Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693980

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693980

North America Dog Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 303 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

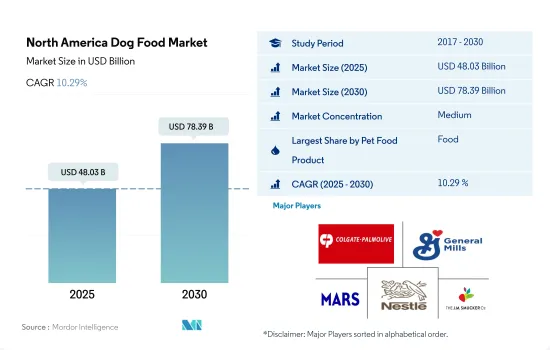

The North America Dog Food Market size is estimated at 48.03 billion USD in 2025, and is expected to reach 78.39 billion USD by 2030, growing at a CAGR of 10.29% during the forecast period (2025-2030).

Veterinary diets comprise the fastest-growing segment, driven by the growing trend of preventative care

- Pet food dominated the market and accounted for about 68.0% of the total market value in 2022. This is because pet food is a staple purchase for most pet owners in the region, regardless of their pet breed size or age. With the increasing trend in the pet population, the pet food market in the region is anticipated to register a CAGR of 10.1% during the forecast period.

- Pet treats accounted for about 15.6% of the total market value in 2022. Generally, treats are mostly preferred by dogs compared to other pet animals. The main purpose of feeding the pets with treats is to train them, maintain their dental health, and reward them. The treats market is anticipated to increase at a CAGR of 10.6% during the forecast period.

- The pet veterinary diets market accounted for about 13.0% of the total market value in 2022. These diets are specifically formulated to address certain health conditions in pets, such as urinary tract diseases, renal failure, and digestive sensitivity. They may also be given to pets as a preventative measure to avoid developing certain health issues. During the forecast period, pet veterinary diets are expected to experience the highest CAGR of 12.3%, indicating a growing demand for these specialized products.

- Pet nutraceuticals or supplements accounted for 3.5% of the market value in 2022. These pet supplements are often given to pets to support overall health and well-being. They can address nutritional deficiencies and support health benefits such as joint, skin, and coat health. The market for pet supplements is anticipated to increase at a CAGR of 6.1% during the forecast period.

- The increasing trend in the pet population and the specific benefits offered by commercial pet foods are anticipated to drive the market during the forecast period.

The growing demand for grain-free, organic, and single meat source dog food products is driving the North American market

- The dog food market in North America was the largest pet food market in the region, accounting for a 49.5% share and reaching USD 36 billion in 2022, an increase of 81.8% from 2017. The increase in the market value was associated with the increase in the adoption of dogs across North American countries by 17.6% between 2017 and 2022.

- In North America, the United States was the largest country in terms of the dog food market due to the increase in demand for high-quality pet food products from pet owners and the rising usage of commercial dog food products. The United States is also the fastest-growing country in the North American dog food market, with an anticipated CAGR of 10.9% during the forecast period, followed by Mexico with 7.2%, with a decrease in usage of homemade food and rising premiumization of pet food products in the region.

- Consequently, with the increasing premiumization among pet parents, dog food products with grain-free or single grain products, single meat source products, organic and natural foods in line with sustainability and climate resilience, along with alternate protein sources such as plant-based protein have higher demand in the premium and super-premium segments in the region. However, the rising concerns about pet health and the benefits of using veterinary diets are estimated to boost the veterinary diets segment to grow faster, with a CAGR of 12.4% during the forecast period.

- The increase in the usage of commercial pet food products, increase in pet premiumization, and humanization with higher disposable income of pet owners are expected to drive the North American dog food market to record a CAGR of 10.4% during the forecast period in the region.

North America Dog Food Market Trends

Growing acquisition of dogs from animal shelters and the evolving pet ecosystem are boosting the market's growth

- Dog adoption is on the rise in North America. Dogs have a higher share than other animals in North America due to the high demand for companionship and dogs' inherent ability to adapt to their owner's routines. This has resulted in an increase in the number of dogs as pets in the region, as developed countries, such as the United States and Canada, witnessed increasing households with dogs as pets. For instance, in 2022, the number of households owning a dog was 65.1 million, and number of households owning a cat was 46.5 million. There were 19% more pet owners in the rural areas of the United States than in urban areas in 2017.

- Small dogs and medium-sized dogs are in high demand. People in the United States living in small apartments are adopting and purchasing dogs weighing between 1 kg and 40 kg. In 2021, dogs with a body weight of less than 11 kg accounted for 47%, and dogs weighing between 11 kg and 18 kg accounted for 31% of the dog population, as smaller dogs require less space compared to large dogs. In 2021, pet parents who considered dogs as family members accounted for 85% of dog owners. This is expected to help in the growth of the dog population as pets in the future.

- Animal shelters are among the key acquisition channels for dog adoption. For instance, in 2020, 38% of dog parents adopted a dog from an animal shelter, whereas 42% purchased from a pet store due to a rise in income levels and the high demand for dogs as companions in big apartments during the pandemic lockdowns.

- Pet humanization and the evolving pet ecosystem are the factors anticipated to help in the growth of the pet population in the region during the forecast period.

The growing trend of premiumization and willingness to provide their pets with eco-friendly pet care products driving the expenditure rate

- A trend of increase in pet expenditure is witnessed in North America. The rise in pet expenditure is due to the availability of different types of pet food and growing premiumization in the United States and Canada. In North America, dog owners prefer to provide their dogs with premium pet food and are willing to adopt eco-friendly pet care products. For instance, in 2022, more than 50% of pet parents were to provide their pets, including dogs, with eco-friendly pet care products by paying a premium price, and 42% of dog owners are providing dogs with premium pet food.

- Pet parents' highest expenses are on pet food and treats, which are expected to increase during the forecast period. For instance, pet food and snacks accounted for 25.8% of expenses incurred for dogs in the United States (USD 2,908) in 2022. They have the highest share and are projected to increase because pet parents treat their pets as family members and raise awareness about specialized pet food. Pet parents are required to spend more in the initial days of dogs as dogs require services such as pet grooming, veterinary care, and pet training for socialization with other dogs. For instance, pet parents spent USD 70-80 for a grooming session in 2022.

- In Canada, there has been an increase in pet parents providing their pets with gifts and services such as pet grooming, pet boarding, and dog walkers. The pet parents' annual expenditure on these services increased from USD 2,075 in 2018 to USD 2,430 in 2021 because they treat their dogs as companions and family members or children. Premiumization and rising awareness about the benefits of quality food are factors anticipated to have helped in increasing pet expenditure in the region.

North America Dog Food Industry Overview

The North America Dog Food Market is moderately consolidated, with the top five companies occupying 59.04%. The major players in this market are Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated, Nestle (Purina) and The J. M. Smucker Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50001462

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Distribution Channel

- 5.2.1 Convenience Stores

- 5.2.2 Online Channel

- 5.2.3 Specialty Stores

- 5.2.4 Supermarkets/Hypermarkets

- 5.2.5 Other Channels

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.3 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.4 General Mills Inc.

- 6.4.5 Mars Incorporated

- 6.4.6 Nestle (Purina)

- 6.4.7 PLB International

- 6.4.8 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.9 The J. M. Smucker Company

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.