PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1440330

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1440330

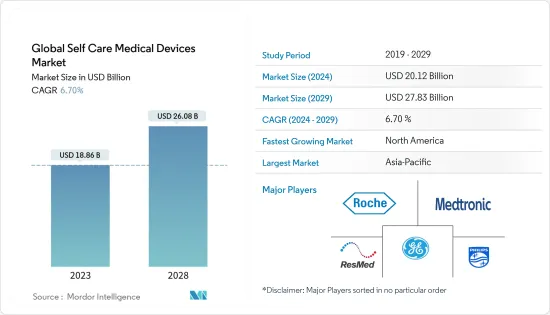

Global Self Care Medical Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Global Self Care Medical Devices Market size is estimated at USD 20.12 billion in 2024, and is expected to reach USD 27.83 billion by 2029, growing at a CAGR of 6.70% during the forecast period (2024-2029).

Globally, the COVID-19 pandemic put enormous pressure on hospitals and healthcare systems that were understaffed and overworked. According to the study titled "Home health monitoring during the COVID pandemic: Results from a feasibility study in Alberta primary care," published in the Healthcare management forum in January 2022, Patients were comfortable with the home healthcare monitoring technology, and more than 60% patients reported an improvement in their quality of life after follow-up. Patients also visited their family physician/emergency department less frequently than in the previous year. Moreover, according to the study titled "Role of self-care in COVID-19 pandemic for people living with comorbidities of diabetes and hypertension" published in the Journal of Family Medicine and Primary Care in November 2020, Dietary precautions, medication adherence, home-based exercises, self-monitoring of blood glucose and blood pressure, salt reduction, self-foot examination, and stress management are all suggested as necessary elements of self-care. Thus, to monitor self-care, the demand for self-care devices increased during COVID-19. Thus, self-care medical devices were positively impacted during the COVID-19 pandemic.

There has been an increase in demand for devices that can continuously track patients' physical well-being due to the rising prevalence of chronic and lifestyle diseases such as cardiovascular disease (CVD) and diabetes, as well as rising consumer health awareness. According to the July 2021 update by the World Health Organization, cardiovascular diseases are the leading cause of death around the world, including diseases like coronary heart disease, cerebrovascular disease, rheumatic heart disease, congenital heart disease, and others. Additionally, according to the data published by the International Diabetes Federation (IDF) Diabetes Atlas Tenth Edition 2021, in the year 2021, approximately 537 million adults (aged 20-79 years) were living with diabetes. The same source estimated that the total number of people living with diabetes is projected to rise to 643 million by 2030 and 783 million by 2045. The rising burden of diabetes is likely to increase the demand for more technically advanced self-care medical devices.

Furthermore, according to the WHO, by 2030, one out of every six people on the planet will be 60 years old or older. The number of people aged 60 and up is expected to rise from 1 billion in 2020 to 1.4 billion by 2050. By 2050, the global population of people aged 60 and above will get double to reach 2.1 billion. Between 2020 and 2050, the number of people aged 80 and above is expected to triple, reaching 426 million.

The market players adopted various strategies such as product launches, product developments, collaborations, and expansions to increase their market revenue. For instance, in November 2021, Abbott, the global healthcare launched the FreeStyle Libre system, the continuous glucose monitoring (CGM) technology available for adults and children (above the age of four) living with diabetes in India and women with gestational diabetes (diabetes during pregnancy), allowing them to check their glucose levels at any time and from any location, resulting in better glucose control.

Thus, all aforementioned factors are anticipated to drive the market over the forecast period. However, the availability of alternative devices and the high cost of the products restraint the market over the forecast period.

Self Care Medical Devices Market Trends

Blood Glucose Monitors Segment is Expected to Dominate the Market Over the Forecast Period

Blood glucose monitors had the largest market share when compared to other self-care medical devices. The number of people diagnosed with diabetes has been steadily increasing due to sedentary lifestyles, poor dietary habits, and the growing geriatric population. Furthermore, technological advancements and growing awareness about diabetes management are driving the market for blood glucose monitors to grow over the forecast period. For instance, as per the September 2021 report of the International Diabetes Federation, in 2021, approximately 537 million adults (20-79 years) were living with diabetes. The total number of people living with diabetes is projected to rise to 643 million by 2030 and 783 million by 2045.

