PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1431072

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1431072

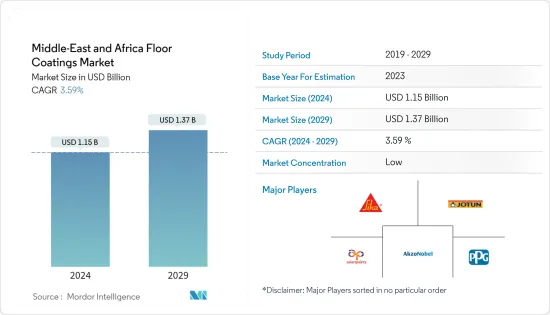

Middle-East and Africa Floor Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Middle-East and Africa Floor Coatings Market size is estimated at USD 1.15 billion in 2024, and is expected to reach USD 1.37 billion by 2029, growing at a CAGR of 3.59% during the forecast period (2024-2029).

In 2020, COVID-19 impacted the construction industry across the Middle East region. However, the upsurge in construction activities post-pandemic has propelled the consumption of floor coatings.

Key Highlights

- In the short term, the residential and commercial construction activities in Saudi Arabia and UAE will likely drive the market.

- On the flip side, strict regulations on VOCs released from floor coatings may restrain industry growth.

- The rising application of polyaspartic coatings in industrial construction will likely offer new avenues to the floor coatings market.

- Saudi Arabia dominates the market and is expected to witness the highest CAGR during the forecast period. The Saudi government is focusing on developing infrastructure, education, industrial, and healthcare sectors for economic expansion.

MEA Floor Coatings Market Trends

Rising Application of Floor Coatings in the Industrial Sector

- The industrial sector dominated the regional floor coatings market. The core sectors, such as chemical, automotive, manufacturing, and other industries, such as food and beverages and electrical and electronics, are some of the significant consumers of floor coatings.

- Epoxy floor coatings are well-suited coatings for industrial applications. Many industrial sites, warehouses, and manufacturing factories rely on epoxy floors to maintain clean and safe conditions for workers, equipment, and inventory. It also provides a shiny high-gloss surface that can significantly increase the brightness of interior areas.

- The rising automotive industry is one of the key factors driving the demand for floor coatings within the region. In 2021, automotive production in South Africa stood at 499 thousand units, up from 447 thousand units in 2020. The industry observed a 12% of growth rate in the year. Additionally, Saudi Arabia motor vehicle sales recorded 556,559 units in Dec 2021, compared with 452,544 units in the previous year.

- In the automotive industry, the floor coating needed to comply with the RMA automotive international factory standard, ensuring that the floors are highly slip-resistant, low maintenance, and easy to clean.

- Furthermore, the construction of new assembly plants for automotive production is also likely to increase the consumption of floor coatings. Several manufacturers are expanding their assembly plants with the growing demand for vehicles. For instance, in January 2022, The Saudi National Automotive Manufacturing Co. confirmed laying the foundation stone for the first car assembly plant in Jubail Industrial City in Saudi Arabia. The production capacity of the plant is set to hit 30,000 cars annually.

- Therefore, considering the abovementioned factors, the demand for the floor coatings market is expected to rise significantly in the industrial application segment in the near future.

Saudi Arabia is Expected to Dominate the Market

- Saudi Arabia dominated the Middle East and Africa floor coatings, with a significant market share in terms of revenue, and is anticipated to maintain its dominance during the forecast period.

- The growing residential and commercial construction activities in the country are the key drivers for the floor coatings market. In the commercial, flooring coating is a commonly used option, to have stability, durability, and enhanced appearance value of the floor. Due to the high performance of epoxy flooring, which is obtained by a mixture of resin and hardening chemicals, its use in homes has continued to soar.

- Saudi Arabia's Vision 2030 transformation agenda has so far released almost USD 1 trillion worth of infrastructure and real estate projects across the country. More than 100,000 hotel rooms, 1.3 million new houses, and more than 3 million square meters of top-notch office space will be added to the string of new cities being built along Saudi Arabia's western coast.

- Furthermore, the Saudi Ministry of Housing announced its goal to work with real estate companies to build about 100,000 new housing units for a total of SAR 65 billion (about USD 17.3 billion). There are already 19 projects in nine regions of the country that have already been announced, and 40 more private projects are anticipated to build 14,000 "villa" housing units across the country.

- All such factors related to the construction sector in the country showcase a strong growth in the demand for floor coatings in the country over the forecast period.

MEA Floor Coatings Industry Overview

The floor coatings market in the Middle East and Africa is fragmented. Some of the major players in the market include Akzo Nobel NV, Jotun, PPG Industries Inc., Sika AG, and Asian Paints, among others (not in particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Construction Activities in Saudi Arabia

- 4.1.2 Strong Demand for Floor Coatings in Industrial Sector

- 4.2 Market Restraints

- 4.2.1 Strict Regulations on VOCs Released for Floor Coatings

- 4.2.2 Other Market Restraints

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Epoxy

- 5.1.2 Polyaspartics

- 5.1.3 Acrylic

- 5.1.4 Polyurethane

- 5.1.5 Other Product Types

- 5.2 Floor Material

- 5.2.1 Wood

- 5.2.2 Concrete

- 5.2.3 Other Floor Materials

- 5.3 End-user Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.4 Construction Type

- 5.4.1 New Construction

- 5.4.2 Repair & Refurbishing/Rehabilitation

- 5.5 Geography

- 5.5.1 Saudi Arabia

- 5.5.2 South Africa

- 5.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Akzo Nobel NV

- 6.4.2 ArmorPoxy

- 6.4.3 Asian Paints

- 6.4.4 BASF SE

- 6.4.5 Epoxy-Coat

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Jazeera Paints

- 6.4.8 Jotun

- 6.4.9 Kansai Nerolac Paints Limited

- 6.4.10 LATICRETE International Inc.

- 6.4.11 Mapei

- 6.4.12 PPG Industries Inc.

- 6.4.13 Sika AG

- 6.4.14 Tambour

- 6.4.15 The Sherwin-Williams Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Investment in the Construction Sector