Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692480

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692480

Recycled Carbon Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 160 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

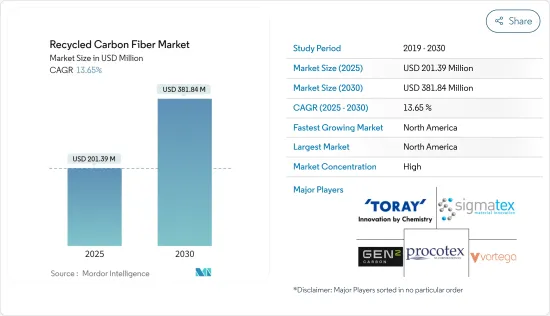

The Recycled Carbon Fiber Market size is estimated at USD 201.39 million in 2025, and is expected to reach USD 381.84 million by 2030, at a CAGR of 13.65% during the forecast period (2025-2030).

Key Highlights

- The market was negatively impacted by COVID-19 in 2020 due to disruption in the supply chain. As the pandemic spread, many manufacturing plants involved in the recycling of carbon fiber globally were shut down due to the strict lockdowns. However, the sector has been recovering since restrictions were lifted owing to increased demand from various end-user industries, such as wind energy.

- Over the short term, the rising demand for lightweight vehicles, growing carbon fiber scrap recycling, its increasing reuse in the wind energy sector, and the cost-effectiveness of recycled carbon fiber are some of the factors driving the market demand.

- The availability of various substitutes and supply chain security for recycled carbon fiber are the factors hindering the market's growth.

- Shifting focus toward sustainability, advancement in research and development for recycling techniques, and increasing potential demand from additive manufacturing and 3D printing sectors are likely to create opportunities for the market in the coming years.

- The North American region is expected to dominate the market and is likely to witness the highest CAGR during the forecast period.

Recycled Carbon Fiber Market Trends

Increasing Usage in the Aerospace and Defense Industry

- Recycled carbon fiber possesses similar properties to new carbon fiber used for manufacturing composites that are used in the aerospace and defense industry. These carbon fibers offer specific advantages to components used for the aerospace and defense industry, such as durability in harsh conditions and at high temperatures, abrasion resistance, and corrosion resistance.

- Recycled carbon fiber has replaced aluminum in aircraft to improve fuel economy. Lightweight materials and structures allow military aircraft to carry more fuel and payload while in commercial aircraft.

- Lightweight materials are used to reduce greenhouse gas emissions and the amount of waste sent to landfills. For instance, the Boeing 787 was made 20% lighter, which helped in increasing the fuel economy by nearly 10% to 12%.

- Moreover, the preference for recycled carbon fiber is also increasing in the aerospace industry to manage the significant problem of aircraft waste. It is estimated that, in the global aerospace industry, about 6000-8000 aircraft will reach the end of their service life by 2030, which may create a potential source for carbon recycling in the industry.

- Airbus has set a target of recycling 95% of its carbon fiber waste by 2020-2025, with 5% recycled back into the aerospace sector. The gross orders of aircraft for airbus were 771 units in 2021, as compared to 383 units in 2020.

- The growing passenger volumes and increasing retirements of aircraft are expected to drive the need for 44,040 new jets (valued at USD 6.8 trillion) over the next two decades. The global commercial fleet is expected to reach 50,660 aircraft by 2038, considering all the new aircraft and jets that may remain in service.

- According to the International Air Transport Association (IATA), the global revenue for commercial airlines was valued at USD 373 billion in 2020 and was estimated at USD 472 billion in 2021, registering a growth rate of 26.7% Y-o-Y. Furthermore, the revenue was expected to reach USD 658 billion by the end of 2022.

- According to Boeing, by 2040, the worldwide commercial fleet will exceed 49,000 planes, with China, Europe, North America, and the Asia-Pacific countries each accounting for around 20% of new plane deliveries and the remaining 20% going to other rising markets.

- Owing to all these factors, the market for recycled carbon fiber is likely to grow globally during the forecast period.

The North American Region to Dominate the Market

- The North American region is expected to dominate the market. In the region, the United States is the largest economy in terms of GDP. The United States and Canada are among the fastest emerging economies in the world.

- The fast-growing automotive and aerospace industries are driving the growth of the market studied in the North American region. Strategic developments, the presence of established car manufacturers, leading recycled carbon fiber manufacturers, and technological advancements related to recycled carbon fiber products all contribute to the market's growth in this region.

- The United States is the region's leader in the consumption of recycled carbon fiber, which is used by major corporations. Due to the growing demand for lightweight materials to reduce vehicle weight, the use of recycled carbon fiber in the automotive and aerospace end-use industries has increased in the region.

- Moreover, in the United States, according to the Federal Aviation Administration (FAA), the number of aircraft in the country's commercial fleet accounted for 5,882 in 2020, witnessing a decline rate of 22.9% compared to the previous year. However, the commercial fleet is projected to increase to 8,756 in 2041, with an average annual growth rate of 2% per year. This is expected to increase the demand for carbon fiber from multiple applications in the aerospace industry.

- In Canada, the country has a Centre de developpement des composites du Quebec (Composite Development Centre of Quebec) (CDCQ) engaged in various activities related to the value chain of various composite materials, including carbon fibers. The center is also actively involved in the recycling of carbon fiber as one of its major activities.

- Globally, Canada ranks first in civil flight simulation, third in civil engine production, and fourth in civil aircraft production. It is the only nationally ranked in the top five of all the key categories. The Canadian aerospace industry exports over 70% of its products to over 190 countries across six continents.

- Wind energy in Canada accounts for 3.5% of electricity generation, being the region's second most important renewable energy source. Wind energy plays a crucial role in reaching global net-zero carbon emissions. Canada is one of the world leaders in producing and using renewable power due to its diversified geography with hydro, biomass, wind, and solar energy sources.

- Due to all such factors, the market for recycled carbon fiber in the region is expected to have steady growth during the forecast period.

Recycled Carbon Fiber Industry Overview

The recycled carbon fiber market is partially consolidated in nature. Some of the major players in the market include Toray Industries Inc., Procotex, Vartega Inc., Gen 2 Carbon Limited, and Sigmatex, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 91476

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand For Lightweight Vehicles

- 4.1.2 Growing Carbon Fiber Scrap Recycling and its Reuse in the Wind Energy Sector

- 4.1.3 Cost Effectiveness of Recycled Carbon Fiber

- 4.2 Restraints

- 4.2.1 Availability of Various Substitutes

- 4.2.2 Supply Chain Security for Recycled Carbon Fiber

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Revenue)

- 5.1 Type

- 5.1.1 Chopped Recycled Carbon Fiber

- 5.1.2 Milled Recycled Carbon Fiber

- 5.2 Source

- 5.2.1 Automotive Scrap

- 5.2.2 Aerospace Scrap

- 5.2.3 Other Sources

- 5.3 End-user Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace and Defense

- 5.3.3 Wind Energy

- 5.3.4 Sporting Goods

- 5.3.5 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Alpha Recyclage Composites

- 6.4.2 Carbon Conversions

- 6.4.3 Carbon Fiber Recycling

- 6.4.4 Carbon Fiber Remanufacturing

- 6.4.5 Gen 2 Carbon Limited

- 6.4.6 Karborek RCF

- 6.4.7 Mitsubishi Chemical Holdings Corporation.

- 6.4.8 Procotex

- 6.4.9 Shocker Composites LLC

- 6.4.10 Sigmatex

- 6.4.11 Toray Industries Inc.

- 6.4.12 Vartega Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Shifting Focus Toward Sustainability

- 7.2 Advancement in Research and Development for Recycling Techniques

- 7.3 Increasing Potential Demand from Additive Manufacturing and 3D Printing Sectors

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.