PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1437620

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1437620

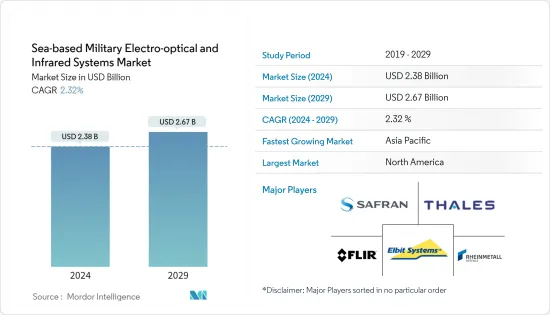

Sea-based Military Electro-optical And Infrared Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Sea-based Military Electro-optical And Infrared Systems Market size is estimated at USD 2.38 billion in 2024, and is expected to reach USD 2.67 billion by 2029, growing at a CAGR of 2.32% during the forecast period (2024-2029).

Many countries are investing in sophisticated electro-optical and infrared (EO/IR) systems for maritime purposes, including threat detection, surveillance, and target identification, due to the rise in maritime conflicts and dangers to naval vessels around the world.

The increasing tensions among nations in the vicinity of the Northern Atlantic and Arctic waters and the South China Sea are fueling the expansion of naval vessel and boat production and acquisition. This aspect is driving the market growth of electro-optical and infrared systems for military use at sea. Technological innovations are also fueling the development of advanced EO/IR systems worldwide. The use of sensor-based imaging and tracking systems that rely on EO/IR technology gives navies an advantage in extreme weather and day/night situations, thus improving their situational awareness while at sea.

Sea-Based Military Electro-Optical & IR Systems Market Trends

Hyperspectral Segment is Projected to Showcase Highest Growth during the Forecast Period

The growth of territorial conflicts and border issues increased the risk for militaries' maritime assets, which led to increasing emphasis on surveillance, threat detection, and target identification at sea. As modern combats involve a greater emphasis on these capabilities, armed forces primarily focus on incorporating and integrating sophisticated and advanced hyperspectral imaging technologies into their naval vessels. The growth of this segment is expected to increase due to rising military expenditure and various modernization efforts by major global powers. For instance, in 2022, the global military expenditure reached USD 2,240 billion, a growth of 6% from 2021.

Navies need to obtain motion imagery from EO/IR sensors that provide day-night, long-range eyes on the target, which improves their ability to identify targets, perform threat assessment, assess intent according to the rules of engagement, and support weapon engagement through automatic tracking and fire control solutions through line-of-sight. Hence, various companies are developing advanced hyperspectral imaging EO/IR solutions for improved protection in the sea. For instance, in March 2023, an Australian company named Arkeus launched its cutting-edge hyperspectral sensor solution called the Hyperspectral Optical Radar (HSOR). This advanced technology is designed for a range of applications, including ISR in the sea and improving maritime domain awareness. As the naval vessels are isolated from the terrain, it becomes important for them to possess advanced threat detection and countermeasure systems for their long-term survival from impending threats. This is driving the growth of the R&D segment currently. Such developments are expected to drive this segment's demand during the forecast period.

Asia-Pacific to Exhibit the Highest Growth Rate during the Forecast Period

The demand for sea-based military EO/IR systems market in Asia-Pacific is driven by increasing tensions and conflicts, particularly in the South China Sea, the East China Sea, and the Indian Ocean. Many nations, including China, have directed their attention toward upgrading their naval capabilities by investing significantly in the latest advancements in EO/IR technologies. China is actively integrating its Over-the-horizon Surface Wave (OTH-SW) radars and electro-optical sites into its anti-ship missile systems. The combined system provides accurate targeting information about enemy ships and submarines.

For instance, in April 2023, China's latest Type 055 destroyer was officially inducted into the country's Navy. The destroyer features navigation radars, various communication and intelligence systems, electronic warfare support measures (ESM), electronic countermeasures (ECM), electro-optic (EO) sensors, laser-warning systems, optronic jammers, and datalink systems. Similarly, in December 2023, Japan started building 24 new FFM missile frigates called the Mogami class. These are being procured in two batches of 12 each. These frigates feature Mitsubishi Electric's OPY-2 X-band multi-purpose active electronically scanned array (AESA) radar and OAX-3 electro-optical/infrared (EO/IR) sensors. Such developments in the naval industry and ongoing naval vessel procurement and modernization programs are expected to drive growth for the sea-based military electro-optical and infrared systems market during the forecast period.

Sea-Based Military Electro-Optical & IR Systems Industry Overview

The sea-based military electro-optical & IR systems market is semi-consolidated as only a few players account for a major market share. Companies such as Elbit Systems Ltd, Rheinmetall AG, Teledyne FLIR LLC, Thales, and Safran SA dominate the market. The market is witnessing much innovation in technologies like long-distance and infrared ranging and sensor fusion. The key players in the market compete on the price and quality of the products, and the growing naval market provides a huge opportunity for key players to generate revenues by gaining new installation and system upgrade contracts.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Imaging Technology

- 5.1.1 Multispectral

- 5.1.2 Hyperspectral

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 India

- 5.2.3.2 China

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Australia

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 Egypt

- 5.2.5.3 Israel

- 5.2.5.4 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Elbit Systems Ltd

- 6.2.2 Saab AB

- 6.2.3 BAE Systems PLC

- 6.2.4 Thales

- 6.2.5 Northrop Grumman Corporation

- 6.2.6 Teledyne FLIR LLC

- 6.2.7 Rafael Advanced Defense Systems Ltd

- 6.2.8 Rheinmetall AG

- 6.2.9 Safran SA

- 6.2.10 HENSOLDT AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS