PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1685818

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1685818

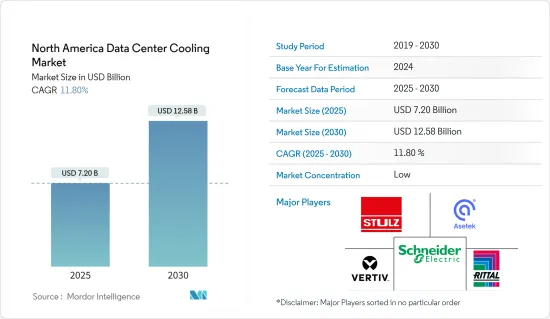

North America Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The North America Data Center Cooling Market size is estimated at USD 7.20 billion in 2025, and is expected to reach USD 12.58 billion by 2030, at a CAGR of 11.8% during the forecast period (2025-2030).

The rapid development of various containerized, modular, and performance-optimized data center (POD) facilities is anticipated to boost the overall demand for various cooling systems that can be utilized in the data centers, driving the market's growth extensively.

The United States dominated the total North American data center cooling market mainly due to the growth in the development of colocation and hyperscale facilities with over 100 MW power capacity. A surge in the need for cost-effective and efficient data centers, healthy growth of enterprises with data centers, various green initiatives for eco-friendly data center solutions, and power density are expected to drive the market's growth.

In addition, the emergence of portable cooling and liquid-based cooling technologies and growth in the need for a modular data center cooling approach are expected to offer lucrative opportunities for the North American data center cooling market. The solution segment had ruled the North American data center cooling market primarily due to the rising adoption of energy-efficient, cost-effective, and environment-friendly cooling solutions in line with various stringent environmental safety rules offered by governmental bodies.

Moreover, the market witnessed significant product launches and innovations, driving the market significantly. For instance, in June 2023, a 5MW, state-of-the-art testing laboratory was commissioned at the Modine Rockbridge facility in Virginia, further expanding the services that Airedale by Modine can provide data center customers and meet growing demand from the data center industry for validated, sustainable cooling solutions. The new lab can test a complete range of air conditioning equipment, accommodating air-cooled chillers up to 2.1MW and water-cooled chillers up to 5MW.

However, the need for specialized infrastructure, higher investment costs, and various cooling challenges during a power outage are expected to restrict the growth of the North American data center cooling market throughout the forecast period.

The COVID-19 pandemic placed data centers in unchartered territory. There were many supply chain disruptions, and due to lockdowns globally, the smooth operations of the systems were hugely impacted. Owing to shipping disruptions and factory closures that affected the delivery of data center equipment, operators found workarounds to meet the challenges. However, during the post-COVID-19 period, the market is expected to witness various lucrative growth opportunities throughout the forecast period.

North America Data Center Cooling Market Trends

Growth in the Construction Sector Boosting the Demand for Furniture Products

- The information technology (IT) industry primarily consists of the overall sales of information technology (IT) services and related goods by various entities such as sole traders, organizations, and partnerships that mainly apply computers, computer peripherals, and telecommunications equipment to retrieve, store, transmit and maneuver data. The IT market also involves computer networking, systems design services, broadcasting, information distribution technologies like telephones and television, and several other equipment used during the process. These huge requirements require a proper cooling system for the devices to perform normally, thereby driving the overall demand for the data center cooling market.

- The IT industry needs on-premise private data storage as well as hyperscale data centers for its various operations according to the organization's size. The rise in the adoption of cloud storage has drastically increased over the years within the region, especially due to growth in SaaS providers, allowing cloud storage providers to extend their capacities, which is anticipated to maximize the demand for data center cooling systems.

- The cooling system is essential in the IT and data center sector, primarily due to the need for various enhanced high-quality cooling solutions that are quite efficient than the traditional air-cooling solution. Also, the rise in technological innovation in the IT infrastructure, coupled with the increase in the demand for cooling systems among the various smartphone manufacturers for thermal management, is also driving the market growth extensively.

- The United States plays a very significant role in terms of establishing various driving the market's growth rate, which is mainly due to the rising investments and establishments of the data center by the key major market players within the region. For instance, in January 2023, Amazon Web Services intends to invest a sum of around USD 35 billion by 2040 to establish various multiple data center campuses across Virginia.

Asia-Pacific is Expected to Hold Significant Market Share

- The United States is poised to dominate the market in North America, owing to the presence of many services and software providers as well as high investments by colocation providers and hyper-scale data center operators. In the last few years, there has been a significant rise in the number of data centers. A considerable number of processors are being utilized in a given space to increase data centers' performance, which results in increased density. The requirement for power and cooling has grown along with increased density.

- The United States also contributes substantially to the global data center requirements from the banking, IT, financial services, and insurance (BFSI), retail, and healthcare industries. Data center service providers in the region are prompted to manage their operating costs, as the region is a lucrative market, considering the number of data centers and their expansions.

- Data centers' power density experiences growth by an average of 1.5 kW per rack, which results in limited air distribution and enhanced heat generation. In general, IT equipment typically needs between 100 and 160 cfm of air per kW, but in a dense environment, it diminishes to less than 100, which results in higher heat generation, driving the market's growth significantly.

