PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408214

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408214

North America Geopolymer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

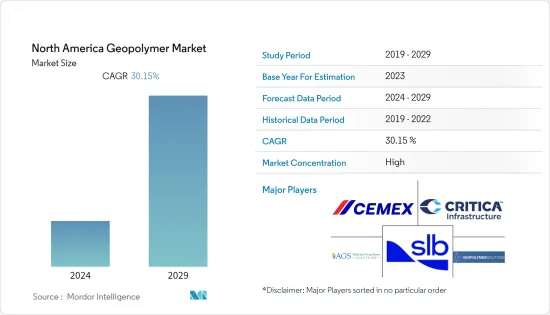

The North America geopolymer market is estimated to reach USD 1.95 billion by the end of this year. It is projected to reach USD 7.30 billion in the next five years, registering a CAGR of 30.15% during the forecast period.

COVID-19 negatively impacted the market. Since there were no construction activities during the pandemic and the manufacturing factories were shut down. Currently, the market recovered from the pandemic and is growing at a significant rate.

Key Highlights

- Over the short term, increasing construction activities, environmental regulations, and emission strain on the cement industry are major factors driving the studied market's growth.

- However, the geopolymer's complex manufacturing process limits the studied market's growth.

- Nevertheless, technological developments and innovations in the construction sector will likely create lucrative growth opportunities for the North American market.

- The United States is likely to remain the largest market in the region over the forecast period owing to the expected increase in demand from various construction activities in the country.

North America Geopolymer Market Trends

Building Segment to Dominate the Market

- Geopolymers are used extensively in the construction of buildings. Due to overcrowding and rapidly rising construction activity, considerable amounts of greenhouse gases are released into the atmosphere, severely impacting the ecosystem. The rising environmental impact of greenhouse gases created either during cement production or in other alternative ways drives the geopolymer demand. It made it possible to create and use geopolymers in the construction of buildings.

- In 2022, the United States residential building sector slowed due to rising mortgage rates, inflation, supply chain issues, and labor shortages. On the other side, there is a rise in non-residential construction.

- According to the AIA (American Institute of Architects) Construction Consensus Forecast Panel, non-residential building construction spending expanded by 5.4% in 2022. Further, expenditure on new private non-residential buildings peaked in the United States at over USD 539 billion in 2022. In 2023, all the major commercial, industrial, and institutional categories are projected to witness at least reasonably healthy gains.

- In Canada, there was a decline of 11.6% in 2022 in residential construction, and the value is expected to decrease by a further 6.2% in 2023. The residential sector declined 2.1%, while the non-residential sector was up 0.8% in December 2022.

- In Canada, budget 2022 proposes to advance USD 2.9 billion in funding under the NHCF (National Housing Co-Investment Fund) to accelerate the creation of up to 4,300 new units and repair up to 17,800 units.

- In addition, the Government of Canada's National Housing Strategy (NHS) is an ambitious 10-year plan to invest more than USD 82 billion to give more Canadians a place to call home.

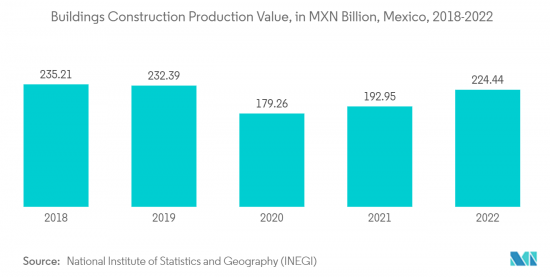

- Further, according to the National Institute of Statistics and Geography (INEGI), the value of building construction projects in Mexico amounted to MXN 224 billion (~USD 11.16 billion) in 2022, the highest value among other construction segments.

- Therefore, various government projects are supporting the sector's growth, which will likely create the demand for geopolymers for building, pipe & concrete repair, and other applications over the forecast period.

United States to Dominate the Market

- The United States is expected to dominate the geopolymer market during the forecast period due to the rising construction and mining activities.

- According to the United States Census Bureau, the value of private construction in 2022 stood at USD 1,434.2 billion, 11.7% higher than USD 1,279.5 billion in 2021. Residential construction spending in 2022 was USD 899.1 billion, up 13.3% from USD 793.7 billion in 2021, while non-residential construction spending accounted for USD 530.1 billion, down 9.1% from USD 485.8 billion in 2021 (1.0%).

- According to the AIA (American Institute of Architects) Construction Consensus Forecast Panel, non-residential building construction spending expanded by 5.4% in 2022. Further, expenditure on new private non-residential buildings peaked in the United States at over USD 539 billion in 2022. By 2023, all the major commercial, industrial, and institutional categories are projected to witness at least reasonably healthy gains.

- One of the major commercial projects is the construction of West Henderson Hospital in South Carolina, which is expected to be completed in Q2 2024. This project involves constructing a 28.91 thousand sq m 128-bed hospital construction, which started in Q1 2022. Similarly, in the same area, the construction of the BMW Group supplier EV plant started in December 2022.

- In addition, the United States is planning to bring an overhaul to the country's existing infrastructure. In May 2022, the government announced the allocation of over USD 110 billion for 4,300 specific projects for modernizing airports and ports, rebuilding roads and bridges, and replacing lead pipes to deliver clean water. These projects are expected to benefit around 3,200 communities across the 50 states and create lucrative demand for geopolymers over the forecast period.

- To bolster the supply chains and ensure the safety of its people, the United States, in August 2022, locked more than USD 2.2 billion from the Rebuilding American Infrastructure with Sustainability and Equity (RAISE) program for upgrading bridges, roads, ports, rail, transit, and intermodal transportation.

- Furthermore, carbon footprint reduction of paving materials could be achieved by recycling mining by-products into different applications, preserving natural resources, and decreasing environmental issues. One possible approach is to reuse mining ore waste and quarry dust as precursors in geopolymer applications.

- Alternatively, some quarry wastes are rich in aluminosilicates and include the proper mineralogy, allowing their application as precursors to produce geopolymer cement.

- According to the United States Geological Survey, the capacity utilization of the United States' mining industry stood at an estimated 87% in 2022.

- Therefore, the rising residential, commercial, and infrastructural construction sectors and mining activities are anticipated to increase the demand for geopolymers through the forecast period.

North America Geopolymer Industry Overview

The North American geopolymer market is consolidated in nature. The major players (not in any particular order) include CEMEX, SAB de CV, SLB (Schlumberger Limited), Critica Infrastructure, Alchemy Geopolymer Solutions, and Geopolymer Solutions LLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Construction Activities in the Region

- 4.1.2 Environmental Regulations and Emission Strain on Cement Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Complex Manufacturing Process

- 4.2.2 Other Restraints

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Cement, Concrete, and Precast Panel

- 5.1.2 Grout and Binder

- 5.1.3 Other Product Types (Composites, Foam, and Bricks)

- 5.2 Application

- 5.2.1 Building

- 5.2.2 Road and Pavement

- 5.2.3 Runway

- 5.2.4 Pipe and Concrete Repair

- 5.2.5 Bridge

- 5.2.6 Tunnel Lining

- 5.2.7 Railroad Sleeper

- 5.2.8 Coating

- 5.2.9 Fireproofing

- 5.2.10 Nuclear and Other Toxic Waste Immobilization

- 5.2.11 Specific Mold Products

- 5.3 Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Alchemy Geopolymer Solutions

- 6.4.2 CEMEX, S.A.B. de C.V.

- 6.4.3 Critica Infrastructure

- 6.4.4 Geopolymer Solutions LLC

- 6.4.5 Milliken & Company Inc.

- 6.4.6 PURIS Corp

- 6.4.7 RENCA Inc

- 6.4.8 SLB (Schlumberger Limited)

- 6.4.9 Standard Cement Materials, Inc.

- 6.4.10 URETEK USA

- 6.4.11 Vortex Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Developments and Innovations in the Construction Sector

- 7.2 Other Opportunities