Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1431080

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1431080

Europe Commercial Aircraft Cabin Seating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2030)

PUBLISHED:

PAGES: 126 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

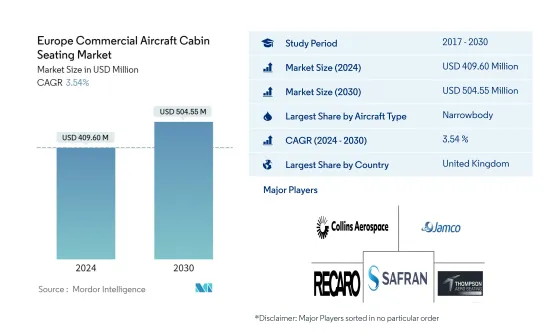

The Europe Commercial Aircraft Cabin Seating Market size is estimated at USD 409.60 million in 2024, and is expected to reach USD 504.55 million by 2030, growing at a CAGR of 3.54% during the forecast period (2024-2030).

Key Highlights

- Narrowbody is the Largest Aircraft Type : A fleet of narrowbody aircraft adds flexibility in terms of fleet management and helps reduce the operating costs of airlines, resulting in its rapid adoption. The demand for premium economy seats in low-cost carriers has increased.

- Narrowbody is the Fastest-growing Aircraft Type : The convenience of air travel, combined with its low cost due to increased domestic airline competition, is anticipated to increase the demand for narrowbody aircraft. Narrowbody aircraft hold a dominant share due to the increasing domestic air traffic across the world.

- Business and First Class is the Largest Cabin Class : The growing per capita income in developing countries and the increasing number of business-class seats globally have aided the growth of business and first-class categories.

- United Kingdom is the Largest Country : The United Kingdom is expected to register a major revenue share during 2023-2029 due to the increasing levels of air transportation and a rising number of commercial aircraft orders from major airlines.

Europe Commercial Aircraft Cabin Seating Market Trends

Narrowbody is the largest Aircraft Type

- Modern-generation aircraft seats are made from lightweight non-metallic materials and lightweight designs to reduce fuel expenses and increase the aircraft's sustainability. The demand for seats with enhanced features and technologically based convenience is increasing, which will accelerate market expansion in the future.

- An enhanced seating structure with more developed space than economy-class seats is becoming highly essential due to rising preferences for business-class travelers. Worldwide airline operators and OEMs are increasing their efforts to reduce weight and develop a sustainable way to manage the airline industry in consideration of the zero-emission 2050 goal.

- During 2017-2022, narrowbody aircraft accounted for the majority of deliveries, which accounted for 81% of the total aircraft delivered. In 2020, as a result of restrictions on travel, including domestic and international routes, there were delays in airline companies adding new aircraft to their fleets. But in 2021, with the reopening of borders and increasing vaccination rates, the procurement of new aircraft has exceeded the pre-pandemic levels by 35%.

- It is anticipated that certain factors, including the rising adoption of innovative cabin seats, the growing demand for luxury air travel, and the huge number of aircraft orders, will drive the market during the forecast period. On this note, as a part of fleet expansion and the demand driven by new narrowbody aircraft with long range on major routes, airlines such as Rostec ordered 250 aircraft, Ryanair ordered 200 aircraft, and Wizz Air ordered 102 narrowbody aircraft. This is expected to aid the overall seating market in the region.

United Kingdom is the largest Country

- The importance of comfortable seating in aircraft has increased. The major reason for this is to provide a better passenger experience. The major European airline companies are now focusing on modernized cabins with customized seats to improve passengers' experiences.

- The increase in passenger traffic is driving the demand for new aircraft procurements, thereby creating the need for a larger cabin interior market. For instance, in 2021, air passenger traffic in the whole of Europe was recorded to be 1.05 billion people, which was a growth of 191% from the traffic registered in 2020. Airline companies in the European region are implementing fleet expansion plans to cater to the growing air passenger traffic across major countries. The United Kingdom, Germany, and Spain accounted for 36% of the total air passenger traffic in the European region. These countries will likely generate the maximum demand for new aircraft compared to other European countries.

- The increasing air passenger traffic will eventually drive aircraft orders and deliveries. The major commercial aircraft manufacturers, namely Boeing and Airbus, are expected to deliver a large number of aircraft in the region. About 2,545 new jets are expected to be delivered across the region. Of these, 2,169 jets are expected to be narrow-body aircraft. There is a high preference for smaller and more economical aircraft, along with the introduction of long-range narrow-body aircraft. The success of LCCs is high in this region. The major airline companies in the region, such as Air France, British Airways, and Lufthansa, are focusing on improving the overall passenger experience in the aircraft market. This is expected to play a vital role in aiding the demand for commercial aircraft cabin interior products in the region.

Europe Commercial Aircraft Cabin Seating Industry Overview

The Europe Commercial Aircraft Cabin Seating Market is fairly consolidated, with the top five companies occupying 97.93%. The major players in this market are Collins Aerospace, Jamco Corporation, Recaro Group, Safran and Thompson Aero Seating (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 93605

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 New Aircraft Deliveries

- 4.3 GDP Per Capita (Current Price)

- 4.4 Revenue Of Aircraft Manufacturers

- 4.5 Aircraft Backlog

- 4.6 Gross Orders

- 4.7 Expenditure On Airport Construction Projects (Ongoing)

- 4.8 Expenditure Of Airlines On Fuel

- 4.9 Regulatory Framework

- 4.10 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION

- 5.1 Aircraft Type

- 5.1.1 Narrowbody

- 5.1.2 Widebody

- 5.2 Country

- 5.2.1 France

- 5.2.2 Germany

- 5.2.3 Spain

- 5.2.4 Turkey

- 5.2.5 United Kingdom

- 5.2.6 Rest Of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Adient Aerospace

- 6.4.2 Collins Aerospace

- 6.4.3 Expliseat

- 6.4.4 Jamco Corporation

- 6.4.5 Recaro Group

- 6.4.6 Safran

- 6.4.7 STELIA Aerospace (Airbus Atlantic Merginac)

- 6.4.8 Thompson Aero Seating

- 6.4.9 ZIM Aircraft Seating GmbH

7 KEY STRATEGIC QUESTIONS FOR COMMERCIAL AIRCRAFT CABIN INTERIOR CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.