PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408746

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1408746

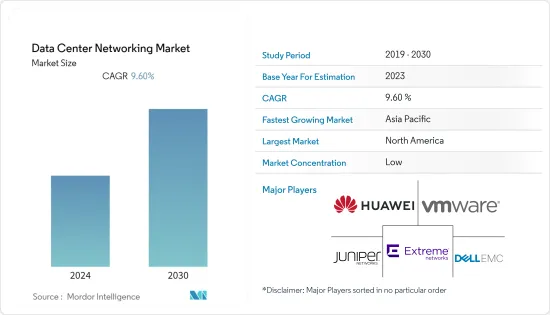

Data Center Networking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2030

The global data center networking market reached a value of USD 24.5 billion in the previous year, and it is further projected to register a CAGR of 9.6% during the forecast period.

Key Highlights

- Networking solutions have gained significant traction in the past few years, primarily owing to the rising need for load balancing, improving performance, as well as to handle much more advanced requirements. Bandwidth demand is growing much faster than the company budgets, and cyber attacks such as distributed denial-of-service (DDoS) are constantly on the rise. It has become a challenge for companies to securely and efficiently deliver their applications at the speed the users expect. This factor leads to major market demand.

- The rise in digitalization will likely increase the demand for data centers, proportionately driving the networking market. Significantly, industry-wide investment in edge computing will transform the profile of the data center ecosystem over the next four years, raising the edge component of total computing by 29%, from 21% of total computing to 27% in 2026. The extent of the industry's ongoing shift to the edge is among the significant findings from a new global survey of data center industry specialists from Vertiv.

- The upcoming IT load capacity of the global data center server market is expected to reach 71K MW by 2029. The region's construction of raised floor area is expected to increase 273.9 million sq. ft by 2029. The region's total number of racks to be installed is expected to reach 14.2 million units by 2029. North America is expected to house the maximum number of racks by 2029.

- There are close to 500 submarine cable systems connecting the regions globally, and many are under construction. One such submarine cable that is estimated to start service in 2025 is CAP-1, which stretches over 12,000 km with a landing point in Grover Beach, United States.

Data Center Networking Market Trends

Application Delivery Controller to Hold Significant Share

- The application delivery controllers primarily provide security and access to the applications at peak times. As computing is moving toward the cloud, software application delivery controllers (ADCs) have been performing tasks that have been traditionally performed by custom-built hardware. They also offer additional functionalities and flexibility for application deployment.

- In today's digital business environment, businesses focus on staying agile and innovative to compete, grow, and thrive. That puts DevOps front and center in digital business strategy as companies seek simple, streamlined ways to develop, deploy, change, and manage applications. The ADC is critical in enabling the full speed and agility that DevOps makes possible.

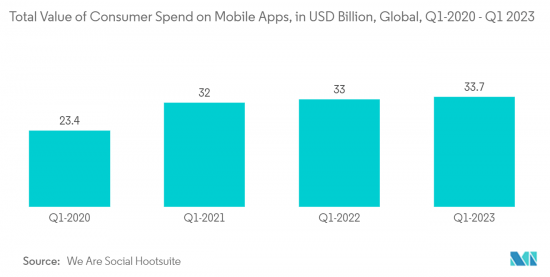

- Moreover, We Are Social and Hootsuite data indicates that consumer spending on mobile applications grew over the past few years, starting at USD 3.7 billion till quarter-one 2023, which is accelerating the demand for the ADC with features that enhance the performance of applications.

- With organizations focusing on extracting greater value from their growing data volumes, market vendors are introducing scalable, secure, and cost-effective modern ADC solutions. For instance, in May 2021, Array Network announced a software version (version 10.2.x) and innovative hardware platforms (the x800 Series) for its APV Series application performance controllers. APV x800 Series physical appliances (APV1800, 2800, 5800, etc.) offer production across multiple metrics, 40 Gig-E interfaces, and improved SSL performance.

- More users are surfing the web on smartphones, tablets, and other mobile devices compared to a laptop or desktops, resulting in the generation of large amounts of data. According to the GSM Association, by 2025, the United States is expected to have the highest smartphone adoption globally.

- Market vendors continuously invest in R&D activities to introduce innovative product offerings to gain more market presence and customer base. For instance, in August 2022, F5 announced the launch of a new traffic management and security solution designed to offer better control over its customers' fleets of NGINX instances. The newly launched F5 NGINX Management Suite 1.0 comes with a centralized dashboard to provide high visibility and control of NGINX instances, application programming interface (API) management workflows, application delivery services, and security solutions.

Asia-Pacific To Hold Significant Market Growth

- In Asia-Pacific, the hyper-connectivity environment has reinforced the importance of telcos, which play a foundational role in supporting consumers' and enterprises' connectivity and collaboration needs. Across Asia-Pacific, 75% of the operators registered positive revenue growth. South Korea is second only to Hong Kong in the world rankings of telecom market maturity.

