PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1431462

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1431462

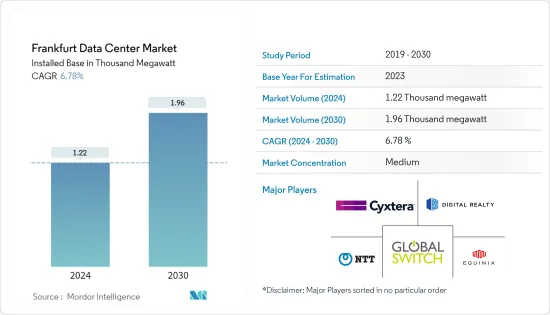

Frankfurt Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2030)

The Frankfurt Data Center Market size in terms of installed base is expected to grow from 1.22 Thousand megawatt in 2024 to 1.96 Thousand megawatt by 2030, at a CAGR of 6.78% during the forecast period (2024-2030).

Key Highlights

- The main drivers anticipated to drive the market expansion are the increasing demand for energy-efficient data centers, considerable investment by colocation service and managed service providers, and expanding hyperscale data center building. Additionally, the development of big data, cloud computing, and the Internet of Things (IoT) has made it possible for businesses to invest in new data centers to preserve business continuity. Additionally, industrial development is expected to prosper due to the rising need for security, operational efficiency, improved mobility, and bandwidth. Software-based data centers boost industry growth by providing a higher level of automation.

- Frankfurt has undergone significant economic growth, becoming a financial and commercial center in Germany and then throughout Europe. The city's significance as the most significant financial center on the European mainland is highlighted by the presence of the European Central Bank, the German Stock Exchange, the German Central Bank, hundreds of commercial banks, and branches of foreign central banks. The city's digital transition has been accelerated by all of these financial institutions driving the data center demand in the country.

- The outbreak of the COVID-19 pandemic affected data center construction in the market studied as it has delayed the construction of several new facilities. Ongoing construction from enterprises and colocation service providers witnessed a halt. Projects pipeline with openings across Q4 2020 and Q1 2021 are majorly affected. The same has been attributed to data center infrastructure-related supply chain disruptions. With problematic imports already in place, the situation worsened as many vendors are dependent on importing IT and power and cooling infrastructure solutions.

- The increased demand from logistics, healthcare, e-commerce, and manufacturing sectors has attracted several cloud and colocation service providers to invest and expand their presence in the country. For instance, recently, Worldstream, a global IaaS services provider with company-owned data centers in the Netherlands and more than 15,000 dedicated servers installed announced the expansion of its presence across Europe with the deployment of a new data center in maincubes' FRA01 facility in Frankfurt, Germany. It includes the installation of a new Point-of-Presence for Worldstream's10Tbit/s global network. It allows Worldstream to offer a private cloud, dedicated servers, block and object storage, DDoS protection, colocation, and other IaaS services from Frankfurt.

- Moreover, to meet the rising demands of the customer, the firms are constructing new data centers in the region. For instance, in February 2022, The second stage of construction of one of Vantage's data center complexes in Frankfurt, Germany, has been revealed. On its 55MW EU campus (FRA1) in Offenbach, the business announced it would erect the second of three buildings there. When fully constructed, the plant would have a 16MW capacity and be 13,000 square meters (140,000 square feet) in size. It will begin serving customers in the first half of 2024.

- While the basic prices for electricity are similar across Europe, the electricity costs of German data centers are over six times higher than those of their European competitors due to taxes, charges, and network fees. Electricity accounts for approximately 50% of the operating costs of German data centers, which weakens the competitiveness of German data centers immensely. According to DgtlInfra (Digital Infrastructure), In 2020, the power supply of the existing data centers in Frankfurt, Germany, was 425 Megawatts, compared to Amsterdam at 390 Megawatts and Paris at 210 Megawatts, with leases to Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, among others.

Frankfurt Data Center Market Trends

Tier 3 Segment is Expected to Hold Significant Share of the Market

- To be defined as a Tier III facility, a data center must adhere to the following specification. The facility should offer N+1 (the amount required for operation plus a backup) fault tolerance. Also, the Tier III facility providers can undergo routine maintenance without a hiccup in the overall operations. However, unplanned maintenance and emergencies may cause problems affecting the system. These problems may potentially affect customer-facing operations.

- These data center facilities provide a 99.982% uptime. The companies using these Tier III facilities are often growing companies or businesses that are considerably larger than the average SMBs (Small to Medium Businesses). These Tier III facilities also offer most of the features of a Tier IV infrastructure facility without some elite protection. For instance, enterprises can leverage the advantage of dual power sources and redundant cooling as the network streams are fully backed up.

- Moreover, owing to the robust cloud market growth amid the global pandemic, many companies accelerated their digital transformation efforts. Companies like Tencent Cloud added four data centers to increase global coverage by 30% in 2021. The company added four new data center locations globally, out of which one is a Tier III facility located in the prime network hub of Frankfurt. The move pushes its network footprint to 27 regions and 66 availability zones worldwide. Such expansion efforts are increasing the city's adoption of Tier III facilities.

- The difficulties of maintaining a private IT infrastructure have long prompted businesses to investigate other data and computing solutions. There is, thankfully, an option. Companies may get all of the power and control of an on-premises solution with the flexibility and cost-effectiveness of the cloud by using colocation data centers. Today's data center providers are using the data center as a service (DCaaS) model to offer attractive solutions for fast-growing businesses trying to compete in an increasingly congested market where speed and adaptability are crucial to success.

- According to Ookla (speedtest.net), in February 2023, the average download speed in Germany was 83.69 Mbit per second. This was faster than in October 2022, when the average speed was 77.34 Mbit per second. Data centers can have varying internet speeds depending on many factors such as network architecture, location, and capacity. Some data centers have speeds of 5Gb/sec, while others can have speeds of 100Gb/sec or beyond. However, as the demand for faster and more efficient data processing continues to increase, many data centers are upgrading their networks to support speeds ranging from 10GB to 100GB.

Cloud & IT is Expected to Drive the Market

- The amount of data stored and processed by the telecom and IT industry is enormous. The advent of mobile data and subscriptions, coupled with their rapid usage, has increased data traffic growth and hence, data centers in Germany. With the introduction of 5G and Cloud, the country's demand is expected to grow exponentially. The country's IT industry necessitates data storage and hyper-scale data centers for its operations according to their size. Additionally, cloud storage selection has progressed over the years due to growth in SaaS providers in the country, enabling cloud storage providers to expand their capacities. It is expected to increase the demand for the data center market.

- The pragmatic choices of data center construction solutions, efficient innovation ecosystem, and substantial private sector investment made the sector significant in the current market. Data centers of the telecom and IT industries across the globe are focusing on services that enable the data centers to meet the future demand by virtualizing and enhancing servers, thus, making transformational changes in storage capabilities and addressing the green IT issues. Typical hardware infrastructure optimization projects being handled by significant organizations are resulting in the reduction of total cost ownership by more than 20%, and this is a prompting aspect for enterprises to adopt more efficient construction solutions.

- For example, in February 2022, A 112-megawatt, 1.2 million sqft (108k sqm), hyperscale data centre campus is being built by CloudHQ, a hyperscale data centre developer and operator in the US and Europe, in Offenbach, Germany, a city that borders Frankfurt to the southeast. With a total investment of EUR 1.1 billion (USD 1.18 billion), CloudHQ's Frankfurt data centre campus will be the biggest in Germany once fully constructed.

- According to Federal Network Agency, in 2022, there were roughly 169 million mobile connections in Germany, such huge number would create opportunities for cloud deployment. Mobile cloud computing is a growing area that provides mobile users with access to computing resources and services through the cloud. This can allow mobile devices to offload computationally intensive tasks to remote servers, reducing the strain on the mobile device's processing power and battery life. Examples of mobile cloud applications include mobile gaming, location-based services, and augmented reality applications.

Frankfurt Data Center Industry Overview

The Frankfurt Data Center market is moderately consolidated with the presence of several players like Equinix Inc, Digital Realty, NTT, Cyxtera and many more. The companies continuously invest in strategic partnerships and product developments to gain substantial market share. Some of the recent developments in the market are:

In October 2022, Mainova, a German energy company, is expanding into the data centre market. The corporation broke ground on a new plant in Frankfurt, Germany. A groundbreaking ceremony for the facility was held earlier this month, according to Mainova WebHouse, a subsidiary of the energy firm. The new data centre will have up to 113,000 square feet (10,500 square metres) of area spread across two data centre buildings. It will also provide a total IT load of 30MW. The data centre campus is set to open in 2024.

In October 2022, Stack Infrastructure plans to establish a new data center in Frankfurt in a former Coca-Cola bottling facility. The company revealed that it intends to build an 80MW facility in the Liederbachdistrict of the German city. The campus will house four institutions and will incorporate green measures such as rainwater gathering and giving excess heat to a future local residential development.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 KEY INDUSTRY TRENDS

- 4.1 Smartphone Users

- 4.2 Data Traffic per Smartphone

- 4.3 Mobile Data Speed

- 4.4 Broadband Data Speed

- 4.5 Regulatory Framework

- 4.6 Value Chain Analysis

5 MARKET OUTLOOK

- 5.1 IT Load Capacity

- 5.2 Raised Floor Space

- 5.3 Number of Racks

6 MARKET SEGMENTATION

- 6.1 DC Size

- 6.1.1 Small

- 6.1.2 Medium

- 6.1.3 Large

- 6.1.4 Massive

- 6.1.5 Mega

- 6.2 Tier Type

- 6.2.1 Tier 1 & 2

- 6.2.2 Tier 3

- 6.2.3 Tier 4

- 6.3 Absorption

- 6.3.1 Utilized

- 6.3.1.1 Colocation Type

- 6.3.1.1.1 Retail

- 6.3.1.1.2 Wholesale

- 6.3.1.1.3 Hyperscale

- 6.3.1.2 End User

- 6.3.1.2.1 Cloud & IT

- 6.3.1.2.2 Telecom

- 6.3.1.2.3 Media & Entertainment

- 6.3.1.2.4 Government

- 6.3.1.2.5 BFSI

- 6.3.1.2.6 Manufacturing

- 6.3.1.2.7 E-Commerce

- 6.3.1.2.8 Other End User

- 6.3.2 Non-Utilized

- 6.3.1 Utilized

7 COMPETITVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Digital Realty

- 7.1.2 Equinix

- 7.1.3 NTT

- 7.1.4 Cyxtera

- 7.1.5 Global Switch

- 7.1.6 Iron Mountain

- 7.1.7 Cyrusone

- 7.1.8 Leaseweb

- 7.1.9 Telehouse

- 7.1.10 Deft

- 7.1.11 Zenlayer

- 7.1.12 Lumen Technologies, Inc.

- 7.1.13 DARZ

- 7.1.14 Aixit

- 7.1.15 Vantage data centres

- 7.2 Market share analysis (In terms of MW)

- 7.3 List of Companies