Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693975

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693975

Europe Dog Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 318 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

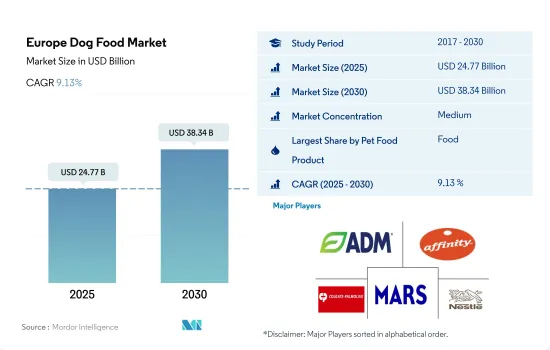

The Europe Dog Food Market size is estimated at 24.77 billion USD in 2025, and is expected to reach 38.34 billion USD by 2030, growing at a CAGR of 9.13% during the forecast period (2025-2030).

Food products and treats were dominating the market due to their regular usage, while veterinary diets comprised the fastest-growing segment

- In 2022, the dog food market accounted for 40.8% of the European pet food market. There was a significant increase of 42% compared to 2017, mainly due to the increased number of dog owners and the growing demand for premium products in the region. The dog population grew by 14.2% in 2022 compared to 2017. The major market shares in 2022 were held by the United Kingdom, Germany, and Russia, accounting for 16.1%, 12.5%, and 9.4%, respectively.

- The food product segment is the largest in the dog food market, and it was valued at USD 13.15 billion in 2022. Dry food is the most popular type of dog food, valued at USD 9.88 billion in 2022. Dog owners prefer dry food because of its longer shelf life and lower cost per serving, making it more convenient and economical to purchase in bulk.

- Treats comprise the second-largest segment of dog food, and they were valued at USD 3.54 billion in 2022. Treats are given to dogs with their regular food to provide additional health benefits, such as aiding digestion and promoting healthy skin and coat. They are also commonly used as training rewards.

- Dog veterinary diets were valued at USD 2.05 billion in the market in 2022. This segment is projected to be the fastest growing, registering a CAGR of 9.9% during the forecast period. The increasing prevalence of digestive issues and chronic kidney diseases in dogs has contributed to the growth of this segment.

- The pet nutraceuticals segment grew by 19.1% in 2022 compared to 2017, driven by the increased awareness of healthy diets, particularly due to rising health concerns in dogs. The market is being driven by the increasing dog population, the specific health needs of dogs, and the growing awareness of pet health among dog owners. It is projected to record a CAGR of 7.5% during 2023-2029.

The United Kingdom is the major European market, while Poland and Russia are the fastest-growing markets

- The European dog food market is witnessing substantial growth, primarily driven by the rising population of pet dogs in the region. The countries with significant dog populations in Europe include Russia, the United Kingdom, Germany, and Spain. Between 2017 and 2021, the European dog food market experienced an increase of about 28.0%, mainly attributed to the growing number of pet dogs, which rose from 84.9 million in 2017 to 97.0 million in 2022.

- Among European countries, the United Kingdom emerged as the largest dog food market, representing around 16.1% of the total market value, i.e., USD 3.13 billion in 2022. The dominance of the United Kingdom can be primarily attributed to high expenditure on dogs. For instance, the average pet expenditure per dog in the United Kingdom stood at USD 646.2 in 2022, the highest among all European countries.

- Germany accounted for about 12.5% of the European dog food market in 2022. The country had a dog population of about 10.6 million, accounting for around 11.0% of the total European dog population in the same year. With the growing dog population and an increasing trend of pet humanization, the German dog food market is anticipated to register a steady CAGR of 3.6% during the forecast period.

- Although Russia held the largest dog population in the region, it only accounted for 9.4% of the market in 2022. This disparity can be attributed to comparatively lower pet expenditure on dogs in the country. The ongoing Ukraine-Russia War has also had a negative impact on the Russian dog food market.

- However, the increasing dog population and pet humanization are the factors anticipated to drive the market during the forecast period.

Europe Dog Food Market Trends

The growing dog-friendly ecosystem in the region is driving the adoption of dogs from animal shelters and rescue organizations

- In Europe, dogs are relatively less popular than cats, with a pet population share of about 29.9%, making them the second-most populous pets after cats in 2022. This is in contrast to the global trend, where dogs are more popular than cats. The dog population in Europe was 21.4% lower than cats in 2022. This was likely because cats are considered lucky in many European countries, such as Italy and Germany. However, the dog population in Europe experienced a significant increase of about 19.1% between 2019 and 2022. The COVID-19 pandemic played a crucial role in this growth, as there was a surge in dog adoptions from animal shelters and rescue organizations. With more people spending time at home, the desire for companionship grew, and dog adoption became an attractive option.

- In 2022, the no. of European households owning pet animals exceeded 90 million, which accounted for 46.0% of the total households. This demonstrates that Europe has a greater inclination toward pet humanization. Among European countries, Russia had the largest population of pet dogs in 2022, making up 18.3% of the total dog population, followed by the United Kingdom with 13.4% and Germany with 11.0%.

- The increase in the dog population in Europe has led to the emergence of various adoption programs. This presents opportunities for businesses to explore new ideas within the pet industry. For instance, some French cafes now offer fine dining experiences for dogs, while companies in the United Kingdom provide paid "paw-ternity" leave for pet parents. Sweden has also implemented regulations to ensure the well-being of pets, emphasizing their health. These trends indicate a positive outlook for the growth of the dog population in Europe during the forecast period.

The surge in demand for high-quality pet food products is increasing the expenditure per pet of pet parents in the region

- Pet expenditure in Europe increased during the historical period because of increased premiumization and spending on different types of food as pet parents became more concerned about the health needs of their pets. These factors helped in increasing the pet expenditure per animal by 24% between 2017 and 2022. In 2022, dogs held the largest share, accounting for 37.9% of the European dog food market, as dogs are fed specialized pet food and have a higher consumption of pet food than cats. For instance, in the United Kingdom, people's average pet food expense was USD 330 in 2022, which was more than a cat's food expense of USD 150. Dogs are provided with services such as pet grooming and training for socialization with other dogs.

- Pet parents provide premium products to their pet dogs. Due to the increasing humanization of pets and rising disposable incomes, pet parents tend to opt for food brands such as Royal Canin, Purina, and Whiskas for their pets. The medium-priced segment of the pet food market is witnessing increased sales due to the similar nutritional values offered by premium products.

- During the pandemic, there was an increase in the sales of pet food through online channels, as the majority of supermarkets had fewer product offerings due to the lockdowns. E-commerce websites also have a higher number of products available. It helped Amazon to be a leader in pet food sales in the United Kingdom, with the website receiving more than 579 million visits annually since the pandemic.

- The rising consumption of medium-priced food and growing awareness about the benefits of healthy, nutritious pet food helped in increasing pet expenditure in the region.

Europe Dog Food Industry Overview

The Europe Dog Food Market is moderately consolidated, with the top five companies occupying 40.12%. The major players in this market are ADM, Affinity Petcare SA, Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), Mars Incorporated and Nestle (Purina) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50001457

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Distribution Channel

- 5.2.1 Convenience Stores

- 5.2.2 Online Channel

- 5.2.3 Specialty Stores

- 5.2.4 Supermarkets/Hypermarkets

- 5.2.5 Other Channels

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Netherlands

- 5.3.5 Poland

- 5.3.6 Russia

- 5.3.7 Spain

- 5.3.8 United Kingdom

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Affinity Petcare SA

- 6.4.3 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.4 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.5 General Mills Inc.

- 6.4.6 Heristo Aktiengesellschaft

- 6.4.7 Mars Incorporated

- 6.4.8 Nestle (Purina)

- 6.4.9 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.