PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693912

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693912

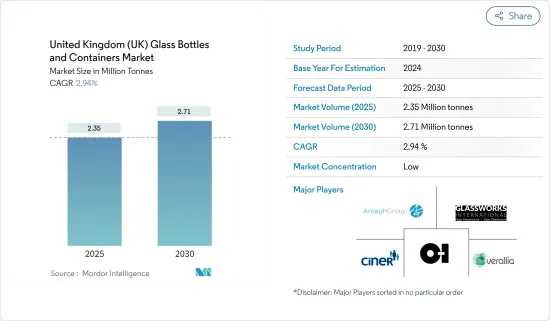

United Kingdom (UK) Glass Bottles and Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The United Kingdom Glass Bottles and Containers Market size is estimated at 2.35 million tonnes in 2025, and is expected to reach 2.71 million tonnes by 2030, at a CAGR of 2.94% during the forecast period (2025-2030).

Plastic packaging technologies have come a long way in recent years. Still, glass continues to dominate upscale alcoholic and non-alcoholic beverage packaging. Glass is among the most preferred packaging materials for alcoholic beverages, such as spirits. The ability of glass bottles to preserve the aroma and flavor of the product is driving the demand.

Key Highlights

- Increasing customer needs for safe and healthier packaging supports glass packaging growth in different categories. Also, innovative technologies for embossing, shaping, and adding artistic finishes to glass make glass packaging more desirable among end users. Furthermore, factors such as the demand for eco-friendly products and the rising need from the food and beverage market are boosting the market's growth.

- Besides, consumers increasingly prefer beer and wine, and glass packaging manufacturers have adjusted their production. Premium food and beverage brands prefer glass (container glass) over other packaging options, such as plastic, as glass is chemically inert, non-porous, and impermeable.

- The growing adoption of alternative forms of packaging, such as plastic and metal, is among the prominent factors affecting the market's growth over the forecast period. In addition, the increase in recycled plastic (rPET) bottles encouraged by the government also leads to challenging conditions for the adoption of glass packaging.

- According to Argus Media, in May 2022, many companies and brands in the UK's fast-moving consumer goods (FMCG) sector aim to increase recycled content in plastic packaging. The British Plastics Federation (BPF) estimates the current average level of recycled content in the United Kingdom PET bottle market is 15%-20%.

- According to Glass Alliance Europe, production with 39.5 million tonnes were produced two years back. This indicates that the glass manufacturers suffered from energy concerns on top of high competition from third countries. Compared with 2021, 2022 extra EU-27 exports decreased by 4.6% in volume at 4.3 million tonnes but increased by 14.9%. The EU-27's four significant clients in volume are the rest of Europe (59.5%), including the UK (20%), and more countries.

- The growing adoption of alternative forms of packaging, such as paper, plastic, and metal, in different parts of the country is among the prominent factors affecting the market's growth over the forecast period. The advancement in plastic manufacturing technologies and the emergence of highly recyclable plastics, such as bio-plastics, are further expected to drive the growth of plastic packaging, as plastic packaging offers a significant cost advantage compared to glass packaging.

United Kingdom (UK) Glass Bottles and Containers Market Trends

Beverages to be the Largest End-user Industry

- Glass is among the most preferred packaging materials for alcoholic beverages, such as spirits. The ability of glass bottles to preserve the aroma and flavor of the product is driving the demand. Rising consumer demand for safe and healthier packaging helps glass packaging grow in different categories. Also, innovative technologies for embossing, shaping, and adding artistic finishes to glass make glass packaging more desirable among end-users.

- Glass bottles and containers are mainly used in alcohol and nonalcoholic beverages because of their chemical sterility and non-permeability. Also, glass is a significant barrier material and ranks highly for transparency in packaging. It creates an extended shelf-life package because it resists CO2 loss and O2 invasion. The glass bottle frangibility has been improved by new processing and coatings. Modern lightweight and strengthening techniques have improved the strength and consumer-friendliness of glass.

- Furthermore, wine sales and consumption have grown manifolds during the pandemic, and while most of the wines sold are packaged in the standard 750-milliliter format, alternatives such as small format bottles are on the rise. The increase in the consumption of liquor in the region during the pandemic has positively impacted the demand for glass bottles.

- According to the Observatory of Economic Complexity (OEC), in April 2023, United Kingdom exports of Glass Bottles totaled GBP 15.8 million (USD 19.48 million), while imports totaled GBP 40.7 million (USD 50.18 million), resulting in an overall trade deficit of GBP 24.9 million (USD 30.70 million). From April 2022 to April 2023, the United Kingdom's export of Glass Bottles decreased by GBP 931,000 (USD 1,147,965), or 5.57%, from GBP 16.7 million (USD 20.59 million) to GBP 15.8 million (USD 19.48 million), while its imports rose by GBP 10,000,000 (USD 12,330,456.2), or 33.9%, from GBP 30.4 million (USD 37.48 million) to GBP 40.07 million (USD 49.40 million).

- The demand from the alcoholic and nonalcoholic beverage industry primarily drives the increase in the import of glass bottles in the country. This upswing is expected to be witnessed in the forecast period also.

Flint to Hold Major Market Share in Colors

- The utilization of transparent packaging is on the rise for food items such as wine, milk, beer, and juice. This decision is driven by the marketing suggestion that customers prefer to inspect the product before purchase.

- In the United Kingdom, the challenge in producing recycled glass is not in its difficulty but rather the insufficient supply of high-quality recycled clear glass (cullet) necessary for making clear glass bottles with high recycled content. Green glass is the only option if a product requires a glass bottle with a high recycled content. While dark glass is a viable alternative, it may not be suitable for certain products and brands, particularly in the food and beverages industry, where a crystal-clear glass of the highest quality, known as flint or extra-flint, is preferred.

- Frequently, the process of segregating mixed-colored glass at a recycling plant is excessively time-consuming and costly. Consequently, the shattered fragments of mixed glass are repurposed to manufacture glass fiber products, which can serve as an insulation material rather than being transformed into fresh bottles. Multi-stream recycling is the most effective method for producing high-quality glass cullet, which is free from other recyclables.

- The purity of the stream is crucially important, particularly with regard to the color of the glass being processed. Green glass can use up to 95% recycled glass, but there are much stricter quality requirements for white or flint glass. In this case, the maximum level of recycled glass permitted is only 60% due to the risk of contamination and its detrimental effect on the final product's quality.

- In the wine industry, the usual bottle colors are green or amber. However, there has been a recent push for lighter and thinner glass bottles due to environmental concerns and commercial demands. This shift towards lighter bottles aims to reduce energy consumption, transportation costs, and recycling expenses. Furthermore, the use of flint glass bottles responds to the need to highlight the color of rose or white wines and improve the overall aesthetics of the packaging. Furthermore, the increasing consumption of beer in the United Kingdom is also expected to boost the growth of the market.

United Kingdom (UK) Glass Bottles and Containers Market Overview

The United Kingdom Glass Bottles and Containers Market is fragmented with various significant players such as Verallia UK Limited (Verallia Packaging SAS), Ciner Glass Ltd., O-I Glass, Inc., Ardagh Group, and more. Companies operating in the industry are focused on expanding their business through collaborations, investments, product innovations, and more.

- May 2023 - Ardagh Glass Packaging (AGP) - United Kingdom announced the building of a highly sustainable, efficient furnace that is set to minimize greenhouse gas emissions from the glass production process.

- February 2023 - Ciner Glass signed a land transfer agreement for 240,000 m2 at Kristalpark III. With this agreement, Ciner Glass finalized the purchase process that started in 2021 and acquired the full right to use the land previously owned by LRM. This will enable the glass bottle manufacturer to constitute the next step in the further development of building a state-of-the-art facility in Lommel. In addition to its historical connection and heritage with the glass industry, Lommel was chosen for its strategic location. Such strategic initiatives are set to help Ciner in revenue growth in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Eco-system Analysis With an Emphasis on Circular Economy

- 4.4 Container Glass - Industry Landscape

- 4.5 Russia-Ukraine Conflict - Impact on the Market Eco-System

- 4.6 Import and Export Analysis

- 4.7 Cost Analysis With Key Drivers (Components and Energy Consumption)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand for Glass Packaging in Beverage Industry

- 5.1.2 Recyclability Benefits Offered by Glass Packaging Drive Sustainability

- 5.2 Market Challenges

- 5.2.1 Alternative Packaging Options Challenging the Market Growth

- 5.3 Analysis of the Increasing Emphasis on Glass Recycling and the Current Recyclability Rate in the United Kingdom

- 5.4 Comparative Analysis of Collection and Recycling of Container Glass in the United Kingdom as Opposed to the European Market

- 5.5 Analysis of the Overall Glass Manufacturing Industry in the United Kingdom

- 5.6 Regulatory Framework

- 5.7 Demand for Glass Containers and Bottles - Retail and Foodservice Industries

- 5.8 Consumer Trends and Preference for Glass Packaging

- 5.9 Industry Standards - Bottle Sizes and Shapes

- 5.10 United Kingdom Glass Production Analysis

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Beverages

- 6.1.1.1 Alcoholic

- 6.1.1.1.1 Beer and Cider

- 6.1.1.1.2 Wine and Spirits

- 6.1.1.1.3 Other Alcoholic Beverages

- 6.1.1.2 Non-alcoholic

- 6.1.1.2.1 Carbonated Soft Drinks

- 6.1.1.2.2 Milk

- 6.1.1.2.3 Water and Other Non-alcoholic Beverages

- 6.1.2 Food

- 6.1.3 Cosmetics

- 6.1.4 Other End-user Industries

- 6.1.1 Beverages

- 6.2 By Color

- 6.2.1 Amber

- 6.2.2 Flint

- 6.2.3 Green

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Verallia Packaging (Verallia SA)

- 7.1.2 Ciner Glass Ltd

- 7.1.3 O-I Glass Inc.

- 7.1.4 Ardagh Group SA

- 7.1.5 Glassworks International

- 7.1.6 Gaasch Packaging

- 7.1.7 Berlin Packaging

- 7.1.8 Vidrala SA

- 7.1.9 Beatson Clark

- 7.1.10 Stoelzle Flaconnage

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET