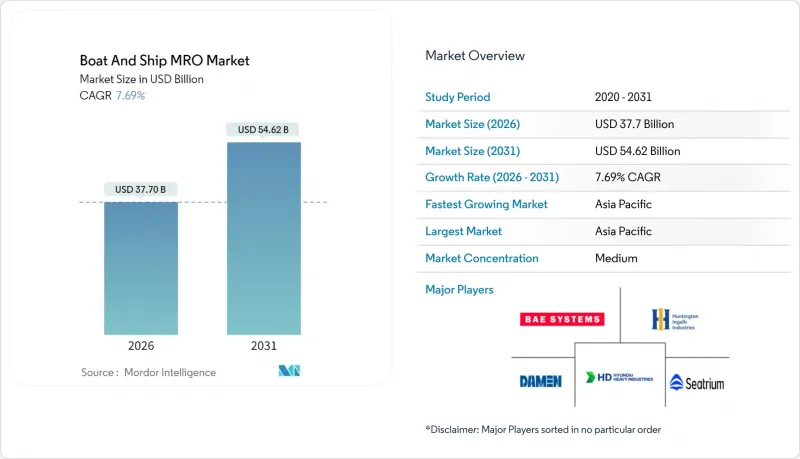

Boat And Ship MRO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Boat & Ship MRO market is expected to grow from USD 35.01 billion in 2025 to USD 37.7 billion in 2026 and is forecast to reach USD 54.62 billion by 2031 at 7.69% CAGR over 2026-2031.

This expansion stems from the dual necessity of maintaining an aging global fleet and complying with stricter environmental mandates that pull previously optional retrofit work inside standard maintenance cycles . Greater commercial-trade volumes, predictive maintenance adoption, and defense fleet modernization collectively reinforce the Boat & Ship MRO market growth outlook. Independent yards leverage cost agility, while OEM-affiliated facilities introduce digital diagnostics and alternative-fuel expertise that reshape competitive positioning. Regional demand skews toward Asia-Pacific, driven by China's capacity expansion and Japan's technology upgrades, yet North American and European operators pursue high-value retrofit projects to meet greenhouse-gas rules, sustaining a balanced global opportunity landscape.

Global Boat And Ship MRO Market Trends and Insights

Stricter IMO Environmental Mandates

The Marine Environment Protection Committee's 20% emission-cut target for 2030 triggers retrofit demand worldwide [1]. The Energy Efficiency Existing Ship Index obliges engine tweaks, hull re-engineering, and alternative-fuel integrations. In parallel, FuelEU Maritime penalties of EUR 2,400 (USD 2,640) per ton of excess CO2 create economic urgency that funnels capital into propulsion conversions capable of running on ammonia or hydrogen .

Aging Global Vessel Fleet

The average merchant fleet age of 22.1 years increases routine MRO frequency and cost. Container ships older than 20 years incur higher maintenance spend per deadweight ton and face detention rates 3.2 times those of younger vessels, pushing operators toward preventative work that safeguards schedules and insurance rates. Bulk carriers and tankers are particularly exposed because hull integrity and propulsion reliability directly affect safety margins and charter viability.

High Capital Intensity and Dock-Capacity Scarcity

Global dry-dock utilization reached a significant share in 2024, stretching maintenance schedules by 3.2 weeks and inflating project costs. Building a mid-sized dock and ultra-large floating docks places high demands, limiting near-term capacity relief. The Sembcorp Marine-Keppel consolidation reveals how scale economies counter rising capex burdens .

Other drivers and restraints analyzed in the detailed report include:

- Growth in Commercial Marine Trade

- Naval Fleet Modernization Budget

- Marine-Fuel Price Volatility Limiting Budgets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commercial ships held 62.64% of the Boat & Ship MRO market in 2025, reflecting high utilization and regulatory obligations that require full-cycle maintenance every 18-24 months. Ballast-water systems, scrubber retrofits, and fuel conversions place continual demand on dock capacity. Offshore support vessels, ferries, and research craft contribute an 7.98% CAGR niche, enabled by renewable-energy build-outs and deep-sea mining exploration. Boat-class craft benefit from tourism rebound yet rely mostly on fiberglass-hull and outboard-engine service.

Upgraded IACS inspection codes for vessels older than 15 years elevate structural-assessment frequency, especially for bulkers and tankers. Superyacht refits ranging from USD 5-50 million remain a specialized but lucrative subset as owners seek luxury interiors and decarbonized propulsion.

Commercial services captured 61.58% of the Boat & Ship MRO market share in 2025 due to trade growth, whereas defense work grew at 9.21% through 2031, supported by cybersecurity, sensor, and weapon-system upgrades with secure-facility requirements. Private-vessel demand follows seasonal luxury-yacht refits in Mediterranean and Caribbean yards.