The market players in the country adopted various strategies such as product launches, product developments, collaborations, and expansions to increase their market revenue. In July 2021, Terumo Corporation launched Dexcom G6 continuous glucose monitoring system in Japan. Dexcom, Inc., based in the United States, manufactures the product and Terumo holds the exclusive distribution agreement in Japan.

Similarly, in November 2021, The POGO Automatic Blood Glucose Monitoring System (Intuity Medical) was cleared by the Food and Drug Administration for people with diabetes aged 13 and up. In the United States, a new type of blood sugar monitoring system allows users to test with a single button press rather than finger-sticking or inserting test strips into a meter.

Thus, all aforementioned factors are anticipated to drive the segment growth over the forecast period.

North America Dominates the Market and Expected to do Same in the Forecast Period.

With the increase in product launches supported by the government authorities, the rising burden of chronic diseases and the increasing geriatric population are leading to a rise in demand for self-care medical in the United States.

The COVID-19 pandemic has changed the landscape of healthcare delivery in the United States, with a new shift toward self-care monitoring. According to a research article by Darren Roblyer published in the Journal of Biomedical Optics in October 2020, industrial and academic research projects use these devices to predict a variety of health outcomes and disease states, including surgical recovery, overall mortality, mental health, heart conditions, and other diseases states. Adding to that, in April 2020, during the COVID-19 pandemic in the United States, telehealth claims accounted for 20% of submitted medical and dental claims in the northeastern United States.

According to the National Diabetes Statistics Report updated in January 2022 published by the Centers for Disease Control and Prevention (CDC), around 37.3 million people have diabetes (11.3% of the United States population). Additionally, as per the same source, 28.7 million people, including 28.5 million adults were diagnosed with diabetes in 2021. Furthermore, according to the Statistics Canada Report titled 'Older adults and population aging statistics, published in July 2020, the number of people aged 65 years or over is about 6,835,866 in 2020. Since chronic diseases such as cardiac diseases have a high prevalence in the older population and have more chances to affect the older population, the burden of the geriatric population will drive the demand for patient monitoring systems, thereby boosting the demand for self-care medical devices in the region.

In addition, due to the high growth potential of the United States, the companies operating in the country are filing for new product approvals to have an edge over their competitors, which is further expected to augment the growth of the studied market in the country over the forecast period. For Instance, in January 2021, Omron Healthcare reported retail availability for HeartGuide, the first wearable blood pressure monitor. The highly-anticipated HeartGuide, an oscillometric blood pressure monitor in the design of a wrist watch, received 510K FDA clearance as a medical device.

Self Care Medical Devices Industry Overview

The self-care medical devices market is moderately fragmented. Various medical device manufacturers are operating in the market, along with several specialized self-care medical device manufacturers. The industry is highly competitive, and there is a growing trend of partnerships and agreements between the industry participants and other medical device manufacturers to incorporate self-care medical device functionalities into their devices. Some of the key market players include Medtronic plc., Koninklijke Philips N.V., Bayer HealthCare LLC, General Electric Company, F. Hoffmann-La Roche AG, and Johnson & Johnson.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Chronic Diseases and Lifestyle Diseases Coupled with The Geriatric Population

- 4.2.2 Growing Preference for Home- Based Treatment Due to Hectic Lifestyle

- 4.3 Market Restraints

- 4.3.1 Availability Of Alternative Options, And High Costs of Devices.

- 4.3.2 Side Effects and Risks Associated with Implantation of Self-Care Medical Devices

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Type

- 5.1.1 Blood Glucose Monitors

- 5.1.2 Blood Pressure Monitors

- 5.1.3 Body Temperature Monitors

- 5.1.4 Nebulizers

- 5.1.5 Pedometers

- 5.1.6 Pregnancy/Fertility Test Kits

- 5.1.7 Others

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Middle-East and Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle-East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Medtronic plc.

- 6.1.2 Koninklijke Philips N.V.

- 6.1.3 Bayer HealthCare LLC

- 6.1.4 General Electric Company

- 6.1.5 F. Hoffmann-La Roche AG

- 6.1.6 Johnson & Johnson

- 6.1.7 ResMed, Inc.

- 6.1.8 Omron Healthcare, Inc.

- 6.1.9 OraSure Technologies, Inc.

- 6.1.10 Abbott Inc.

- 6.1.11 B. Braun Melsungen

7 MARKET OPPORTUNITIES AND FUTURE TRENDS