- The expansion of mobile broadband, the emergence of 5G, growth in Big Data analytics, and cloud computing are the primary factors driving the demand for new data center infrastructures in the United States. Network providers are working to ensure the rapid implementation of 5G for better innovation. Such developments are further driving the demand for efficient data center cooling solutions and services among United States's enterprises.

- As per Cloudscene, as of September 2023, the total count of data centers in the United States was 5,375, whereas Germany ranked second with an overall count of 522 data centers. The United Kingdom ranked 3rd among countries in terms of the total number of data centers, with 517, while China recorded 448. This possession of a significant number of data centers in the United States is expected to amplify the market's growth throughout the forecast period.

North America Data Center Cooling Industry Overview

The North American data center cooling market is highly competitive and fragmented. Market penetration is growing with a strong presence of major players, such as Schneider Electric SE, Black Box Corporation, Asetek, Nortek Air Solutions LLC, Emerson Electric Co., Hitachi Ltd, Rittal GmbH & Co. KG, Fujitsu Ltd, Stulz GmbH, and Vertiv, in established markets. With the increasing focus on innovation, the demand for new technologies, such as liquid-based cooling and portable cooling technologies, is also growing, which, in turn, is driving investments for further developments in the region.

In May 2024, Stulz unveiled its latest innovation, the CyberCool Coolant Management and Distribution Unit (CDU), specifically engineered to optimize heat exchange efficiency in liquid cooling solutions. The product line comprises four models, available in two distinct sizes. These units boast an impressive heat exchange capacity, ranging from 345 kW to 1,380 kW. Stulz has set the rated water supply temperature for the facility water system at 32°C (89.6°F), with the liquid supply temperature for the technology cooling system pegged at 36°C (96.8°F).

In March 2024, Rittal Private Limited marked the opening of its new Integration Center, specifically tailored for Cooling Units and Liquid Cooling Package (LCP) solutions, at its Bangalore, India manufacturing plant. This strategic move not only bolsters the company's production capabilities but also positions it to cater to the escalating demand for Industrial Cooling Solutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview (Coverage: A detailed analysis of the current regional trends related to Data Center Cooling are included in this section)

- 4.2 Key cost considerations for Cooling

- 4.2.1 Analysis of the key cost overheads related to DC operations with an eye on DC Cooling

- 4.2.2 Key innovations and developments in Data Center Cooling

- 4.2.3 Key energy efficiency practices adopted in Data Centers

5 MARKET DYNAMICS

- 5.1 Market Drivers (Key factors such as the increased emphasis on energy consumption, move towards green solutions are mapped based on their relative impact over the next 5-7 years)

- 5.2 Market Challenges (Key factors such as the dynamic nature of regulations, evolving customer needs are mapped based on their relative impact over the next 5-7 years)

- 5.3 Market Opportunities

- 5.4 Comparison of raised floor with containment & raised floor without commitment

- 5.5 Industry Ecosystem Analysis

6 ANALYSIS OF THE CURRENT REGIONAL DATA CENTER FOOTPRINT

- 6.1 Regional Analysis of IT Load Capacity & Area Footprint of Data Centers (for the period of 2017-2030)

- 6.2 Regional Analysis of the Established DC Markets and Emerging DC Hotspots in North America region (we will include coverage by highlighting major established and emerging DC markets)

- 6.3 Regional Analysis of Regulatory Framework On DC Cooling

7 DATA CENTER COOLING MARKET SEGMENTATION

- 7.1 By Cooling Technology (Key trends, market size estimates & projections for the period of 2022-2029 and future outlook)

- 7.1.1 Air-based Cooling

- 7.1.1.1 CRAH

- 7.1.1.2 Chiller and Economizer

- 7.1.1.3 Cooling Tower (covers direct, indirect & two-stage cooling)

- 7.1.1.4 Others

- 7.1.2 Liquid-based Cooling

- 7.1.2.1 Immersion Cooling

- 7.1.2.2 Direct-to-Chip Cooling

- 7.1.2.3 Rear-Door Heat Exchanger

- 7.1.1 Air-based Cooling

- 7.2 By End-user Vertical

- 7.2.1 IT & Telecom

- 7.2.2 Retail & Consumer Goods

- 7.2.3 Healthcare

- 7.2.4 Media & Entertainment

- 7.2.5 Federal & Institutional agencies

- 7.2.6 Other end-users

- 7.3 By Country

- 7.3.1 United States

- 7.3.2 Canada

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Vertiv Group Corp.

- 8.1.2 Stulz GmbH

- 8.1.3 Schneider Electric SE

- 8.1.4 Rittal GmbH & Co. KG

- 8.1.5 Asetek A/S

- 8.1.6 Alfa Laval AB

- 8.1.7 Iceotope Technologies Limited

- 8.1.8 Green Revolution Cooling Inc.

- 8.1.9 Chilldyne Inc.

- 8.1.10 Airedale International Air Conditioning Ltd.

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS