PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644327

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644327

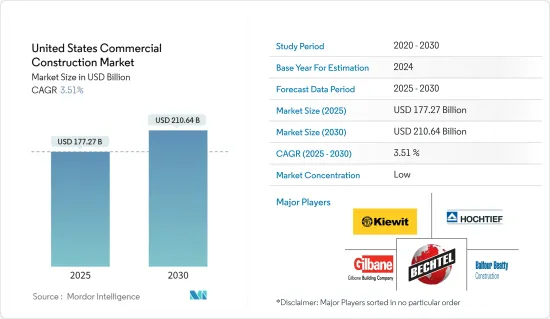

United States Commercial Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The United States Commercial Construction Market size is estimated at USD 177.27 billion in 2025, and is expected to reach USD 210.64 billion by 2030, at a CAGR of 3.51% during the forecast period (2025-2030).

Despite inflation and labor shortage, the demand for commercial real estate continues to drive the market. Furthermore, the market is driven by the huge investments pouring into infrastructure building in the country.

Key Highlights

- Overall, the commercial construction industry had a good year in 2021. Construction spending increased due to high spending in residential construction; however, the non-residential segment fell for the second year in a row. Construction firms also had to deal with ongoing labor shortages and delays in receiving building materials due to supply issues and rising material prices. Through November 2021, construction spending totaled USD 1.46 trillion, setting the year to another record-high for construction put-in-place.

- Infrastructure spending will be one of the top areas for growth in construction in 2022. With the USD 1.2 trillion Infrastructure Investment and Jobs Act, Congress finally passed a long-term infrastructure bill after years of stopgap measures and short-term spending bills. Over the next five years, the federal government will invest USD 550 billion in new infrastructure construction and repairs to existing infrastructure. The bill proposes investing USD 110 billion in roads, bridges, and infrastructure projects, USD 40 billion in bridge repairs and replacement, USD 39 billion in public transportation, USD 66 billion in passenger and freight rail, USD 65 billion in broadband internet, USD 65 billion in electric grid reconstruction, and USD 55 billion in water infrastructure.

- During the pandemic, the non-residential building market did not see a similarly dramatic increase in construction services. To be sure, some industries experienced rapid growth, such as warehouses and data centers, but these were offset by more pervasive laggards, such as office buildings and hotels. Construction, like so many other industries, was harmed by brittle supply chains and a shrinking labor force. Building material prices skyrocketed, with lumber, for example, rising as much as 264% from pre-pandemic levels at one point. Furthermore, product lead times continued to skyrocket, with three and four times the pre-pandemic rates not uncommon. To combat rising prices, the Federal Reserve has raised the federal funds rate aggressively, with four hikes in 2022 to date.

- According to the resources, inflation and lead times for certain building materials are finally easing. Construction spending in six sectors-manufacturing, highways, transportation, multifamily housing, lodging, and communications-is expected to increase by at least 5% in 2023, according to the firm. Other sectors, including healthcare, public safety, education, and commerce, are expected to grow by 0-4%. Lead times for other materials, such as architectural interiors, lumber, and plumbing, have also decreased. In the case of plumbing pipes, raw material availability has improved, production has increased, and residential construction demand has decreased.

US Commercial Construction Market Trends

The Emergence of Smart Cities is a Key Market Trend

New York City is currently ranked as the second smartest city in the world and is one of the most prominent Smart Cities. The main innovation of the city can be identified by the form of the transportation and communication linkages. In Smart Cities, the management of operations involves the integration of data and communication, as well as the utilization of the most up-to-date technologies. The development of Smart Cities leads to the creation of functional areas, such as Transportation, Traffic Management, Energy Efficiency and Sustainability, and Governance. The increasing number of Smart City projects across the United States will necessitate the construction of sophisticated road network systems, thus creating growth opportunities for vendors in the market.

For instance, in October 2022, Honeywell's Accelerator Program for Smart City Strategic Planning announced that it is partnering with Acceleration for America to help cities plan for their future and build the capacity to fund transformative initiatives. In-kind support will be provided through Honeywell's Smart Cities Accelerator Program, which is a partnership between Honeywell and Acceleration for America. The Acceleration for America program is designed to accelerate progress in cities' strategic planning efforts. The Honeywell Smart Cities Acceleration Program is a partnership between Acceleration for America (AFA) and Honeywell (Honeywell), which is a subsidiary of Honeywell Inc. (Honeywell). Five U.S cities have joined the Acceleration for America: Cleveland (Cleveland, OH); Louisville, KY; Kansas City, MO; San Diego, CA; Waterloo, and Iowa.

Each city will receive Smart City Strategic Plans (SCPs) through Honeywell's and Accelerator's technical support. Each SCP aligns key stakeholders, sets priorities, and identifies high-impact, inclusive initiatives that improve residents' quality of life (QoE) in areas like climate resilience, public safety and operational efficiency, and enhanced service delivery. Each city will also be supported in applying for Federal grants to help implement identified projects.

Office and Retail Space Driving the Market

In March 2022, 144.7 million square feet of office space were under construction in the United States, accounting for 2.2% of total stock. Notably, half of that pipeline will be provided in urban submarkets outside of key business areas. Furthermore, 93% of the space is Class A or A+, indicating that businesses are continuing to prioritize high-quality projects to retain their workforce.

In March 2022, Austin, Texas, had 10 million square feet of office space under construction. This represented 11.5% of the city's current stock, while planned projects represented 25.3%, the highest percentage among major cities. This comes after Austin outperformed all other markets in 2021 in terms of office-using job growth (14%), as well as new development (5.3 million square feet). In contrast, construction in Denver and Phoenix slowed due to the pandemic and massive pre-pandemic deliveries; between 2015 and 2021, each city added more than 16 million square feet of additional supply. In March, both cities had slightly more than 1 million square feet of office space under construction, accounting for slightly more than 0.8% of total stock.

US Commercial Construction Industry Overview

The US Commercial Construction Market is fragmented and highly competitive, with the major local and international players creating a highly competitive environment in this sector. However, the market opens opportunities for small and medium players due to increasing govt investments in the sector. Major players in the market include Gilbane Building Company, MA Mortenson Company, Balfour Beatty LLC, Hensel Phelps Construction Co., McCarthy Holdings Inc., and Tutor Perini Corporation. The market presents opportunities for growth during the forecast period, which is expected to drive market competition further. Large players competing with others for a significant increase in market share leaves the industry with no observable levels of consolidation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Initiatives

- 4.2.2 Demand for office and retail space

- 4.3 Market Restraints

- 4.3.1 Lack of Skilled Labor

- 4.3.2 Supply chain issues and rising material costs

- 4.4 Market Opportunities

- 4.4.1 Greater Use of New Technologies

- 4.5 Insights into Supply Chain/Value Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Overview of the Commercial Construction Market in the United States

- 4.8 Brief on Construction Costs (average cost, office and retail space, per sq feet)

- 4.9 Insights into the newly office space completions (sq. feet)

- 4.10 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By End User

- 5.1.1 Office Building Construction

- 5.1.2 Retail Construction

- 5.1.3 Hospitality Construction

- 5.1.4 Institutional Construction

- 5.1.5 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Kiewit Corporation

- 6.2.2 Hochteif Construction

- 6.2.3 Bechtel Corporation

- 6.2.4 Gilbane Building Company

- 6.2.5 MA Mortenson Company

- 6.2.6 Balfour Beatty LLC

- 6.2.7 Hensel Phelps Construction Co.

- 6.2.8 McCarthy Holdings Inc.

- 6.2.9 EMCOR

- 6.2.10 Fluor Corporation

- 6.2.11 Skanska USA Building Inc.*

7 *List Not Exhaustive

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

- 9.1 Insights into the Wage Statistics

- 9.2 Insights into the Number of Businesses

- 9.3 Insights into Financial Benchmarks and Commercial Construction

- 9.4 Insights into the Labor Statistics

- 9.5 Macroeconomic Indicators (GDP Distribution by Activity, Contribution of Commercial Construction to economy)

- 9.6 Insights into the Industrial Benchmarks, Commercial Construction

- 9.7 Insights into Capital Flows (Investments in the Commercial Construction Sector)