PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408737

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408737

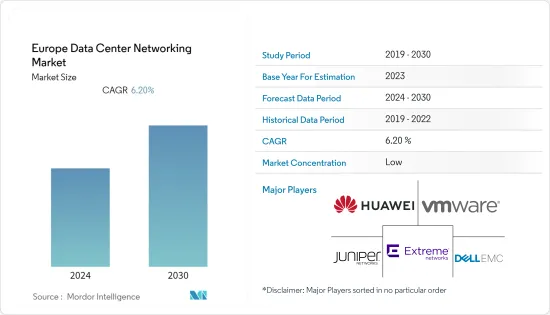

Europe Data Center Networking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2030

The Europe data center networking market reached a value of USD 6.5 billion in the previous year, and it is further projected to register a CAGR of 6.2% during the forecast period.

Key Highlights

- Within Europe, clients and data centers are located close to each other, so 80% of European data centers provide latency of no more than 50 milliseconds. Together with dense coverage of high-speed data transmission channels, this allows businesses and their clients to get fast access to data 24/7.

- Data centers in the region are concentrating on the reduction of high power consumption, WAN consolidation, and bandwidth requirements, creating growth opportunities for data center interconnect, leading to major market demand.

- The upcoming IT load capacity of the Europe data center Server market is expected to reach 18K MW by 2029. The region's construction of raised floor area is expected to increase 87.6 million sq. ft by 2029.

- The region's total number of racks to be installed is expected to reach 4.3 million units by 2029. The United Kingdom is expected to house the maximum number of racks by 2029.

- There are close to 210 submarine cable systems connecting Europe, and many are under construction. One such submarine cable that is estimated to start service in 2025 is SeaMeWe-6, which stretches over 19,200 km with a landing point in Marseille, France.

Europe Data Center Networking Market Trends

IT and Telecom to Hold Significant Share

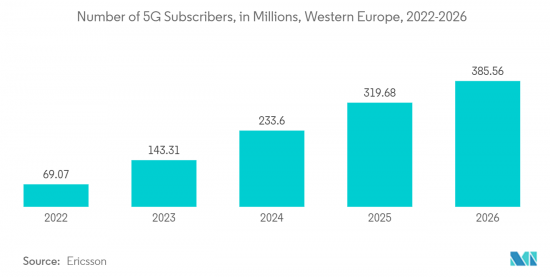

- In Europe, players in the telecommunications industry are faced with shrinking revenues and profitability, as well as the effects of regulatory pricing intervention and consolidation. The rapidly increasing 4G penetration and the upcoming 5G wave are adhering telecom vendors to invest in the data center market. Recently, Swedish network provider Net4Mobility, a joint venture between local carriers Tele2 and Telenor, has announced plans to connect 90% of the nation's population to its 5G network by the end of 2023.

- The Netherlands has also quickly modernized with cutting-edge technology, solidifying its position as one of Europe's leading telecom markets. The goals of the European Union (EU) Gigabit Society are supported by the Dutch government, such as all homes should have access to broadband networks with speeds of at least 100 Mbps, and the vast majority should be taking advantage of 1 Gbps by 2023.

- Recently, Huawei Technologies extended its 5G portfolio for European markets by launching a version of its blade AAU antenna tailored to meet EU requirements that supports all existing network bands, including 3G, 4G, and 5G under sub 6Ghz network band added, with support the coverage of several suppliers at the same time with 400 MHz.

- With the French government promoting cloud usage, businesses in France are more likely to use public cloud services. For government agencies, the French government's economic recovery plan stresses a cloud-first strategy. Despite worries about data protection and sovereignty, many enterprises in the country are using the public cloud.

- The French National Agency for the Security of Information Systems (ANSSI) will provide certificates to confirm that cloud data is stored in Europe and that data loss prevention mechanisms used by providers are functional. The French government is also concentrating on platform-as-a-service deployments for artificial intelligence (AI), big data, and collaborative work suites. Five government cloud projects worth more than EUR 100 million (USD 118 million) have been found.

- In October 2021, Thales and Google Cloud announced a strategic partnership to jointly develop a French hyperscale cloud offering. A joint venture with Thales will run it as the primary shareholder, and it will meet the French 'Trusted Cloud' standards. With this new service, French businesses and government agencies will have access to all of the power, security, flexibility, agility, and sovereignty that the two respective technologies have to offer.

United Kingdom to Hold Significant Growth

- The Federation of Small Businesses (FSB) states that, as of 2022, there were 5.5 million small businesses in the UK, accounting for 99.2% of the total business in the region. Additionally, small- and medium-sized enterprises (SMEs) account for three-fifths of the employment and around half of the UK's private sector turnover. A growing shift towards Hyperscale data centers to efficiently support robust, scalable applications is anticipated to propel the data center networking market in the United Kingdom.

