PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1434285

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1434285

LED Farming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

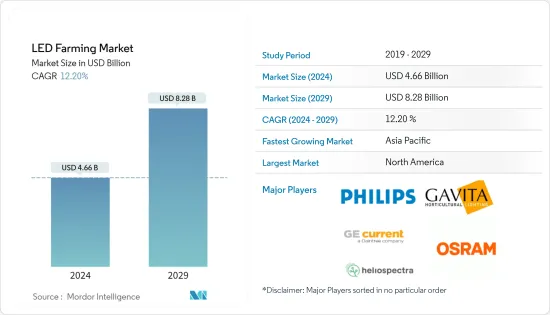

The LED Farming Market size is estimated at USD 4.66 billion in 2024, and is expected to reach USD 8.28 billion by 2029, growing at a CAGR of 12.20% during the forecast period (2024-2029).

Key Highlights

- The advent of Controlled Environment Agriculture (CEA) in terms of vertical farming has had a significant role to play in the LED farming market. Increased reliability, energy-efficiency, diversified products, and reduced long-term costs are the key features driving the penetration of LED lighting in vertical farms.

- North America held the largest market size in the global LED farming market in 2019, followed by indoor farms and commercial greenhouses. The onset of the urban populationdwelling across cities, such as New York, Chicago, and Milwaukee, Toronto, and Vancouver, has propelled the establishment of indoor farms in shipping containerized form or building-based farms to cater to the emerging need for fresh grown foods.

- The market for LED farming is fairly fragmented with the well-established players and emerging companies equally vying for a stronger foothold in the market. Some of the key players in the market includeKoninklijke Philips N.V., Gavita International B.V., General Electric Company, OSRAM Opto Semiconductors GmbH, Heliospectra AB, Hortilux Schreder B.V., and Illumitex, among others.

LED Farming Market Trends

Vertical Farming to Lead the LED Farming Market

The onset of vertical farming has embarked on a revolutionary trend for the light-emitting diode (LED) technology. A rapid transition has been witnessed in Controlled Environment Agriculture (CEA) from only high-value crops such as cannabis to a wide-ranging variety such as microgreens and vegetables owing to the affordable and efficient LED lights thrusting the agricultural technology market. According to the US Department of Energy, the price of LEDs dropped by 90% whole their efficiency increased double-fold between the period 2010-2014. Empirical observations have revealed that LEDs are 40% to 70% more energy-efficient and suitable for vertical farms than high-pressure sodium (HPS) lights or metal halide (MH) lamps. According to the European Research Council, lighting contributed the largest share of 35.8% valued at USD 268.0 million to the total revenue of vertical farming, globally, in 2016. This signifies that LED lights have played a pivotal role in vertical farming and is further expected to witness a rapid growth in this segment during the forecast period.

North America - The Largest Market in LED Farming

North America accounted for the largest share in the global LED farming market in 2019. The United States contributed the largest portion of the total revenue generated in the region. The US has been surfaced with farmland scarcity and the subsequent need for higher productivity of crops. According to the United States Department of Agriculture (USDA) estimates, the amount of land used for agricultural purposes fell by 100,000 acres in Alabama and Georgia in 2015 while the percentage of agricultural land in the total land area fell steadily from 44.58% in 2015 to 44.36% in 2017. As of 2016, the total number of commercial-scale vertical farms in the US approached 20 and is further expected to rise with increased investment in the agricultural technology sector, thus, giving a boost to the LED farming market. The Agricultural Research Service has also undertaken a project to increase tomato production in the US and the quality of production in other protected environments using LED lights. Moreover, a "fresh-from-farm-to-table" consumption preference has encouraged several Canadian players such as Modular Farms, Goodleaf Farms, Nova Scotia's TruLeaf, and Ecobain Gardens, to turn to urban agriculture to answer food shocks in the country from time to time.

LED Farming Industry Overview

The market is highlycompetitive witha few internationally established players as well as several regional players vying for a higher market share in the emerging market for LED lights in farming. The key players in the market include Koninklijke Philips N.V., Gavita International B.V., General Electric Company, OSRAM Opto Semiconductors GmbH, Heliospectra AB, Hortilux Schreder B.V., and Illumitex, among others. Mergers and acquisitions, innovation, diversification of product portfolios, and investments are some of the most adopted strategies of these players for penetrating the evolving market with an all-encompassing Research & Development approach. For instance, Heliospectra launched thenew modular LED lighting series, MITRA,in May 2019, which provides high-intensity light output and electrical efficacy of up to 2.7 µmol/J forcommercial greenhouses, indoor, and vertical farms.In 2018, OSRAM acquired Fluence Bioengineering, a Texas-based leading provider of LED lighting for commercial crop production, in a bid to enhance its outreach in Europe, the Middle East, and Africa regions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.4 Market Restraints

- 4.5 Industry Attractiveness - Porter's Five Force Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Vertical farming

- 5.1.2 Indoor Farming

- 5.1.3 Commercial Greenhouse

- 5.1.4 Turf and Landscaping

- 5.2 Wavelength

- 5.2.1 Blue Wavelength

- 5.2.2 Red Wavelength

- 5.2.3 Far Red Wavelength

- 5.3 Crop Type

- 5.3.1 Fruits & Vegetables

- 5.3.2 Herbs & Microgreens

- 5.3.3 Flowers & Ornamentals

- 5.3.4 Other Crop Types

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 US

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 UK

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 UAE

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Koninklijke Philips N.V.

- 6.3.2 Gavita International B.V.

- 6.3.3 General Electric Company

- 6.3.4 OSRAM Opto Semiconductors GmbH

- 6.3.5 Heliospectra AB

- 6.3.6 Hortilux Schreder B.V.

- 6.3.7 Illumitex

- 6.3.8 LumiGrow

- 6.3.9 Smart Grow Systems, Inc.

- 6.3.10 Hubbell

7 MARKET OPPORTUNITIES AND FUTURE TRENDS