Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693981

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693981

North America Pet Diet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 225 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

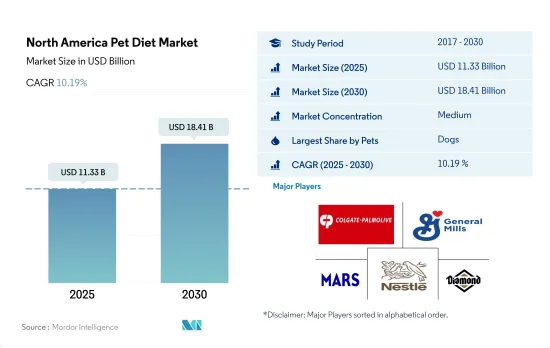

The North America Pet Diet Market size is estimated at 11.33 billion USD in 2025, and is expected to reach 18.41 billion USD by 2030, growing at a CAGR of 10.19% during the forecast period (2025-2030).

Dogs and cats are the largest consumers of pet veterinary diets in the region due to pet owners' increased focus on their pet's health

- Veterinary diets are specialized types of pet food formulated to address specific health conditions of pets. The value of pet veterinary diets increased by 100.1% between 2017 and 2022 due to the advancements in pet nutrition science and research. This has resulted in more specialized veterinary diets that can address a wider range of health issues in pets. As a result, in 2022, pet veterinary diets accounted for 11.6% of the North American pet food market by value.

- Veterinary diets have gained popularity among dog owners as they recognize the importance of specialized nutrition for dogs' health. Dogs are the largest consumers of pet veterinary diet food, with a market value of USD 4.68 billion in 2022. This segment is projected to experience a growth of 101.3% between 2023 and 2029, reaching a market value of USD 10.41 billion in 2029. This growth can be attributed to the increasing population of dogs in the region and the rising trend of pet adoption.

- In North America, cats are the second most popular pets and a significant consumer base for pet nutraceuticals, with a value of USD 2.42 billion. In line with the rapid growth of the cat population at a rate of 13.6% between 2017 and 2022, the cat veterinary diet food market is projected to register a CAGR of 9.1% during the forecast period, making it one of the fastest-growing segments among pets.

- Other animals, such as birds, small mammals, and rodents, have significant requirements for veterinary diets to prevent health problems. As a result, the pet nutraceuticals market value for other animals in the region was USD 1.34 billion in 2022.

- The increasing pet populations, growing concerns about pet health, and rising pet health issues are driving the growth of the market during the forecast period.

The United States is the largest pet veterinary market in North America due to its growing trend of pet humanization

- Veterinary diets are crucial in pet care, offering specially formulated foods for pets with specific diseases or infections, either for prevention or cure. These diets have become a significant segment of the pet food market in North America, accounting for an 11.6% share in 2022. Over the years, the veterinary diet market has shown steady growth in the region. It registered a significant increase in 2020 and has continued to grow ever since. This can be attributed to the rise in pet adoption during the pandemic.

- In North America, the United States emerged as the largest market for pet veterinary diets in 2022. Its dominance has been steadily increasing for over a decade and is estimated to be sustained over the coming years. The market's growth in the United States can be attributed to the prevalent usage of commercial pet food and the growing trend of pet humanization, where pets are regarded as family members and receive specialized care.

- The United States and Mexico are expected to be the fastest-growing countries in the pet veterinary diets market within North America, registering CAGRs of 10.8% and 8.5%, respectively, during the forecast period. This accelerated growth can be attributed to the rapid increase in pet adoption, as observed in previous trends.

- Digestive sensitivity and urinary tract disease diets held significant shares, amounting to 21% and 20.5%, respectively, in 2022. The higher prevalence of these diseases among common pets, such as dogs and cats, contributes to their larger market shares.

- Therefore, the increasing incidence of infections and diseases in pets and growing awareness among pet owners regarding the benefits of veterinary diets are projected to drive the North American market to register a CAGR of 10.5% during the forecast period.

North America Pet Diet Market Trends

Growing pet humanization and increasing adoptions of cats, particularly by young adults and millennials, driving the cat population

- Cats as pets have been adopted in North America due to the high demand for companionship and less expenditure on pet food for cats compared to other pets. In the region, the number of cats as pets increased by 13.6% between 2017 and 2022 due to a rise in pet humanization and since cats require less space to live. For instance, in the United States, in 2020, 26% of households owned a cat as a pet.

- The United States, Canada, and Mexico witnessed high adoption of cats as pets after the COVID-19 pandemic because there was an increase in pet ownership stimulated by remote work. A higher number of pet owners belong to the millennial generation. For instance, in 2022, millennials accounted for 33% of pet parents in the United States, and in 2020, 40% of the cat pet population was adopted from animal shelters in the United States. Pet parents with high incomes also purchased cats from pet stores, and in 2020, 43% of cat parents in the United States purchased cats from pet stores. Therefore, the cat pet population in North America increased by 5.34% between 2020 and 2022.

- There is a higher adoption of young cats in the United States as compared to adult cats by pet parents. For instance, in 2021, the adopted cat population in the United States was about 684,144, and young cats accounted for 53.5% of the cats adopted in the country. The higher population of millennials being pet parents is expected to help in the growth of veterinary diets during the forecast period as cats will be older in the coming years. Factors such as an increase in the adoption and purchase of cats and an increase in pet humanization are expected to help the growth of the pet population which in turn help in the growth of the pet food market in the region.

The veterinary cost is the second-highest expense incurred by pet parents in North America while increasing premiumization is driving pet expenditure in the region

- An increasing trend in pet expenditure is being witnessed in North America. The rise in pet expenditure is due to the availability of different types of pet food and the growing premiumization of pet food products in the United States and Canada. Pet parents are also spending on premium segments such as customized pet food and natural as well as organic pet food in the region.

- The veterinary cost is the second-highest expense incurred by pet parents in North America. Pet parents, particularly dog owners, provide their pets with veterinary diets in their initial days and services such as pet grooming and pet walking for better care of the pets, along with adequate nutrition. In 2022, the veterinary expenditure was 26.4% of the annual expenditure on pets in the United States. In Canada, pet parents have an annual expenditure, including other services, of about USD 960 for their dogs and USD 711 for cats, as people are willing to spend more on veterinary services than other expenses. In the United States, about 40% of pet parents purchased premium pet food, while USD 11.4 billion was spent on services such as pet grooming and pet walking in 2022.

- Pet parents purchase pet food through online retailers, supermarkets, and pet stores. Pet food sales are higher through online retailers as pet parents have access to a vast number of pet food products available on e-commerce sites, and the pandemic increased online orders. For instance, in the United States, online sales of pet care products, including food, increased from 32% in 2020 to 40% in 2022.

- Premiumization and rising awareness about the benefits of quality food are factors anticipated to have helped in increasing pet expenditure in the region.

North America Pet Diet Industry Overview

The North America Pet Diet Market is moderately consolidated, with the top five companies occupying 45.55%. The major players in this market are Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated, Nestle (Purina) and Schell & Kampeter Inc. (Diamond Pet Foods) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50001463

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Product

- 5.1.1 Diabetes

- 5.1.2 Digestive Sensitivity

- 5.1.3 Oral Care Diets

- 5.1.4 Renal

- 5.1.5 Urinary tract disease

- 5.1.6 Other Veterinary Diets

- 5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

- 5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

- 5.4 Country

- 5.4.1 Canada

- 5.4.2 Mexico

- 5.4.3 United States

- 5.4.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Affinity Petcare SA

- 6.4.2 Alltech

- 6.4.3 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.4 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.5 General Mills Inc.

- 6.4.6 Mars Incorporated

- 6.4.7 Nestle (Purina)

- 6.4.8 PLB International

- 6.4.9 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.