PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1404447

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1404447

Air Data Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

The air data systems market is valued at USD 872.42 million in 2024 and is anticipated to grow to USD 1.09 billion by 2029, registering a CAGR of 5.86% during the forecast period.

Air data systems provide vital information for aircraft flight control, such as accurate measurements over a wide range of attack and airspeed angles. Increasing demand for new aircraft by airlines and armed forces across the globe is the major driving factor for the air data systems market. The R&D investments in developing advanced air data systems may further propel the growth of the market in the coming years. Technological advancements in cloud computing, artificial intelligence, and real-time data monitoring are a few additional factors boosting the growth of the market. Air data system manufacturers continually update their products to suit their customers' needs with the latest technologies. However, developing systems for managing multiple data types, formats, and structures with even better efficiency continues to remain a challenge for manufacturers.

Air Data Systems Market Trends

Commercial Segment Holds Highest Shares in the Market

The commercial segment held the highest shares in the market and continued its domination during the forecast period. The growth is attributed to the increasing air traffic, rising demand for new aircraft, and growing expenditure on the aviation sector. According to the International Air Transport Association (IATA), the overall air passenger number will reach 4 billion in 2024. Furthermore, as per the Boeing Company's Commercial Market Outlook 2023-2042, there will be a demand for more than 42,000 new commercial aircraft, both passenger and cargo aircraft, during the next two decades.

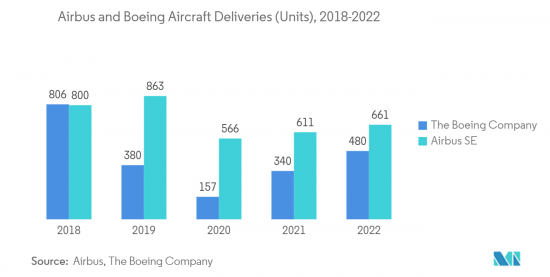

The commercial aviation sector witnessed substantial growth in 2022, driven by a rapid rise in air passenger traffic, which resulted in both Airbus and Boeing Company, two of the largest aircraft OEMs, recording significant increases in orders from airlines operating across the globe. In 2022, Airbus delivered a total of 661 commercial aircraft to 84 customers and registered 1,078 gross new orders. The Boeing Company delivered a total of 480 commercial airplanes. The recertification of the Boeing B737 MAX models caused a resurgence in the demand for the Boeing B737 MAX family of aircraft. On this note, in 2022, the Boeing Company received a total of 561 orders for Boeing B737 MAXs. During the same timeframe, the Boeing Company also received orders for 213 widebodies and 78 freighters, including 50 orders for the B777-8 freighters. Thus, growing deliveries of commercial aircraft and the increasing number of new aircraft orders are driving the growth of the market.

Asia-Pacific to Experience the Highest Growth during the Forecast Period

The Asia-Pacific region is expected to experience a high growth rate during the forecast period. The primary driver for the growth of the market is the increasing procurement of commercial aircraft from countries like China, India, Indonesia, Vietnam, and Thailand. The increasing air traffic in the region forced the commercial airlines to expand their fleet by procuring new-generation aircraft. For instance, in November 2022, seven leasing companies signed a contract with the Commercial Aircraft Corporation of China (COMAC) for the procurement of 300 new C919 planes and 30 ARJ21 aircraft. Similarly, in February 2023, Air India announced its plans to procure 470 new aircraft from Airbus and the Boeing Company as part of its fleet expansion plans. The airline announced procuring 210 Airbus A320neo, 40 Airbus A350s, 190 Boeing B737 MAXs, 20 Boeing B787s, and 10 Boeing B777X. On the other hand, the countries in the region are also procuring new military aircraft. China is investing heavily in the development and deployment of advanced fighter aircraft while also expanding its operational capabilities with respect to AEW&C and bomber aircraft. Japan is buying substantial numbers of F-35A fighters to replace its aging F-4 fleet, while South Korea is focused on adding both indigenous (KF-X) and foreign-made aircraft (F-35A) to its fleet. Thus, the growing procurement of new aircraft is creating a demand for air data systems, thereby propelling the growth of the market.

Air Data Systems Industry Overview

The air data systems market is consolidated in nature due to the presence of a few players holding significant shares in the market. Some of the prominent players in the market are Honeywell International Inc., RTX Corporation, Curtiss-Wright Corporation, AMETEK, Inc., and Meggitt PLC. These players together account for a major share of the air data systems market. Companies are investing significantly in the research and development of air data systems and are launching new products to increase their market share. Collins Aerospace, an RTX Corporation company, launched the latest generation of SmartProbe Air Data Systems. It integrates sensing probes, pressure sensors, and powerful air data computer processing to provide all critical air data parameters, including pitot and static pressure, air, speed, altitude, angle of attack, and angle of sideslip.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Commercial

- 5.1.2 Military

- 5.2 Component

- 5.2.1 Electronic Units

- 5.2.2 Probes

- 5.2.3 Sensors

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Qatar

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Honeywell International Inc.

- 6.2.2 THOMMEN AIRCRAFT EQUIPMENT Ltd.

- 6.2.3 Collins Aerospace (RTX Corporation)

- 6.2.4 Curtiss-Wright Corporation

- 6.2.5 AMETEK.Inc

- 6.2.6 Astronautics Corporation of America

- 6.2.7 Shadin L.P.

- 6.2.8 Meggitt PLC

- 6.2.9 Aeroprobe Corporation

- 6.2.10 THALES

7 MARKET OPPORTUNITIES AND FUTURE TRENDS