PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1404336

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1404336

Dynamic Random Access Memory (DRAM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

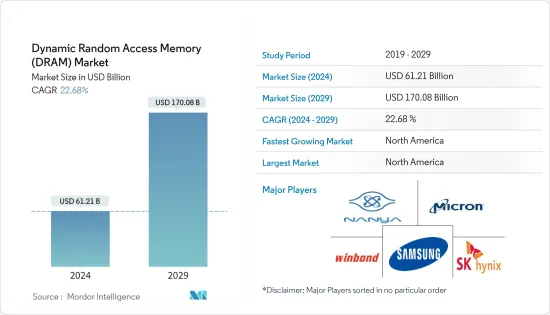

The Dynamic Random Access Memory Market size is estimated at USD 61.21 billion in 2024, and is expected to reach USD 170.08 billion by 2029, growing at a CAGR of 22.68% during the forecast period (2024-2029).

Semiconductor memory, commonly referred to as dynamic random access memory (DRAM), is utilized to store and process data or program code necessary for a computer processor's functioning. This type of RAM is commonly found in personal computers, smartphones, ADAS systems, smartwatches, workstations, and servers.

Key Highlights

- The growing adoption of generative AI boosts the demand for fast processing and highly efficient DRAM solutions. For instance, Micron Technology partnered with Qualcomm Technologies Inc. to accelerate generative AI at the edge for smartphones. The company shipped production samples of the low-power double data rate 5X (LPDDR5X) memory to Qualcomm in October 2023. The LPDDR5X memory operates at a world-leading 9.6 Gbps speed grade, delivering the speed and performance the mobile ecosystem needs to unleash the power of AI at the edge.

- Micron LPDDR5X provides advanced power-saving capabilities for mobile users using its innovative, 1β process node technology. Also, in September 2023, SK Hynix announced and presented a prototype of their AI accelerator card, AiMX1, based on the high-speed, low-power, and high-density memory solution GDDR6-AiM at the AI hardware & edge AI Summit 2023 in California. AiMX1 is expected to significantly contribute to developing high-performance, data-intensive, and AI-based systems.

- Datacenter demand for DRAM is projected to grow significantly, which will lift overall DRAM demand annually. Artificial intelligence and other cutting-edge technologies like streaming, gaming, and autonomous vehicles will continue to drive robust demand for data centers. This will drive innovation in data center architecture and technology as operators strive to provide the capacity that supports the increased power density required by high-performance computing. Integrating artificial intelligence, the Internet of Things, and 5G will be a massive tailwind to the demand for computing and DRAM.

- Worldwide smartphone shipments declined significantly in FY 2023 compared to FY 2022 due to decreased consumer spending, economic downturn, and increased inflation. The leading smartphone vendors such as Samsung, Apple, Xiaomi, and Oppo (including One Plus) witnessed a decline in the sales of smartphones. Following smartphones, tablets, and PCs/laptops, demand declined in FY 2023 due to weakened consumer spending, interest rates, and increasing uncertainty due to ongoing geopolitical tensions. These factors will restrict the growth of the DRAM market.

- The COVID-19 pandemic had a significant impact on the DRAM market, both on the demand side and the supply side. Lockdowns and factory shutdowns worldwide contributed to the supply shortage, but many of these impacts are expected to be temporary. Governments worldwide are taking steps to support the semiconductor industries, which could lead to a recovery.

Dynamic Random Access Memory (DRAM) Market Trends

Datacenter Application Segment is Expected to Hold Significant Market Share

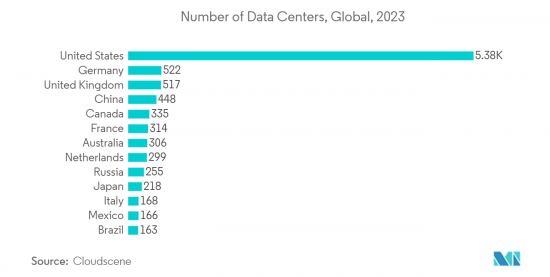

- The COVID-19 pandemic accelerated the use of digital platforms and cloud services, boosting data center development. As DRAM is an essential component for the proper functioning of modern enterprise and data center applications, the growth in data centers has significantly fueled the demand for the market. According to Cloudscene, as of September 2023, there are over 9380 data centers worldwide.

- Since 2022, DRAM suppliers have been working towards adjusting their product mixes to assign more wafer input to server DRAM products while minimizing the wafer input for mobile DRAM products. Two reasons have driven this trend. Firstly, the demand outlook is bright for the server DRAM segment. The latest server platforms from AMD and Intel finally shipped to OEMs in 2022 but are expected to need ~six months for qualifying, facilitating a headwind to near-term server shipments and associated memory demand. Simultaneously, DRAM suppliers are building up significant inventory positions as production surge has continued to outpace demand.

- On the second position, the reason lies that the mobile DRAM segment has faced significant oversupply during 2022, and moving into 2023, the projections on the development of smartphone shipments and the surge in the average DRAM content of smartphones remain pretty conservative. Resultantly, DRAM suppliers intend to keep expanding the share of server DRAM in their product mixes, thus providing significant growth in the data center segment.

- Semiconductor manufacturers are likely to respond to changes in demand by producing more dynamic RAM (DRAM) for servers than for mobile devices this year, a milestone highlighting increasing enterprise use of emerging technology related to cloud computing, AI, and high-performance computing (HPC) applications. To handle the emerging-tech workloads, servers' average DRAM content is expected to increase significantly.

- Moreover, in the data center segment t, buyer inventory of DDR5 has been gaining popularity. For instance, Micron Technology unveiled its DDR5 chip, which it stated found the most demand from data center applications before popping up in client devices. Furthermore, Renesas has been leading the data center market due to new chipsets for High-Performance Memory Modules Based on DDR5 Multiplexer Combined Ranks (MCR) Dual In-line Memory modules. Meanwhile, Samsung's intensified production cutbacks have notably shrunk DDR4 wafer inputs, causing a supply crunch in server DDR4 stocks. This scenario leaves no leeway for further server DDR4 price reductions.

United States is Expected to Hold Significant Market Share

- In the United States, the growth of DRAM is projected to extend beyond personal devices and find increased utilization in cloud computing, servers, and automotive applications. Smartphones are increasingly incorporating DRAM, and mobile phones are anticipated to hold a significant portion of the DRAM market due to their expanding market penetration and declining prices, resulting in greater consumer acceptance. As the range of use cases and mobile phone adoption continues to diversify and expand, the demand for the DRAM market is expected to rise.

- The adoption of AI, high-performance computing, and cloud technology by businesses has resulted in a significant increase in the demand for memory chips in servers. In fact, servers now contain more DRAM than all mobile devices combined. As data continues to grow at an exponential rate, the ability to extract insights from it is crucial for business success. Due to the advancements and investments in advanced data centers, the DRAM market in the region is expected to experience growth. The United States is currently the largest region for connectivity and cloud technology, with a total of 5,375 data centers, according to Clodscene.

- Data center operators are required to optimize platform performance by leveraging advanced memory capabilities and processor advancements, thereby fueling the demand for DDR5 DRAMs in the market. The United States is consistently experiencing substantial investments in data centers, which is anticipated to stimulate the requirement for DRAMs. Notably, in April 2022, Google disclosed its plan to invest USD 9.5 billion in US data centers and offices, primarily concentrating on the southern and western regions of the country. In the past five years, the organization has allocated over USD 37 billion toward enhancing its offices and data centers across 26 states. The anticipated outcome of these expansion investments is to stimulate the market.