The USD 3.2 billion Columbia-class submarine infrastructure investment demonstrates scaled in-house maintenance protocols for nuclear propulsion. IoT analytics allow commercial operators to reduce downtime up to 30%, integrating maintenance within voyage planning.

The Boat & Ship MRO Market Report is Segmented by Vessel Type (Boat, Yacht, Commercial Vessels, and Other Types), Vessel Application (Private, Commercial, and Defense), MRO Type (Engine MRO, Component MRO, and More), Service Provider Type (Independent Yards, OEM-Affiliated MROs, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated with a 39.05% of the Boat & Ship MRO market share in 2025 and an 8.44% CAGR outlook toward 2031. China delivered a major share of global new-build tonnage in 2024 and funnels the same yard base toward MRO, reinforced by partnerships that import European analytics platforms. Japan's LNG and naval specialization leverages predictive systems from Mitsubishi Heavy Industries to trim operating costs, while South Korean groups such as Hanwha Ocean deploy modular construction to shorten dock time.

Europe remains a premium-service hub, hosting Italy's and Spain's super-yacht refit clusters. Tighter emissions rules and FuelEU Maritime enforcement accelerate retrofit spend. Germany's engineering houses craft technical standards that ripple through worldwide retrofit protocols, and Turkey's Istanbul-Antalya corridor attracts mid-priced commercial and yacht projects.

North America banks on naval modernization and Jones Act protections. The U.S. Navy maintenance allotment sustains coastal yard networks, while Canada's Arctic shipping lanes generate ice-class repair demand. Labor tightness fuels automation investments such as General Dynamics NASSCO's augmented-reality inspection suites. The rest of world shows divergent trends: Middle Eastern free-zone yards compete on tax advantages, South America targets coastal tourism craft supported by green-retrofit grants, and Africa's emerging offshore-energy support craft catalyze local dry-dock development.

- Huntington Ingalls Industries Inc.

- Zamakona Yards

- Abu Dhabi Shipbuilding Co.

- Bender CCP, Inc.

- Mitsubishi Heavy Industries Ltd.

- Bath Iron Works (General Dynamics)

- Rhoads Industries Inc.

- BAE Systems plc

- Damen Shipyards Group

- Hyundai Heavy Industries Co.

- General Dynamics NASSCO

- Seatrium Limited

- ST Engineering

- Fincantieri S.p.A.

- Rolls-Royce Power Systems

- Caterpillar Inc. (Cat Marine)

- Wartsila Corporation

- ABB Group (ABB Marine & Ports)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter IMO Environmental Mandates

- 4.2.2 Aging Global Vessel Fleet

- 4.2.3 Growth in Commercial Marine Trade

- 4.2.4 Naval Fleet Modernization Budget

- 4.2.5 Predictive-Maintenance Adoption by Mid-Sized Yards

- 4.2.6 Green-Retrofit Subsidies for Coastal Tourism Craft

- 4.3 Market Restraints

- 4.3.1 High Capital Intensity and Dock-Capacity Scarcity

- 4.3.2 Marine-Fuel Price Volatility Limiting Budgets

- 4.3.3 Skilled Labor Gap in Composite-Hull Repair

- 4.3.4 Cyber-Security Compliance Cost for Connected Vessels

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Vessel Type

- 5.1.1 Boat

- 5.1.2 Yacht

- 5.1.3 Commercial Vessels

- 5.1.4 Other Types

- 5.2 By Vessel Application

- 5.2.1 Private

- 5.2.2 Commercial

- 5.2.3 Defense

- 5.3 By MRO Type

- 5.3.1 Engine MRO

- 5.3.2 Component MRO

- 5.3.3 Dry-dock / Hull

- 5.3.4 Modifications and Retrofits

- 5.3.5 Other Types

- 5.4 By Service Provider Type

- 5.4.1 Independent Yards

- 5.4.2 OEM-Affiliated MROs

- 5.4.3 In-house Operator Facilities

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Huntington Ingalls Industries Inc.

- 6.4.2 Zamakona Yards

- 6.4.3 Abu Dhabi Shipbuilding Co.

- 6.4.4 Bender CCP, Inc.

- 6.4.5 Mitsubishi Heavy Industries Ltd.

- 6.4.6 Bath Iron Works (General Dynamics)

- 6.4.7 Rhoads Industries Inc.

- 6.4.8 BAE Systems plc

- 6.4.9 Damen Shipyards Group

- 6.4.10 Hyundai Heavy Industries Co.

- 6.4.11 General Dynamics NASSCO

- 6.4.12 Seatrium Limited

- 6.4.13 ST Engineering

- 6.4.14 Fincantieri S.p.A.

- 6.4.15 Rolls-Royce Power Systems

- 6.4.16 Caterpillar Inc. (Cat Marine)

- 6.4.17 Wartsila Corporation

- 6.4.18 ABB Group (ABB Marine & Ports)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment