Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644979

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644979

Germany Solar Inverter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 200 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

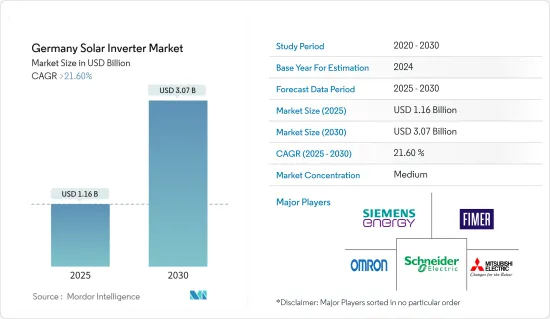

The Germany Solar Inverter Market size is estimated at USD 1.16 billion in 2025, and is expected to reach USD 3.07 billion by 2030, at a CAGR of greater than 21.6% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the growing adoption of solar PV in commercial and industrial sectors and increasing investments in solar energy projects are expected to drive the market.

- On the other hand, the recent subsidy cuts on solar panels by governments in the Europe region is expected to hinder the market growth during the study period.

- Nevertheless, Many inverter manufacturers strive for innovation and adoption of the latest technologies powered by solar energy. This factor is expected to create immense opportunities for Germany's solar inverter market in the near future.

Germany Solar Inverter Market Trends

Central Inverters Segment Expected to Dominate the Market

- A central inverter is a large grid feeder. It is often used in solar photovoltaic systems with rated outputs over 100 kWp. Floor or ground-mounted inverters convert DC power collected from a solar array into AC power for grid connection. These devices range in capacity from around 50kW to 1MW and can be used indoors or outdoors.

- As central inverters are used for utility-scale applications, they should produce the same voltage and frequency as that of the electric grid where they are used. As there are a lot of different electric grid standards worldwide, manufacturers are allowed to customize these parameters to match the specific requirements in terms of the number of phases; most central inverters manufactured are three-phase inverters.

- Acoriding to International Renewable Energy Agency (IRENA), by the end of December 2022, the country will have 58.726 GW of solar PV capacity.

- Moreover, to promote the utilization of central inverters, several companies collaborated. For instance, In May 2022, Gamesa Electric and Siemens AG signed a strategic partnership agreement addressing the employment of its Proteus central inverters for PV and Energy Storage projects. Under this agreement, Siemens could use Gamesa Electric Proteus inverters for PV and BESS projects. These central inverters are distinguished by their high-power output of up to 4700kVA and a record efficiency of 99.45%, providing integrated solutions for solar and storage projects.

- In January 2022, Sungrow launched its new '1+X' central modular inverter with an output capacity of 1.1MW. This 1+X modular inverter can be combined into eight units to reach a power of 8.8MW and features a DC/ESS interface for connecting energy storage systems (ESS).

- Therefore, the Central Inverters Segment is expected to dominate the market based on the above factors, like increased power demand.

Increasing Investments in Solar Energy Projects to Drive the Market

- Germany is the largest solar photovoltaic market in Europe in terms of installed capacity, which justifies it being one of the front runners in energy and climate security globally. The country has witnessed significant developments in the solar PV market. It will likely continue to do so due to a combination of self-consumption with attractive feed-in premiums, especially for medium- to large-scale commercial systems ranging from 40 kW to 750 kW.

- The cumulative solar photovoltaic installed capacity in Germany has witnessed significant growth. The solar PV installed capacity will be 66.5 GW in 2022 and 58.7 GW in 2021. There has been 13.2 % year-on-year growth in 2022 compared to the previous year.

- Significant investments in the solar energy sector are being made to set up new solar energy projects. For instance, In March 2022, Germany intends to invest USD 216 billion in renewable energy to reduce its reliance on Russian gas, which has left it susceptible to the effects of the conflict in Ukraine.

- Additionally, in April 2022, Germany's Federal Network Agency announced that the agency had selected 201 proposals with a combined output of 1.084 GW under the solar auction, up from 510.34 MW in July 2021. The bids in the round ranged from EUR 0.040 to EUR 0.055 per kWh. The volume-weighted average price stood at EUR 0.0519 (USD 0.057) per kWh, up from EUR 0.050 per kWh in the previous round.

- Furthermore, in July 2022, Germany agreed on proposals for the government's special "climate and transformation fund" to invest USD 180 billion over the following four years to expedite the energy shift to a cleaner economy and less reliant on Russian energy sources.

- As of October 2022, Germany was home to over 2.58 million energy-generating solar photovoltaic sites. This figure illustrates the peak number of sites recorded in the period of consideration.

- Owing to the above points, increasing investments in the country's solar energy market are expected to dominate the Germany solar inverter market soon.

Germany Solar Inverter Industry Overview

The Germany solar PV inverters market is semi-fragmented. Some of the major players in the market (in no particular order) include FIMER SpA, Schneider Electric SE, Siemens Energy AG, Mitsubishi Electric Corporation, and Omron Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 5000152

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

- 1.4 Study Deliverables

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Adoption of Solar PV in Commercial and Industrial Sectors

- 4.5.1.2 Increasing Investments in Solar Energy Projects

- 4.5.2 Restraints

- 4.5.2.1 Recent Subsidy Cuts on Solar Panels by Governments in the Europe Region

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Inverter Type

- 5.1.1 Central Inverters

- 5.1.2 String Inverters

- 5.1.3 Micro Inverters

- 5.2 Application

- 5.2.1 Residential

- 5.2.2 Commercial and Industrial

- 5.2.3 Utility-Scale

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 FIMER SpA

- 6.3.2 Schneider Electric SE

- 6.3.3 Siemens Energy AG

- 6.3.4 Mitsubishi Electric Corporation

- 6.3.5 General Electric Company

- 6.3.6 SMA Solar Technology AG

- 6.3.7 Omron Corporation

- 6.3.8 Delta Energy Systems Inc.

- 6.3.9 Huawei Technologies Co. Ltd.

- 6.3.10 KACO New Energy GmbH

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation and Adoption of the Latest Technologies Powered by Solar Energy

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.