Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1404365

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1404365

Oilfield Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

PUBLISHED:

PAGES: 125 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

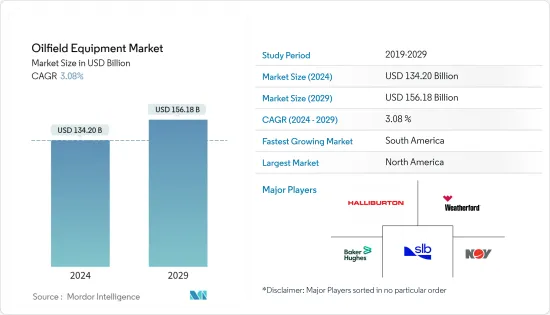

The Oilfield Equipment Market size is estimated at USD 134.20 billion in 2024, and is expected to reach USD 156.18 billion by 2029, growing at a CAGR of 3.08% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, factors such as the increasing number of deep-water and ultra-deepwater fields and the growing drilling operations in regions (like South America, North America, the Middle East, and Africa) will likely drive the oilfield equipment market during the forecast period.

- On the other hand, the volatile oil prices due to the supply-demand gap and geopolitics are major factors restraining the market's growth.

- Nevertheless, the increasing oil and gas discoveries and the global liberalization in the industry created new opportunities for the players to invest in.

Oilfield Equipment Market Trends

Onshore Segment to Dominate the Market

- Onshore drilling encompasses all the drilling sites located on dry land and accounts for 70% of worldwide oil production. Onshore drilling is similar to offshore drilling but without the difficulty of deep water between the platform and oil.

- The global crude oil prices showed signs of recovery and are improving quickly, and the onshore projects are easier to kick start than offshore ones. Therefore, riding on the optimism associated with the recovery of crude oil prices, onshore projects are expected to record significant growth over the forecast period, driving the demand for the oilfield equipment market.

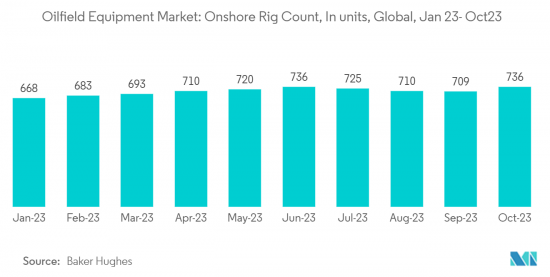

- According to Baker Hughes, as of October 2023, the total onshore rig counts accounted for 736 units, approximately 75% of the total rig counts. With the increasing rig counts on the land region, drilling, production, and other oil field activity are expected to be in demand. It, in turn, will drive the oilfield equipment market for the onshore region.

- According to Schlumberger (SLB), a provider of oilfield services, the company would increase its quarterly dividend in 2023 by 43% (to 25 cents per share) and resume its share buyback program in reaction to the strong energy markets. In 2021, the company recorded total revenue of USD 586 million, out of which the onshore segment recorded revenue of USD 439 million, representing 75% of the total revenues. The offshore segment reported USD 147 million, representing 25% of the total revenue.

- Moreover, oil Production increased by 1.6% in 2021 worldwide. In 2021, the oil production was 89877 thousand barrels per day compared to 2020, which was 88494 thousand barrels per day.

- Hence, the onshore segment is expected to dominate the oilfield equipment market worldwide.

North America is expected to Dominate the Market

- North America is expected to dominate the oilfield equipment market in 2023. It is expected to continue its dominance during the forecast period.

- The share of North America in global crude oil production increased from 17.3% in 2013 to around 22.7% in 2021, which resulted in an increased demand for oilfield equipment in the region.

- Further, Canada's oil and gas industry is expected to attract rising investment interests in the future due to an aggressive push by Newfoundland and Labrador as prices plummet in oil-rich Alberta.

- In May 2022, the Canadian Association of Energy Contractors raised its drilling prediction for oil and natural gas after a good first quarter due to higher-than-expected oil and gas prices. The revised drilling projection predicts 62,121 working days for the year, up from the earlier forecast of 58,111, and 170 active rigs, up from 159.

- Furthermore, due to higher oil prices and declining drilling costs, the offshore rig count and offshore oil production in the United States increased significantly, indicating that growth is not only offshore drilling but also production activity. It, in turn, is expected to be the major driver for the oilfield equipment market in the country.

- Therefore, factors such as rising oil and gas activities are expected to grow the oilfield equipment market in the forecast period.

Oilfield Equipment Industry Overview

The oilfield equipment market is consolidated, with some of the top companies holding the major share of the market. Some companies include (in no particular order) Schlumberger Limited, Baker Hughes Company, Halliburton Company, Weatherford International PLC, and National Oilwell Varco Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 61086

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Onshore and Offshore Active Rig Count and Forecast, till 2028

- 4.4 Crude Oil and Natural Gas Production and Forecast, till 2028

- 4.5 Historic and Demand Forecast of CAPEX in USD billion, by Onshore and Offshore, till 2028

- 4.6 Major Upcoming Upstream Projects

- 4.7 Recent Trends and Developments

- 4.8 Market Dynamics

- 4.8.1 Drivers

- 4.8.1.1 The Increasing Number of Deep-Water and Ultra-Deepwater Fields

- 4.8.1.2 The Growing Drilling Operations in Regions (like South America, North America, and Middle-East and Africa)

- 4.8.2 Restraints

- 4.8.2.1 The Volatile Oil Prices, Owing to the Supply-Demand Gap and Geopolitics

- 4.8.1 Drivers

- 4.9 Supply Chain Analysis

- 4.10 Porter's Five Forces Analysis

- 4.10.1 Bargaining Power of Suppliers

- 4.10.2 Bargaining Power of Consumers

- 4.10.3 Threat of New Entrants

- 4.10.4 Threat of Substitutes Products and Services

- 4.10.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 Equipment Type

- 5.2.1 Drilling Equipment

- 5.2.2 Production Equipment

- 5.2.3 Other Equipment Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States of America

- 5.3.1.2 Canada

- 5.3.1.3 Rest of the North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of the Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 South Korea

- 5.3.3.4 Rest of the Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of the South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Iran

- 5.3.5.4 Rest of the Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Schlumberger Limited

- 6.3.2 Weatherford International PLC

- 6.3.3 Baker Hughes Company

- 6.3.4 Halliburton Company

- 6.3.5 Tenaris SA

- 6.3.6 TMK Ipsco Enterprises Inc.

- 6.3.7 National Oilwell Varco Inc.

- 6.3.8 Vallourec SA

- 6.3.9 Aker Solutions ASA

- 6.3.10 Stabil Drill

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Increasing Oil and Gas Discoveries, Coupled With the Liberalization in the Industry

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.