- In July 2022, Micron made an announcement regarding the availability of their DDR5 server DRAM for commercial and industrial channel partners. This move is aimed at supporting the industry qualification of next-generation Intel and AMD DDR5 server and workstation platforms. The new server DDR5 memory from Micron is designed to enhance performance for AI, HPC, and data-intensive applications that require higher memory bandwidth and CPU computing capacity. The introductory data rate for DDR5 is 4800MT/s, but it is expected to increase in order to meet the future demands of data centers.

- Another significant factor influencing the market is the implementation of 5G technology in the area. Despite its recent introduction, 5G technology and wireless communication as a whole are projected to have a substantial effect on the market. As per Accenture's analysis, the adoption of 5G is anticipated to contribute more than USD 1.5 trillion to the gross domestic product (GDP) of the United States (US) between 2021 and 2025. Furthermore, according to VIAVISION, the United States has the highest number of cities with 5G availability. These factors are expected to boost the market's growth.

Dynamic Random Access Memory (DRAM) Industry Overview

The Dynamic Random Access Memory (DRAM) Market is moderately consolidated, with the major players in the market, like Samsung Electronics, SK Hynix, and Micron, holding a market share of more than 80% in FY 2022. Geographical expansion and product innovation play a vital role in the competitive strategy of market players. In line with the increasing data center, mobile, and consumer applications that require improved speed and performance, vendors need enhanced fabrication and processing capabilities.

The prominent vendors in the DRAM market are investing heavily in the next generation of chips, like 24GB, DDR5, and HBM, and have moved into the next phase of making FRAMs for AI and 5G. This is helping them stay ahead of the competition, but it also means they need to be able to pay for their research and development.

- September 2023 - Samsung Electronics recently unveiled the pioneering Low Power Compression Attached Memory Module (LPCAMM) form factor, marking a significant breakthrough in the DRAM market for personal computers, laptops, and potentially data centers. This cutting-edge development, boasting a remarkable speed of 7.5 gigabits-per-second (Gbps), has successfully undergone rigorous system verification on Intel's platform.

- June 2023 - Micron Technology Inc. has revealed its intention to construct a new assembly and test facility in Gujarat, India. The facility will cater to the manufacturing of DRAM and NAND products and will cater to both domestic and international markets. The construction of the new facility is expected to commence in 2023 and will be carried out in phases. The first phase will include 500,000 square feet of cleanroom space and is expected to become operational in late 2024.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of Macroeconomic Factors on the Dram Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Continuous Evolution of Mega Trends such as Cloud Computing, IoT, 5G, AI, and Mobility are Expected to Create Demand in the Future

- 5.2 Market Restraints

- 5.2.1 Slowdown in the Mobile Device, Tablet, Laptop/PC Demand

6 PRICING ANALYSIS

- 6.1 DRAM Spot Price (Per GB)

- 6.2 Pricing Trends Analysis

7 MARKET SEGMENTATION

- 7.1 By Architecture

- 7.1.1 DDR3

- 7.1.2 DDR4

- 7.1.3 DDR5

- 7.1.4 DDR2/Others Architectures

- 7.2 By Application

- 7.2.1 Smartphones/Tablets

- 7.2.2 PC/Laptop

- 7.2.3 Datacenter

- 7.2.4 Graphics

- 7.2.5 Consumer Products

- 7.2.6 Automotive

- 7.2.7 Other Applications

- 7.3 By Geography

- 7.3.1 United States

- 7.3.2 Europe

- 7.3.3 Korea

- 7.3.4 China

- 7.3.5 Taiwan

- 7.3.6 Rest of Asia-Pacific

- 7.3.7 Rest of the World

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Samsung Electronics Co. Ltd.

- 8.1.2 Micron Technology Inc.

- 8.1.3 SK Hynix Inc.

- 8.1.4 Nanya Technology Corporation

- 8.1.5 Winbond Electronics Corporation

- 8.1.6 Powerchip Semiconductor Manufacturing Corp.

- 8.1.7 Transcend Information Inc.

9 VENDOR MARKET SHARE ANALYSIS

10 INVESTMENT ANALYSIS

11 FUTURE OF THE MARKET