Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408582

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408582

United States White Cement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

PUBLISHED:

PAGES: 100 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

The United States white cement market is estimated to be valued at USD 842.99 million in 2024. It is expected to reach USD 957.41 million by 2029, registering a CAGR of 2.58% during the forecast period.

Key Highlights

- Over the medium term, factors such as the growing residential construction in the country and increasing investments in the infrastructure sector are expected to boost the growth of the US white cement market during the forecast period.

- On the other hand, the high production costs are expected to hinder the white cement market.

- Nevertheless, white cement is extensively used in architectural work because of its good aesthetic values, helping create marvelous architectural designs. Thus, the rising demand for white cement over grey cement for adding architectural beauty could provide excellent growth opportunities for the US white cement market.

United States White Cement Market Trends

Type I Cement to Dominate the Market

- White cement is a type of cement produced in white color by limiting the presence of some oxide contents during the manufacturing process. Type I cement is a general-use material used in the fitting of marble, the finishing of tiles, and the installation of countertops. Type I white cement is commonly used to produce architectural concrete. It is durable and provides high strength. Despite being expensive, this product is extensively used because of its advantages.

- The general applications of type I white cement include cast-in-place or precast wall panels, slabs, floors, terrazzo, thin-set and tile grouts, masonry units and mortars, cast stone, stucco, swimming pools and spas, glass fiber reinforced concrete, ornamental statuary, floor tiles, and concrete roof tiles. It can also be used in pavers and traffic safety items such as concrete median barriers, bridge parapets, and pedestrian crosswalks.

- Lehigh White Cement Co. LLC operates two production plants in the United States in Waco, TX, and York, PA, with annual production capacities in million tons. CementirHolding NV has a production capacity of around 10 million tons of white and grey cement.

- In the United States, the repair, expansion, and modernization of infrastructure have become essential, with its infrastructure now supporting the country's construction sector for decades. Cement was produced at 96 plants in 34 states and 2 plants in Puerto Rico. Texas, Missouri, California, and Florida were, in descending order of production, the four leading cement-producing states, accounting for approximately 43% of US production.

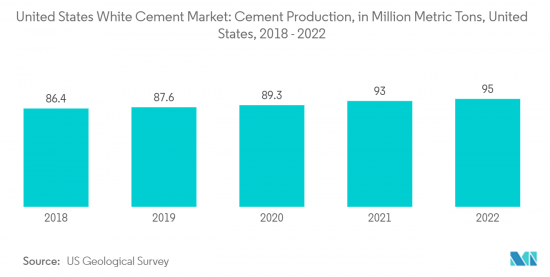

- According to the US Geological Survey's Mineral Commodities Summary 2023, cement production in the United States has been increasing and reached 95 million metric tons in 2022, marking strong growth for the US white cement market.

- From the above points, it can be concluded that due to the rising cement production, the type I cement segment will play a dominant role in white cement production.

Growing Residential Construction to Drive the Market

- In the United States, the growth in population, migration from hometowns to service sector clusters, and the growing trend of nuclear families are reasons that give rise to growth in residential construction. Residential properties such as apartments, bungalows, and villas are gaining popularity in the country, mainly driven by urbanization.

- In addition to new residential construction, the United States is doing massive home renovations. With the growing population of migrants in the country, the need for renovations has become increasingly important. Thus, with such a rise in new homes and renovations for the increasing populace, the white cement market in the country also rises.

- According to the US Census Bureau statistics release, privately-owned housing completions in January 2023 were at a seasonally adjusted annual rate of 1,406,000, registering a growth rate of 1.0% from the revised December estimate of 1,392,000 and 12.8% from the January 2022 rate of 1,247,000. Therefore, increasing housing completions drives the demand for white cement in residential construction.

- Furthermore, in July 2023, privately owned housing starts accounted for 1,452,000 units, reflecting an increase of 3.9% compared to June 2023, as per the US Census Bureau.

- According to the US Census Bureau, new home construction output in the US private sector reached nearly USD 900 billion in 2022, representing an increase of around 11% compared to 2021.

- In June 2022, three significant homebuilders paid USD 111.7 million in the United States for an 836-acre plot of unoccupied property in the West Valley that can house up to 2,800 people. The property, located on the northwest corner of 163rd Avenue and Happy Valley Road in Surprise, is directly northeast of Lennar's current Asante master-planned community, which comprises 3,500 acres and will house more than 14,000 houses.

- Thus, the increasing investments in new residential infrastructure in the United States are expected to boost the white cement market during the forecast period.

United States White Cement Industry Overview

The US white cement market is moderately fragmented. Some of the major players in the market include Almaty's GMBH, Argos USA LLC, Cementer Holdings NV, Cimsa, and Holcim, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50001220

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Residential Construction in the Country

- 4.1.2 Increasing Investments in the Infrastructure Sector

- 4.2 Restraints

- 4.2.1 High Production Costs

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Production Capacity

- 4.6 Import and Consumption of White Cement (Breakdown by States) (Volume in Tons)

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Type I Cement

- 5.1.2 Type III Cement

- 5.1.3 Other Product Types

- 5.2 Application

- 5.2.1 Residential

- 5.2.2 Infrastructure

- 5.2.3 Commercial

- 5.2.4 Industrial and Institutional

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share (%) Analysis

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Almaty's Gmbh (OYAK)

- 6.3.2 Argos USA LLC

- 6.3.3 Cementer Holding NV (Lehigh White Cement Co. LLC)

- 6.3.4 CEMEX SAB De CV

- 6.3.5 CIMSA

- 6.3.6 Federal White Cement

- 6.3.7 Heidelberg Materials

- 6.3.8 HOLCIM

- 6.3.9 Royal El Minya Cement (SESCO Cement Corp.)

- 6.3.10 Royal White Cement Inc.

- 6.3.11 Suwannee American Cement (CRH PLC)

- 6.3.12 Titan America LLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Demand for White Cement over Grey Cement for Adding Architectural Beauty

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.