PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1436025

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1436025

Global Next-generation Implants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

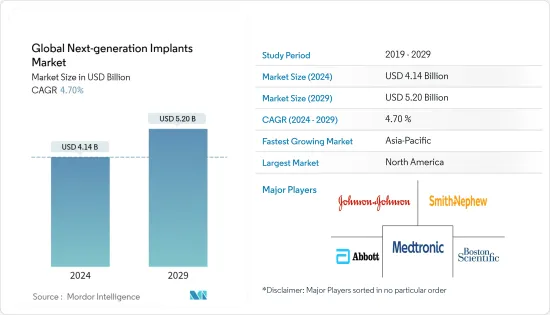

The Global Next-generation Implants Market size is estimated at USD 4.14 billion in 2024, and is expected to reach USD 5.20 billion by 2029, growing at a CAGR of 4.70% during the forecast period (2024-2029).

The COVID-19 pandemic shut down population movements and transport systems across large parts of the world due to the rising COVID-19 cases. Most countries also implemented travel restrictions, which led to a decline in medical services. The number of visits to hospitals and clinics decreased with the decline in elective surgical procedures which impacted the next-generation medical implants market. The implant manufacturers encountered many challenges, including scarcity of resources, shifts in the supply and demand chain, and revenue decline compared to the growth rate in the past decades. The next-generation implant market was hindered by the COVID-19 pandemic in the short term. For instance, according to an article titled 'Cochlear Implant Surgery During the Covid Pandemic Lockdown-The KEM Hospital, Pune Experience' published in August 2022, during the COVID-19 pandemic elective surgeries such as cochlear implantation were postponed to divert medical resources to COVID-19 management. However, with the reducing severity of the COVID-19 infection, the next-generation implants market is expected to resume a strong growth rate post-COVID-19 pandemic.

The growing aging population, higher life expectancy, and an increase in the number of age-related disorders are contributing to the growth of the next-generation implant market. The geriatric population is more prone to cardiovascular, orthopedic, and dental degenerative conditions, which increases the demand for next-generation implants. According to the World Health Organization (WHO) report on Ageing and Health published in October 2021, between 2015 and 2050, the proportion of the world's population over 60 years will nearly double from 12% to 22%. The report estimated that the population of people over 60 years would have outnumbered the population of children below the age of 5 years in 2020. Also, as per the same source, about 80% of the geriatric population will be living in low- and middle-income countries by 2050. The growing older population is expected to further increase the demand for innovative treatment procedures, thereby, accelerating the growth of the next-generation implants market all around the world.Moreover, according to the World Population Ageing 2020, the largest increase is projected to occur in Eastern and South-Eastern Asia, growing from 261 million in 2020 to 573 million in 2050. The fastest increase in the number of older persons is expected in Northern Africa and Western Asia, rising from 29 million in 2020 to 96 million in 2050.

Another factor is the growing prevalence of degenerative disease and the burden of chronic disease globally. According to the National Health Institute's article on neurodegenerative diseases published in June 2022, over 6.2 million in the United States were estimated to be affected by Alzheimer's disease and over a million adults were estimated to be affected by Parkinson's in the year 2022. Age-related macular degeneration makes a significant contribution to degenerative disorders.

Additionally, technological advancements have been resulting in the development and introduction of medical implants that are more simplified than earlier available products. Various companies are currently offering more advanced implants, such as bioabsorbable stents, cardioverter-defibrillators, personalized joint replacements, and leadless pacemakers, which offer improved operation and extended battery life and allow patients to continue normal activities after implantation. The innovation by the market players is a major factor adding to the growth of the market. For instance, in June 2021, Medtronic PLC gained the United States Food and Drug Administration (FDA) clearance for Vanta, a high-performance rechargeable implantable neurostimulator. The novel product launches are expected to add to the growth of the studied market over the forecast period.

However, major restraining factors for the growth of the studied market are the high cost of next-generation implants and stringent regulatory policies for implants.

Next-generation Implant Market Trends

The Orthopedic Implants Segment is Expected to Occupy a Significant Share of the Market During the Forecast Period

Orthopedic implants are artificial bones or joints designed to replace or support a missing or injured bone or joint. These implants are designed to correct abnormalities and improve body posture. The rise in the geriatric population, which raises the risk of osteoporosis, osteoarthritis, and other musculoskeletal problems, is one of the major factors for the growth of the segment market. For instance, according to an article titled 'Bone health 2022: an update' published in the journal of 'Climacteric' in January 2022, osteoporosis causes more than 8.9 million fractures annually all over the world, resulting in an osteoporotic fracture every 3 seconds. The article indicated that osteoporosis affects 200 million women worldwide. Also, as per an article by the American Society for Biochemistry and Molecular Biology on Osteoporosis Awareness Month 2022 published in May 2022, osteoporosis will be responsible for three million fractures resulting in USD 25.3 billion in costs every year by the end of the year 2025. According to these statistics, the number of orthopedic surgeries is expected to increase, driving the demand for orthopedic implants in the coming years.

Additionally, several factors drive the segmental growth, such as advances in joint replacements and increased investment by key market participants in orthopedic implant research and development activities. For instance, Intelligent Implants Ltd's SmartFuse Implant technology, a next-generation technological platform for orthopedics, gained the United States Food and Drug Administration (FDA)'s breakthrough device designation in June 2021. The orthopedic implants segment is expected to expand rapidly during the analysis period, owing to increased demand for innovative therapies, minimally invasive procedures, and increased patient knowledge of orthopedic implants.

Therefore, owing to the above-mentioned factors, the orthopedic implants segment is expected to have a significant growth during the forecast period.

North America is Expected to Dominate the Next-generation Implant Market During the Forecasts Period

North America currently dominates the next-generation implants market and is expected to follow the same trend over the forecast period. The rising trend in the geriatric population, the rising prevalence of chronic disease, changing lifestyles, and the availability of advanced medical facilities are anticipated to boost the growth of the next-generation implant market. According to the article on arthritis by the United States Centers for Disease Control and Prevention (CDC) updated in October 2021, around 58.5 million people in the country were affected by doctor-diagnosed arthritis. As per the same source, by the year 2040, over 78.4 million adults in the United States will be affected by arthritis. Also, as per the Arthritis Society Canada article on arthritis facts and figures updated in September 2021, around 6 million Canadians were found to be affected by arthritis in 2021, with an estimate of over 9 million arthritis cases by the year 2040. The rising cases of arthritis are expected to boost the market growth in the region over the forecast period.

Similarly, technological advancement and improvement in the products are expected to boost growth in the region. For instance, in June 2022, ZimVie Inc., a life sciences solutions provider in the dental and spine markets, launched the new, FDA-cleared T3 PRO Tapered Implant and Encode Emergence Healing Abutment in the United States. Such product launches in the region are likely to add to the growth of the next-generation implant market.

Thus, owing to the above-mentioned factors, the studied market in North America is expected to propel over the forecast period.

Next-generation Implant Industry Overview

The next-generation implants market is mostly fragmented with many market players focusing on advancement in the technology to deliver more efficient and cost-effective implant devices to leverage growth opportunities in the market. Some of the major players are vigorously making collaborations, mergers, and acquisitions to consolidate the market position across the world. The several players in the next-generation implants market are Abbott Laboratories, Smith & Nephew PLC, Johnson & Johnson, Boston Scientific Corporation, C.R. Bard Inc., Wright Medical Group NV, Stryker Corporation, Globus Medical Inc., DENTSPLY SIRONA Inc., and Zimmer Biomet Holdings Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Aging Population

- 4.2.2 Growing Prevalence of Degenerative Disease

- 4.2.3 Technological Advancement in Next-generation Implants

- 4.3 Market Restraints

- 4.3.1 High Cost of Next Generation Implants

- 4.3.2 Stringent Regulatory Reforms

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - in USD Millions)

- 5.1 By Application

- 5.1.1 Orthopedic Implants

- 5.1.2 Cardiovascular Implants

- 5.1.3 Ocular Implants

- 5.1.4 Dental Implants

- 5.1.5 Other Applications

- 5.2 By Material

- 5.2.1 Metals and Metal Alloys

- 5.2.2 Ceramics

- 5.2.3 Polymers

- 5.2.4 Biologics

- 5.2.5 Other Materials

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Orthopedic Clinics

- 5.3.4 Academic and Research Institutes

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Smith & Nephew PLC

- 6.1.3 Johnson & Johnson

- 6.1.4 Boston Scientific Corporation

- 6.1.5 C.R. Bard Inc.

- 6.1.6 Medtronic PLC

- 6.1.7 Wright Medical Group NV

- 6.1.8 Stryker Corporation

- 6.1.9 Globus Medical Inc.

- 6.1.10 DENTSPLY SIRONA Inc.

- 6.1.11 Zimmer Biomet Holdings Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS