PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1431294

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1431294

HVAC Field Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

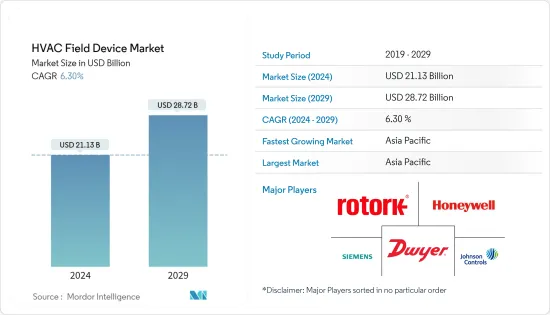

The HVAC Field Device Market size is estimated at USD 21.13 billion in 2024, and is expected to reach USD 28.72 billion by 2029, growing at a CAGR of 6.30% during the forecast period (2024-2029).

The pandemic significantly influenced the HVAC industry, as demand for the systems observed a significant drop during the initial months, owing to lockdown restrictions and businesses refraining from investing in new equipment. Due to the pandemic, many construction projects were halted across the world. Reduced commercial, residential, and industrial construction activities temporarily dampened the demand for HVAC field devices.

Key Highlights

- Consequently, the US government has significantly invested in federal funds that can be used in public buildings, schools, and other settings to improve indoor air quality. For instance, the American Rescue Plan provided USD 350 billion for state and local governments, along with USD 122 billion for schools, that can be used for ventilation and filtration upgrades.

- The end users are adopting smart HVAC equipment to predict when maintenance is needed before a real issue occurs. The latest HVAC technologies, which utilize an Internet of Things (IoT) system, are embedded with sensors, software, and connectivity, enabling the HVAC system to exchange data with other connected devices. IoT systems enhance preventative maintenance by sensing data on air quality and equipment status. Moreover, the latest and most affordable Internet of Things HVAC technology makes it significantly easier to view insights across several equipment types, such as rooftop air-handling units, air- and water-cooled heat pumps, variable air volume (VAV) with reheat systems, etc. These developments in HVAC equipment are expected to further drive the studied market.

- Rising consumer purchasing power coupled with increasing disposable income, especially in developing economies, also positively impacts the market. For instance, according to the National Bureau of Statistics of China, the average disposable income per capita for residents in China was 36,883 yuan, a nominal increase of 5.0% compared to the previous year and an absolute increase of 2.9% after adjusting for inflation in 2022.

- In addition to this, the rising manufacturing sector has further bolstered the scope of HVAC equipment and field devices. According to the World Manufacturing Production Quarter 3 2022 Report by the United Nations Industrial Development Organization, manufacturing production in Asia and Oceania experienced an output growth of 4.4%, ahead of North America (3.5%) and Europe (1.7%). The manufacturing sector in Latin America and the Caribbean expanded by 4.9%, and South Africa grew by 3.0%.

- Furthermore, Eastern Europe has colder climatic conditions, and the demand for heating solutions is significant in these countries, such as the Czech Republic, Poland, Bulgaria, and others. Like other countries in the region, measures to increase energy efficiency in the heating and cooling sectors are rising. The Intelligent Energy Europe Programme of the EU, which co-founded Stratego, claims that an investment of EUR 50 billion between 2010 and 2050 will save enough fuel to lower the costs of the energy system. As part of this investment, district heating's share stood at EUR 5 billion and individual heat pumps at EUR 15 billion.

- Several governments worldwide are offering financial benefits to promote the use of energy-saving equipment in residential and commercial spaces. For instance, the U.S. government introduced the Energy Policy Act of 2005, which provides a tax deduction of up to USD 1.80 per square foot for new commercial buildings. Buildings that reduce their regulated energy consumption by 50% in comparison to the specifications outlined in the American Society of Heating, Refrigerating, and Air-Conditioning Engineers, Inc.'s 2001 new construction standard (ASHRAE 90.1) were eligible for the tax benefit. Government initiatives and rising awareness about environmental degradation and energy management are expected to keep the demand for energy-efficient HVAC control systems, including field devices.

HVAC Field Device Market Trends

Residential Sector is Expected to Hold Significant Market Share

- One of the key drivers propelling the market for HVAC field devices is the growing percentage of energy consumption in residential buildings, which has led to the usage of energy retrofit systems to increase the efficiency of buildings. For instance, HomeServe introduced its benefits program for home HVAC subscriptions in August 2022. This helps utilities accomplish energy efficiency goals and improve customer satisfaction by lowering the cost of replacing an HVAC (heating and air conditioning) system, which is expensive for households.

- Growing demand for air conditioners has been one of the most critical factors driving the market in this sector. Central air conditioning is expected to become the most common way people across the globe cool their homes. According to the IEA, air conditioners and electric fans account for about a fifth of the total electricity in buildings worldwide, or 10% of all global electricity consumption. Over the next three decades, the use of ACs is set to soar, becoming one of the top drivers of global electricity demand.

- Furthermore, one of the key factors propelling the expansion of the HVAC field device market in the residential sector is the rising concern for indoor air quality. Also, several governments are encouraging the purchase of this high-efficiency equipment by enforcing laws to satisfy energy demand and implementing sales programs for these air conditioners at discounted prices. By routinely making upward changes to the Energy Labeling Program in favor of energy-efficient systems, the Bureau of Energy Efficiency (BEE) and the Ministry of Electricity, for instance, have been enforcing rules on the amount of electricity consumed by residential air conditioners.

- According to OBERLO, 60.4 million US homes were expected to be actively utilizing smart home devices in 2023, which was 3% more than in 2022, when 57.4 million households used smart home devices. In 2023, the proportion of households utilizing smart home technology is expected to be 46.5% of all households. This penetration is likely to lead to an increase in demand for smart devices with low energy consumption, including HVAC systems.

- To reduce CO2 emissions, vendors and numerous governments are also focused on residential decarbonization. As a result, it is anticipated that the adoption of heat pumps in the residential sector will gain traction, which will aid homeowners in reducing their utility costs and promote a decrease in the use of fossil fuels, which feed global climate change. Major vendors like Carrier, Daikin, Johnson Controls, Danfoss, and others are constantly investing in residential product launches, which is one of the major factors driving the market.

Asia-Pacific is Expected to Hold Significant Market Share

- The construction industry in China has witnessed massive growth due to sustainable construction policies and a shift toward a service-led economy over the past few years. Investing in large-scale infrastructure projects has been a vital part of the Chinese government's strategy to boost growth.

- According to the China Construction Industry Association, in 2021, residential structures accounted for a significant share of finished construction in China. Buildings intended for housing accounted for over 67% of the completed floor space. As the country's economy grows, people migrate from rural areas to major cities, increasing demand for residential accommodation in these locations. Furthermore, apartments utilized as investment properties drive up demand. Such massive residential construction is expected to drive the study market.

- According to MLIT (Japan), there were about 859.5 thousand home starts in Japan in 2022. Compared to the prior year, this represented an increase of 0.4%. Over 10,200 office building construction projects began in Japan in 2022. Such a vast number of constructions would drive the studied market.

- Further, according to IBEF, India invested USD 2.4 billion in real estate assets over the last year, a 52% increase annually. From April 2000 to September 2022, FDI in the industry, comprising construction development and operations, totaled USD 55.18 billion. Such a massive rise in real estate would allow the studied market to grow.

- Further, the new data center construction projects in the country are also pushing the market's growth in South Korea. For instance, SK Broadband, the internet infrastructure division of SK Telecom, recently announced plans to invest USD 1.75 billion in the creation of a brand-new hyperscale data center encircling a startup campus. The first phase of the data center and startup cluster development is expected to be completed by 2024 and comprise four data center buildings, with plans to add 12 more by 2029.

HVAC Field Device Industry Overview

The global HVAC field device market is highly fragmented and has several major players. In terms of market share, a few of the major players currently dominate the market. These major players with prominent shares in the market are focusing on expanding their customer base across foreign countries. These companies leverage strategic collaborative initiatives to increase their market shares and profitability.

In March 2023, Honeywell introduced its Versatilis transmitters for condition-based monitoring of rotating equipment such as pumps, motors, compressors, fans, blowers, and gearboxes. Honeywell Versatilis transmitters provide relevant measurements of rotating equipment, delivering intelligence that can improve safety, availability, and reliability across industries.

In August 2022, Airzone announced it was entering the rapidly growing North American market with an exclusive smart control solution for HVAC inverter systems. Airzone's Aidoo Pro acted as the bridge between proprietary HVAC inverter and mini-split manufacturers' protocols and IoT device APIs, including for the popular Ecobee, Honeywell, and Nest smart thermostats. The Aidoo Pro enables HVAC professionals to integrate HVAC inverter systems with leading smart thermostats, preserving all inverter features and providing unparalleled efficiency, energy savings, connectivity, and comfort.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Development of the Construction Market

- 5.1.2 Supportive Government Regulations Including Incentives for Saving Energy through Tax Credit Programs

- 5.1.3 The Emergence of IoT and Product Innovations to Aid Replacements

- 5.2 Market Restraints

- 5.2.1 Dependence on Macro-economic Conditions

- 5.2.2 High Initial Cost of Energy Efficient Systems

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Control Valve

- 6.1.2 Balancing Valve

- 6.1.3 PICV

- 6.1.4 Damper HVAC

- 6.1.5 Damper Actuator HVAC

- 6.1.6 Other Types

- 6.2 By Sensors

- 6.2.1 Environmental Sensors

- 6.2.2 Multi Sensors

- 6.2.3 Air Quality Sensors

- 6.2.4 Occupancy & Lighting

- 6.2.5 Other Sensors

- 6.3 By End-user Industry

- 6.3.1 Commercial

- 6.3.2 Residential

- 6.3.3 Industrial

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Siemens AG

- 7.1.2 Honeywell International Inc.

- 7.1.3 Johnson Controls International PLC

- 7.1.4 Rotork Plc

- 7.1.5 Dwyer Instruments Inc.

- 7.1.6 Belimo Holding AG

- 7.1.7 Robert Bosch GmbH

- 7.1.8 Electrolux AB

- 7.1.9 Azbil Corporation

- 7.1.10 Danfoss A/S

- 7.1.11 Daikin Industries Ltd.

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET