PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1686607

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1686607

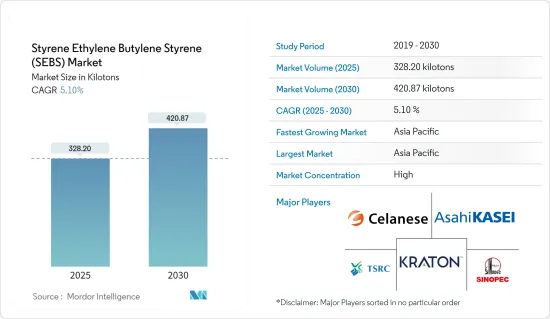

Styrene Ethylene Butylene Styrene (SEBS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Styrene Ethylene Butylene Styrene Market size is estimated at 328.20 kilotons in 2025, and is expected to reach 420.87 kilotons by 2030, at a CAGR of 5.1% during the forecast period (2025-2030).

The COVID-19 pandemic hampered the styrene ethylene butylene styrene (SEBS) market as nationwide lockdowns in several countries and strict social distancing measures affected applications such as adhesives and sealants, automotive, and plastics. However, the market registered a significant growth rate well after the restrictions were lifted due to the increasing demand for ethylene butylene styrene from adhesives and sealants, automotive, and plastics industries.

Key Highlights

- The increasing investments in the adhesives industry and the growing demand from the automotive industry are expected to drive the market for styrene ethylene butylene styrene.

- On the flip side, the hazardous nature and regulations of styrene are expected to hinder the growth of the market.

- The emergence as a replacement for PVC across various applications is expected to create opportunities for the market during the forecast period.

- Asia-Pacific is expected to dominate the market. It is also expected to register the highest CAGR during the forecast period. This is due to the rising demand for styrene ethylene butylene styrene from adhesives and sealants, automotive, and plastics industries.

Styrene Ethylene Butylene Styrene (SEBS) Market Trends

The Automotive Industry is Expected to Dominate the Market

- Styrene-ethylene-butylene-styrene (SEBS), owing to its high strength, excellent UV and heat stability, and other physical properties, is used in automotive weather seals, window encapsulation, glass run channels, static seals, automotive interior trim, and instrument panel preparation.

- Global automobile manufacturing is expected to surpass 100 million units in the near future due to increasing population levels and rising affluence in emerging markets. According to the Organization Internationale des Constructeurs d'Automobiles (OICA), in 2023, around 93.55 million vehicles were produced worldwide, witnessing a growth rate of 10% compared to 85.02 million vehicles in 2022. This indicated an increased demand for SEBS from the automotive industry. In 2023, around 68 million passenger cars were manufactured worldwide, up by nearly 11% compared to 2022.

- The growth in the automotive industry can also be seen due to the rising demand for electric vehicles. In terms of EV volume, the total number of electric vehicle sales is expected to reach 31 million in 2027 and 74.5 million by 2035. Therefore, the demand for SEBS is expected to grow in the coming years.

- China's passenger electric vehicle (EV) market continues to grow at an impressive rate. EV sales rose by 87% Y-o-Y in 2022. BYD, Wuling, Chery, Changan, and GAC are some of the top Chinese brands that dominate the EV market, with local brands commanding 81%. Additionally, in 2022, BYD increased its market share by over 11% Y-o-Y, with six out of the top 10 EV models in the Chinese market coming from the brand.

- The Chinese government estimates a 20% penetration rate of electric vehicle production by 2025. This is anticipated to increase the production and consumption of vehicle batteries, thus increasing SEBS demand in the market.

- According to the China Association of Automobile Manufacturers (CAAM), China has the largest automotive production base in the world, with a total vehicle production of 30.16 million units in 2023, registering an increase of 11.7% compared to 27 million units produced last year.

- Owing to all these factors, the market for styrene-ethylene-butylene-styrene (SEBS) is likely to grow globally during the forecast period.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific dominated the global SEBS market. With growing construction activities in countries like India, China, Japan, and South Korea, the demand for adhesives, sealants, and electrical products has been increasing in the region, further leading to an increase in the consumption of SEBS.

- The Chinese adhesives and sealants market is estimated to witness healthy growth over the coming years in end-user segments such as packaging, automotive, construction, and electronic industries. Some of the major players and potential customers for SEBS in the country are 3M, HB Fuller Company, Henkel AG & Co. KGaA, Arkema Group, Sika AG, Huitian New Materials, Wanwei High-tech, and others.

- According to statistics from the China Adhesive and Adhesive Tape Industry Association, adhesive production in the country increased year on year from 2021 to 2022, reaching a total of 7.88 million metric tons in 2022. The production of adhesives is expected to reach 8.55 million metric tons in 2025, which is expected to increase the demand for SEBS.

- India is the second-largest footwear manufacturer in the world, accounting for 9% of the annual global production of 22 billion pairs. Nearly 90% of the manufactured footwear is utilized in the country, and the rest is exported. The consumption of footwear stood at around 2.1 billion pairs, and it ranks third after China and the United States.

- India has the potential to become a world leader in the footwear and leather industry. The leather industry is expected to grow due to the country's free trade agreement (FTA) with the United Arab Emirates. Exports increased by 64% in November 2022, according to the Union Minister for Trade Industries, Consumer Affairs, Food, and Public Distribution and Textiles.

- According to the Japan Electronics and Information Technology Industries (JEITA), the production value of industrial electronic devices stood at JPY 293,577 million (USD 2,080.85 million) in December 2023, increasing by almost 100% annually. Furthermore, the production value of consumer electronic equipment in the country stood at JPY 35,775 million (USD 253.57 million) in December 2023, increasing by around 112.2% during the same period the previous year.

- Due to all such factors, the market for styrene-ethylene-butylene-styrene (SEBS) in the region is expected to show steady growth during the forecast period.

Styrene Ethylene Butylene Styrene Industry Overview

The styrene-ethylene-butylene-styrene (SEBS) market is consolidated in nature, with top players contributing to the major share of the market. Some of the major players in the market include (not in any particular order) Kraton Corporation, China Petrochemical Corporation (Sinopec Corp.), Celanese Corporation, TSRC, and Asahi Kasei Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Investments in the Adhesives Industry

- 4.1.2 Growing Demand From the Automotive Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Hazardous Nature and Regulations of Styrene

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Form

- 5.1.1 Pellets

- 5.1.2 Powder

- 5.2 End-User Industry

- 5.2.1 Footwear

- 5.2.2 Adhesives and Sealants

- 5.2.3 Plastics

- 5.2.4 Roads and Railways

- 5.2.5 Automotive

- 5.2.6 Sporting and Toys

- 5.2.7 Electrical and Electronics

- 5.2.8 Other-end User Industries (Medical, 3D Printing, Lubricant Tackifiers, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Asahi Kasei Corporation

- 6.4.2 Celanese Corporation

- 6.4.3 China Petrochemical & Chemical Corporation (Sinopec Corp.)

- 6.4.4 Dynasol Group

- 6.4.5 General Industrial Polymers

- 6.4.6 ENEOS Corporation

- 6.4.7 Kraton Corporation

- 6.4.8 Kuraray Co. Ltd

- 6.4.9 LCY GROUP

- 6.4.10 Ningbo Changhong Polymer Scientific and Technical Inc.

- 6.4.11 Ravago

- 6.4.12 RTP Company

- 6.4.13 Trinseo

- 6.4.14 TSRC

- 6.4.15 Versalis SpA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emergence as a Replacement For PVC Across Various Applications