- The need for data centers is increasing significantly and placing a greater emphasis on effectiveness and low latency. China and India are putting much effort into overtaking their competitors globally in constructing data centers, which is generating a booming demand for processing capacity as larger organizations attempt to scale up their data centers to assure the stability and reliability of data services.

- The South Korean government employed cloud computing technologies to enhance its banking on the country's super-fast internet connectivity, e-government services, and stable long-term evolution (LTE) availability. This is expected to contribute to the market's growth positively over the forecast period.

- Owing to technological advancements, there is an increase in the number of connected devices in the studied market. Moreover, strong government backing and substantial private sector investment are behind the growth of China's cloud computing industry. Furthermore, 5G and 5 G-enabled devices will exponentially increase the devices' interconnectivity. As a result, it increases connected devices, thereby directly augmenting the need for controlling the data traffic and security of the cloud-based applications.

- As financial organizations are increasingly adopting hybrid cloud, public cloud, and multi-cloud strategies to meet the need for compliance, competition, and modernization, the demand for networking solutions is anticipated to grow in the coming years. According to F5's State of Application Strategy Report- Financial Services Edition for 2022, 69% of financial services organizations in the Asia Pacific region have deployed multi-cloud strategies.

- In addition, the increasing internet users and data traffic in countries like China, India, and Indonesia are further augmenting the growth of ADC solutions in the region. With the evolving digital era, market vendors are offering more innovative network solutions and products for end-users, ensuring they have the best technology experience driving the market segment.

- For instance, in June 2022, Cyber security and application delivery solutions provider Radware and managed security service provider OneSecure announced the expansion of their collaboration agreement. In order to enhance OneSecure's Webyith defacement and domain phishing monitoring service for the ASEAN enterprises, the MSSP announced to expand of the cyber security suite to include Radware's Application Protection-as-a-service offering and cloud-distributed denial-of-service (DDoS) protection service.

Data Center Networking Industry Overview

The global data center networking market exhibits a notable degree of fragmentation, characterized by a competitive landscape that has intensified in recent years. Key industry players, including Extreme Networks Inc., Dell EMC, and VMware, Inc., among others, have solidified their positions and demonstrated substantial market shares. These major players are actively concentrating on expanding their customer base across various regions. To achieve this goal, they employ strategic collaborative initiatives designed to bolster their market share and enhance overall profitability.

In November 2022, VMware, Inc. introduced its cutting-edge SD-WAN solution, which encompasses a novel SD-WAN Client. This innovation aims to assist enterprises in delivering applications, data, and services securely, reliably, and efficiently across diverse networks to any device.

In September 2022, AppViewX, a prominent player specializing in automated machine identity management (MIM) and application infrastructure security, made a significant announcement. The company joined F5's Technology Alliance Program (TAP), ushering in a partnership that is expected to jointly promote enterprise application security and delivery solutions. This collaboration focuses on the management of applications and the enhancement of cybersecurity measures across on-premises, cloud, and edge locations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Need of Cloud Storage and Rsing Demand for Reliable Application Performance

- 4.2.2 Increasing Cyberattacks Among Enterprises

- 4.3 Market Restraints

- 4.3.1 Increasing Network Complexity

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 By Product

- 5.1.1.1 Ethernet Switches

- 5.1.1.2 Router

- 5.1.1.3 Storage Area Network (SAN)

- 5.1.1.4 Application Delivery Controller (ADC)

- 5.1.1.5 Other Networking Equipment

- 5.1.2 By Services

- 5.1.2.1 Installation & Integration

- 5.1.2.2 Training & Consulting

- 5.1.2.3 Support & Maintenance

- 5.1.1 By Product

- 5.2 End-User

- 5.2.1 IT & Telecommunication

- 5.2.2 BFSI

- 5.2.3 Government

- 5.2.4 Media & Entertainment

- 5.2.5 Other End-Users

- 5.3 Region

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 South America

- 5.3.5 Middle East

- 5.3.6 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Extreme Networks Inc.

- 6.1.2 Dell EMC

- 6.1.3 Vmware, Inc.

- 6.1.4 Huawei Technologies Co. Ltd.

- 6.1.5 Juniper Networks Inc.

- 6.1.6 Arista Networks Inc.

- 6.1.7 NEC Corporation

- 6.1.8 HP Development Company, L.P.

- 6.1.9 Fortinet, Inc.

- 6.1.10 Array Networks, Inc.

- 6.1.11 Radware Corporation

- 6.1.12 A10 Networks, Inc.

- 6.1.13 Moxa Inc.

- 6.1.14 Lenovo Group Limited

- 6.1.15 Broadcom Corporation

- 6.1.16 H3C Holding Limited

- 6.1.17 NVIDIA (Cumulus Networks Inc.)

- 6.1.18 Cisco Systems Inc.

- 6.1.19 F5 Networks Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS