Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693871

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693871

Europe Cheese - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 201 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

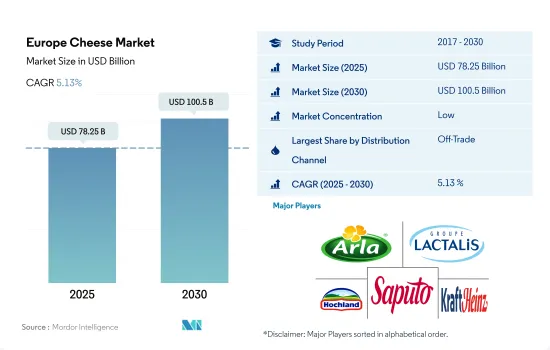

The Europe Cheese Market size is estimated at 78.25 billion USD in 2025, and is expected to reach 100.5 billion USD by 2030, growing at a CAGR of 5.13% during the forecast period (2025-2030).

Greater presence of supermarket and hypermarket is promoting the retailing segment in europe

- The high market share of off-trade channels is primarily driven by hypermarkets/supermarkets. Strategic product positioning, dedicated shelf space for cheese products, and the availability of local brands, along with global brands, are key factors driving cheese sales through these channels. In Europe, supermarkets/hypermarkets covered 58.45% of cheese sales, in terms of value, in 2022.

- Key supermarket and hypermarket chains have established a network of stores in different locations across the region to cover the maximum market. Some of the major operators identified in the market include Metro Group, Ahold Delhaize, Fidesco, AmazonFresh, Walmart, Tesco, REWE Group, Kaufland, and Aldi. Germany, France, and the United Kingdom hold the largest number of supermarket and hypermarket stores in the region. In 2022, three countries collectively acquired a 36.29% share in the overall cheese sales volume through supermarkets and hypermarkets in Europe.

- The online channel is projected to be the fastest-growing distribution channel as modern consumers prefer online grocery purchases due to their busy lifestyles. The increasing number of online cheese shops in response to the rising number of internet users is anticipated to drive online sales of natural cheese during the forecast period. In 2022, the share of households with internet access was recorded as 93%, up from 72% in 2011. Netherlands, France, the United Kingdom, Germany, and Italy are the countries with high penetration of internet users. Key online cheese retailers include FROMAGES.COM, The East London Cheese Board, La Gourmeta, Love Cheese, Italia Regina, and Frank and Sal. The online channel sales value is anticipated to register a CAGR of 5.15% during 2023-2029.

Explosive cheese consumption led by Germany, France, and Italy is fueling the growth

- Cheese has traditionally been considered the preferred outlet for milk from the European Union after local fresh-milk requirements have been met. The cheese segment acquired a market volume share of 11.20% in 2022, with a volume sales growth of 8.46% from 2017 to 2022. Cheese is an integral part of European cuisines like Italian, British, German, Greek, and French.

- Germany, France, and Italy are highly cheese-consuming countries and collectively covered 39.53% volume of the overall cheese consumed in the region in 2022. More than 400 types of cheeses are produced in Italy. Mozzarella, parmesan, and Pecorino are commonly used cheeses in regional Italian cuisines. Pizza, Balsamic di Modena, Risotto, Tortellini, Polenta, and Pesto are key Italian dishes featuring cheese either as a topping or filling.

- The fact that an average French individual consumes 26.5 kilograms of cheese per year adds to its prominence. In fact, almost 40% of people consume cheese every day, and over 95% have included it in their regular diet. The consumption of value-added dairy products like cheese is growing in the United Kingdom. This has influenced processors using raw milk delivered off farms. In 2019, the volume of raw milk going into cheese rose by 1.09 billion liters.

- Supermarkets/hypermarkets are identified as major distribution channels for cheese in Europe. The segment acquired a 44.33% share of the overall sales volume in 2022. On-trade consumption of cheese is driven by the presence of leading fast-food brands such as McDonald's, KFC, Taco Bell, Subway, and Burger King. Burger King, a France-based fast-food restaurant chain, has more than 480 stores across France. Volume sales across on-trade channels are projected to register a CAGR of 0.73% during 2023-2029.

Europe Cheese Market Trends

The increased cheese consumption in Europe across various European cultures contributes to its high demand and consumption

- The per capita consumption of cheese increased by 3% in 2022 compared to 2021. Europeans have been eating cheese for at least 7,000 years. Cheese is an integral part of European cuisines like Italian, British, German, Greek, and French. Approximately nine million metric tons of cheese are consumed annually in the European Union. Different dishes in European cuisine, including pasta, pizza, sandwiches, and burgers, are incomplete without cheeses. A consumer study conducted in August 2021 revealed that 71% of respondents among the 1,554 surveyed population eat cheese regularly.

- Much of the cheese consumed is also produced in Europe, mainly in France, Italy, Germany, and the Netherlands. These countries collectively covered 39.53% volume of the overall cheese consumed in the region in 2022. Cheese is highly valued among French people due to its diverse flavor and the social aspect it offers. In fact, almost 40% of people consume cheese every day, and over 95% have included it in their regular diet. The fact that an average French individual consumes 26.5 kilograms of cheese per year adds to its prominence.

- The consumption patterns of various nations vary significantly. Italian producers of cheeses have around 400 different varieties. Regional Italian cuisines frequently use mozzarella, parmesan, and pecorino cheeses. Pizza, Balsamic di Modena, Risotto, Tortellini, Polenta, and Pesto are key Italian dishes featuring cheese either as a topping or filling. Cheese made from cow milk is most preferred across the regions. For instance, among the 1,000 types of cheeses that exist in France, Raclette cheese, creamy Camembert, and Emmental, among others, are highly consumed ones that are made from cow's milk.

Europe Cheese Industry Overview

The Europe Cheese Market is fragmented, with the top five companies occupying 13.04%. The major players in this market are Arla Foods amba, Groupe Lactalis, Hochland Holding GmbH & Co. KG, Saputo Inc. and The Kraft Heinz Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50000735

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Cheese

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Product Type

- 5.1.1 Natural Cheese

- 5.1.2 Processed Cheese

- 5.2 Distribution Channel

- 5.2.1 Off-Trade

- 5.2.1.1 By Sub Distribution Channels

- 5.2.1.1.1 Convenience Stores

- 5.2.1.1.2 Online Retail

- 5.2.1.1.3 Specialist Retailers

- 5.2.1.1.4 Supermarkets and Hypermarkets

- 5.2.1.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.2.2 On-Trade

- 5.2.1 Off-Trade

- 5.3 Country

- 5.3.1 Belgium

- 5.3.2 France

- 5.3.3 Germany

- 5.3.4 Italy

- 5.3.5 Netherlands

- 5.3.6 Russia

- 5.3.7 Spain

- 5.3.8 Turkey

- 5.3.9 United Kingdom

- 5.3.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Arla Foods amba

- 6.4.2 Bel Group

- 6.4.3 Egidio Galbani SRL

- 6.4.4 Granarolo SpA

- 6.4.5 Groupe Lactalis

- 6.4.6 Groupe Sodiaal

- 6.4.7 Hochland Holding GmbH & Co. KG

- 6.4.8 Kingcott Dairy

- 6.4.9 Koninklijke ERU Kaasfabriek BV

- 6.4.10 Saputo Inc.

- 6.4.11 Savencia Fromage & Dairy

- 6.4.12 The Kraft Heinz Company

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.