Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693941

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693941

GEO Satellite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 207 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

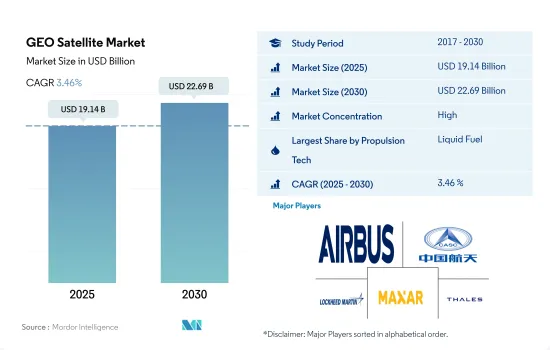

The GEO Satellite Market size is estimated at 19.14 billion USD in 2025, and is expected to reach 22.69 billion USD by 2030, growing at a CAGR of 3.46% during the forecast period (2025-2030).

Liquid fuel propulsion is expected to surge during the forecast period

- A satellite's propulsion system plays a key role in changing its speed and direction. It is also used to adjust the position of the spacecraft in orbit. After entering orbit, the spacecraft requires attitude control to correct its orientation with respect to the Earth and the Sun. In some cases, it is necessary to move the satellite out of orbit, and without the ability to adapt to orbit, the satellite is considered dead. Therefore, the importance of powertrain systems is expected to drive market growth. Different types of fuel are used for different purposes. Liquid propellants use rocket engines that use liquid propellants. Gas fuels can also be used but are less popular due to their low density and difficulty using conventional pumping methods. In 2020, the market was declined by 44%, impacted by the manufacturing and operational challenges faced by the pandemic.

- The liquid system that made it possible has proven to be highly efficient and reliable. These include hydrazine systems, single or dual propulsion systems, hybrid systems, cold/hot air systems, and solid propellants. It is used when strong thrust or quick maneuvering is required. Therefore, liquid systems will continue to be the space propulsion technology of choice if their total thrust capacity is sufficient to meet mission requirements.

- On the other hand, electric propulsion is commonly used to hold stations for commercial communications satellites, and its high specific impulse makes it the primary propulsion for some space exploration missions. The utilization of electric propulsion systems is expected to surge during 2023-2029, and the overall market is expected to surge by 22%. New satellite launches are expected to accelerate market growth during the forecast period.

- The global GEO satellite market is expected to grow significantly in the coming years, driven by various satellite applications across different industries. The market can be analyzed concerning North America, Europe, and Asia-Pacific, which are the major regions in terms of market share and revenue generation. Between 2017 and 2022, 147 satellites were manufactured and launched by various operators in this segment into GEO. Of these 147 satellites, nearly 75% were launched for communication purposes.

- North America is expected to dominate the global GEO satellite market due to the presence of several leading market players, such as Boeing, Lockheed Martin, and Northrop Grumman. The increasing demand for high-speed internet, navigation services, and remote sensing applications in the region is expected to fuel market growth. Between 2017 and 2022, the region accounted for 30% of the total satellites manufactured and launched into GEO.

- In Europe, the GEO satellite market is expected to grow significantly due to the increasing demand for high-speed internet and communication services. The ESA has been investing heavily in the development of advanced satellite technology, which is expected to further drive the growth of the market in the region. During 2017-2022, the region accounted for 11% of the total satellites manufactured and launched into GEO.

- In Asia-Pacific, increasing investments in the development of satellite technology and infrastructure by governments and private organizations in the region are expected to further boost the growth of the market. During 2017-2022, the region accounted for 59% of the total satellites manufactured and launched into GEO.

Global GEO Satellite Market Trends

Satellites are equipped with more sophisticated communication devices, advanced imaging capabilities, and advanced sensors that, in addition to other functions, contribute to their mass

- The mass of GEO (geostationary Earth orbit) satellites can vary depending on their specific design, purpose, and the technological advancements integrated. However, certain trends and general considerations have shaped the mass of GEO satellites over time. Over the years, there has been a general trend of increasing the mass of GEO satellites, mainly due to advances in technology and the increasing complexity of satellite payloads. Satellites now carry more advanced communications equipment, high-resolution imaging systems, and sophisticated sensors that, among other capabilities, contribute to their overall mass.

- High-throughput satellites (HTS) are designed to provide enhanced data capacity and faster communication speeds. These satellites employ advanced antenna systems, multiple spot beams, and frequency reuse techniques to maximize their communication capabilities. The additional complexity and larger communication payloads of HTS can result in higher satellite masses.

- GEO satellites primarily serve as relays for communications, providing services such as television broadcasting, internet connectivity, and telecommunications. The size and volume of the communication payload have increased as the demand for higher bandwidth and more advanced services has increased. To accommodate larger and more powerful communications equipment, GEO satellites have become heavier. During 2017-2022, over 140 satellites were launched in GEO globally. The surge in the number of military satellites is expected to aid the GEO satellite segment in the forecast period.

The growth of the global market is expected to be supported by indigenous space capabilities

- A geostationary orbit is a circular orbit located at an altitude of approximately 35,786 km above the Earth's equator. GEO satellites offer a range of market applications and services such as communications, navigation, surveillance, remote sensing, weather forecasting, satellite broadcasting, and internet services. Between 2017 and May 2022, over 145+ GEO satellites were launched globally.

- The Canadian space industry adds USD 2.3 billion to the country's GDP and employs 10,000 people, according to the government. The government reports that 90% of Canadian space firms are small- and medium-sized businesses. The Canadian Space Agency's (CSA) budget is modest, with its budgetary spending for 2022-23 estimated at USD 329 million.

- In Asia-Pacific, currently, only China, India, and Japan have full end-to-end space capacity and complete space infrastructure and technology for all communication, Earth observation (EO), and navigation satellites, including for the manufacturing of satellites, rockets, and spaceports. Other countries in the region rely on international cooperation to carry out their respective space programs. However, this trend is expected to change to some extent over the coming years, although many countries in the region are developing indigenous space capabilities as part of their latest agile strategies. In June 2022, South Korea launched the Nuri rocket, putting six satellites into orbit, making it the seventh country in the world to successfully launch a payload weighing more than one ton.

GEO Satellite Industry Overview

The GEO Satellite Market is fairly consolidated, with the top five companies occupying 88.46%. The major players in this market are Airbus SE, China Aerospace Science and Technology Corporation (CASC), Lockheed Martin Corporation, Maxar Technologies Inc. and Thales (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50001253

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Mass

- 4.2 Spending On Space Programs

- 4.3 Regulatory Framework

- 4.3.1 Global

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 China

- 4.3.6 France

- 4.3.7 Germany

- 4.3.8 India

- 4.3.9 Iran

- 4.3.10 Japan

- 4.3.11 New Zealand

- 4.3.12 Russia

- 4.3.13 Singapore

- 4.3.14 South Korea

- 4.3.15 United Arab Emirates

- 4.3.16 United Kingdom

- 4.3.17 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 Satellite Mass

- 5.2.1 10-100kg

- 5.2.2 100-500kg

- 5.2.3 500-1000kg

- 5.2.4 above 1000kg

- 5.3 End User

- 5.3.1 Commercial

- 5.3.2 Military & Government

- 5.4 Propulsion Tech

- 5.4.1 Electric

- 5.4.2 Gas based

- 5.4.3 Liquid Fuel

- 5.5 Region

- 5.5.1 Asia-Pacific

- 5.5.2 Europe

- 5.5.3 North America

- 5.5.4 Rest of World

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Airbus SE

- 6.4.2 China Aerospace Science and Technology Corporation (CASC)

- 6.4.3 Indian Space Research Organisation (ISRO)

- 6.4.4 Japan Aerospace Exploration Agency (JAXA)

- 6.4.5 Lockheed Martin Corporation

- 6.4.6 Maxar Technologies Inc.

- 6.4.7 Mitsubishi Heavy Industries

- 6.4.8 Northrop Grumman Corporation

- 6.4.9 Thales

- 6.4.10 The Boeing Company

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.