PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1433808

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1433808

India Health and Medical Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

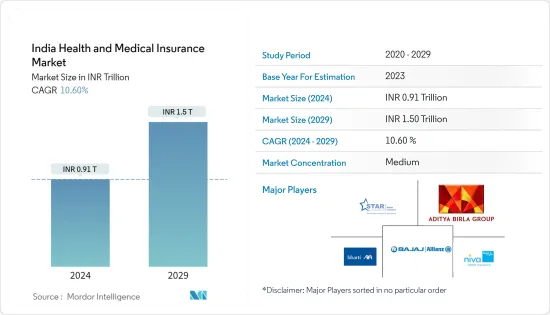

The India Health and Medical Insurance Market size is estimated at INR 0.91 trillion in 2024, and is expected to reach INR 1.5 trillion by 2029, growing at a CAGR of 10.60% during the forecast period (2024-2029).

Health and Medical Insurance is a type of health coverage that pays for medical expenses incurred because of an illness. These costs could be related to hospitalization, medication, or doctor consultation fees. The increasing cost of quality healthcare and increased demand for healthcare coverage due to growing income levels, rising life expectancy, and the epidemiological shift toward noncommunicable diseases have made health and medical coverage mandatory in India.

Health insurance is a major contributor to the expansion of the general insurance market in India. It contributes to approximately 29% of total general insurance premium income in India. The expansion of this sector is significant in terms of the overall expansion of the general insurance industry. The insurance market is expanding due to significant government initiatives, strong democratic factors, a favorable regulatory framework, growing partnerships, product innovations, and dynamic distribution networks. Health insurance is a rapidly growing sector of the Indian economy. For instance, as per the India Brand Equity Foundation, in the fiscal year 2020, there was an increase in health insurance coverage. In Bihar, Assam, and Sikkim, the proportion of households with health insurance increased by 89% in FY20 compared to FY16.

While the global pandemic had an impact on many industries, COVID-19 spurred growth in the Indian insurance sector. The health and medical insurance industry of India demonstrated its importance by offering COVID-19-specific health insurance plans and providing assistance to policyholders. Health insurance plan sales increased amid COVID-19, which benefited both customers and insurers. Health insurance providers with exclusive facilities and benefits were in higher demand. For instance, the Insurance Regulatory and Development Authority of India (IRDAI) mandated and instructed health insurers to include COVID-19 coverage in all policyholders' regular health insurance plans.

Health insurance is an emerging insurance sector in India, following life and automobile insurance. The rise of the middle class, higher hospitalization costs, expensive health care, digitization, and an increase in awareness are some important drivers for the growth of India's health insurance market. The health insurance industry is at an emerging stage. There exists a huge potential for growth and penetration of health insurance among a larger population. Additionally, there are both opportunities and restraints in the marketing and distribution of health insurance products in India.

India Health Insurance Market Trends

Government Subsidized Health Insurance Schemes is Boosting the Sales of Health and Medical Insurance Policies

India's health and medical insurance market is growing because of big government programs, strong democratic factors, a good regulatory environment, steadily more partnerships, new products, and strong distribution channels.

Government programs and financial inclusion initiatives are likely to have aided in driving adoption and penetration across all segments. AB PM-JAY is an entitlement-based scheme funded entirely by the government under Ayushman Bharat. It is the world's largest health assurance scheme, aiming to provide INR 500,000 ($6,900) per family per year for secondary and tertiary care hospitalization to over 107 million vulnerable families (approximately 500 million beneficiaries). Nearly 514 million people in India were covered by health insurance schemes in the fiscal year 2021. The majority of these people were covered by government-sponsored health insurance plans, while the minority were covered by individual insurance plans.

Focus Towards Growth of General Insurance is Driving the Growth of the Industry

According to the Insurance Regulatory and Development Authority of India (IRDAI), the penetration of general insurance in FY 2021 was nearly 1%. This is especially low in India, owing to the lack of awareness within the population. However, the IRDAI as announced aspirational targets to reach a penetration of 2.52% by 2027. Further, the IRDAI has given growth targets for next five years for non-insurance companies such as ICICI Lombard, Bajaj Allianz General, HDFC Ergo, and others. Additionally, it has also asked public sector insurers to increase premiums by 25% annually, and private sector insurers to surge the premiums by 40% each year. This will assist the general insurance sector to gain a significant growth in the overall insurance industry in India.

India Health Insurance Industry Overview

The Health and Medical Insurance Market is moderately consolidated. The increasing number of new players in the market is expected to increase the competition levels for the established market players. The rapid adoption of advanced technology for improved healthcare, as well as the introduction of new policies, are significant factors influencing the competitive nature. Furthermore, to gain market share, players are employing various strategies such as expansion, merger and acquisition, partnership, and collaboration.Some of the key players operating in the market are Star Health, Aditya Birla, Niva Bupa Health Insurance (Formerly known as Max Bupa Health Insurance), Bajaj Allianz Health Insurance, Bharti AXA Life Insurance, Reliance Health Insurance, and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porters' Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Insights of Technology Innovations in the Market

- 4.6 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type of Insurance Provider

- 5.1.1 Public Sector Insurers

- 5.1.2 Private Sector Insurers

- 5.1.3 Standalone Health Insurance Companies

- 5.2 By Type of Customer

- 5.2.1 Non-Corporate

- 5.2.2 Corporate

- 5.3 By Type of Coverage

- 5.3.1 Individual Insurance Coverage

- 5.3.2 Family or Floater (Group)Insurance Coverage

- 5.4 By Product Type

- 5.4.1 Disease- specific Insurance

- 5.4.2 General Insurance

- 5.5 By Demographics

- 5.5.1 Minors

- 5.5.2 Adults

- 5.5.3 Senior Citizens

- 5.6 By Distribution Channel

- 5.6.1 Direct to Customers

- 5.6.2 Brokers

- 5.6.3 Individual Agents

- 5.6.4 Corporate Agents

- 5.6.5 Online

- 5.6.6 Bancassurance

- 5.6.7 Other Distribution Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Star Health and Allied Insurance Co Ltd

- 6.2.2 Aditya Birla Group

- 6.2.3 Niva Bupa Health Insurance Company Limited

- 6.2.4 Bajaj Allianz Health Insurance

- 6.2.5 Bharti AXA Life Insurance

- 6.2.6 Religare

- 6.2.7 HDFC Ergo

- 6.2.8 Oriental Insurance

- 6.2.9 ICICI Lombard

- 6.2.10 United India Insurance

- 6.2.11 Reliance Health Insurance

- 6.2.12 New India Assurance

- 6.2.13 National Assurance

- 6.2.14 Cigna TTK*

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 DISCLAIMER AND ABOUT US