- Through measures in five critical areas - human capital, lab-to-market innovations, networking, regulation, and infrastructure - the UK government continues to support growth and industry development. With almost 65% of the UK's artificial intelligence (AI) enterprises and startups headquartered in London, the survey, backed by the All-Party Parliamentary Group on Artificial Intelligence (APPG AI), ranks London as the most demanded city for investment and talent. London is home to 1300 AI startups, accounting for 65% of the UK AI ecosystem.

- The UK is one of the most digitally advanced economies. The government invests in 5G and next-generation digital technologies to support businesses to build back better after COVID-19. In line with consumer demand, the cloud computing segment is expected to shift inherently to include the use of multi-cloud in enterprises.

- The UK government has launched a EUR 30 million competition to turn the country into a leading global destination for developing the next generation of 5G networks in the hopes of fostering new research collaboration between international and homegrown players in the country's public telecoms networks. The scheme is part of the UK government's diversification policy, which was announced in December 2020 following the decision to remove Huawei equipment from national infrastructures.

- According to the telecom regulator, Ofcom (Office of Communication, UK), 96% of UK premises have access to superfast broadband, and 46% had access to gigabit-capable broadband as of September 2021. In rural areas, superfast broadband is available in 83% of residences. According to Ofcom, at least one cell operator's 5G signal is present in the vicinity of about 50% of establishments.

- Over the next two years, Amazon Web Services (AWS) will invest EUR 1.8 billion (USD 2.196 billion) in cloud computing infrastructure in the United Kingdom, more than doubling its previous commitment. SAP will also create a secure UK-based cloud service and open new offices in London and Manchester as part of a EUR 250 million (USD 295 million) five-year investment plan (approximately GBP 212 million) (USD 292.56 million). These developments and trends will drive the studied market in the region as networking equipment are one of the crucial devices for data centers and cloud storage.

Europe Data Center Networking Industry Overview

The Europe data center networking market exhibits a notable level of fragmentation among its key players, and they have sharpened their competitive edge in recent years. Some of the major players in this sector include Extreme Networks Inc., Dell EMC, and VMware Inc. These industry leaders, commanding a significant market share, are actively engaged in expanding their customer base across the region. They employ strategic collaborative initiatives to enhance their market presence and drive profitability.

In November 2022, VMware, Inc. introduced its cutting-edge SD-WAN solution. This innovative offering includes a new SD-WAN Client designed to empower enterprises to securely, reliably, and optimally deliver applications, data, and services across diverse networks to any device.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Need of Cloud Storage and Rsing Demand for Reliable Application Performance

- 4.2.2 Surge in Adoption of 5G Deployment in Major Countries

- 4.3 Market Restraints

- 4.3.1 Increasing Network Complexity

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 By Product

- 5.1.1.1 Ethernet Switches

- 5.1.1.2 Router

- 5.1.1.3 Storage Area Network (SAN)

- 5.1.1.4 Application Delivery Controller (ADC)

- 5.1.1.5 Other Networking Equipment

- 5.1.2 By Services

- 5.1.2.1 Installation & Integration

- 5.1.2.2 Training & Consulting

- 5.1.2.3 Support & Maintenance

- 5.1.1 By Product

- 5.2 End-User

- 5.2.1 IT & Telecommunication

- 5.2.2 BFSI

- 5.2.3 Government

- 5.2.4 Media & Entertainment

- 5.2.5 Other End-Users

- 5.3 Country

- 5.3.1 France

- 5.3.2 United Kingdom

- 5.3.3 Sweden

- 5.3.4 Austria

- 5.3.5 Belgium

- 5.3.6 Germany

- 5.3.7 Ireland

- 5.3.8 Italy

- 5.3.9 Norway

- 5.3.10 Poland

- 5.3.11 Spain

- 5.3.12 Switzerland

- 5.3.13 Netherlands

- 5.3.14 Denmark

- 5.3.15 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Extreme Networks Inc.

- 6.1.2 Dell EMC

- 6.1.3 Vmware, Inc.

- 6.1.4 Huawei Technologies Co. Ltd.

- 6.1.5 Juniper Networks Inc.

- 6.1.6 Arista Networks Inc.

- 6.1.7 NEC Corporation

- 6.1.8 HP Development Company, L.P.

- 6.1.9 Fortinet, Inc.

- 6.1.10 Array Networks, Inc.

- 6.1.11 Radware Corporation

- 6.1.12 A10 Networks, Inc.

- 6.1.13 Moxa Inc.

- 6.1.14 Lenovo Group Limited

- 6.1.15 Broadcom Corporation

- 6.1.16 Cisco Systems Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS