Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693589

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693589

Commercial Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 338 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

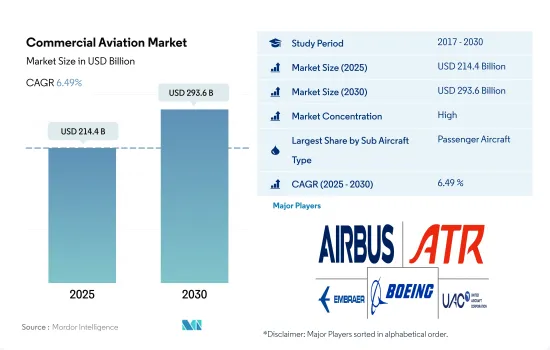

The Commercial Aviation Market size is estimated at 214.4 billion USD in 2025, and is expected to reach 293.6 billion USD by 2030, growing at a CAGR of 6.49% during the forecast period (2025-2030).

The Growth In Air Passenger Traffic And The Increasing Demand For Fuel-Efficient And Modern Aircraft Are Expected To Boost The Commercial Aviation Industry Globally

- According to the UNWTO, tourism contributes 10% of the world's GDP, making it one of the main sources of income in the modern world, with 57% of cross-border travelers using aircraft. In the last 15 years, the number of passengers in commercial aviation has doubled. During the forecast period, a total of 14,080 commercial aircraft are expected to be delivered, some of which may replace the current fleet's more aged aircraft. The COVID-19 pandemic affected air passenger traffic globally in 2020, reducing flight activity and impacting airline cash flows. As a result, most airlines decided to cancel or defer their aircraft orders.

- However, the commercial aviation industry recovered gradually in 2022, which led to a significant increase in aircraft deliveries compared to 2021. Airlines are looking for aircraft with better fuel efficiency and range, and the development of newer aircraft may help OEMs attract more airline customers in the coming years. In terms of deliveries during 2017-2022, a total of 2,049 aircraft were procured by various airlines globally. Of these total 2,049 aircraft, passenger aircraft accounted for 96%, and freighter aircraft accounted for 4%.

- Since the domestic passenger demand is anticipated to return to pre-COVID-19 levels earlier than the international passenger demand, the market for narrowbody aircraft is anticipated to rebound faster than the demand for widebody aircraft. The 737 MAX's return to service in late 2020 may also support the expansion of the narrowbody segment. Such developments are expected to drive the demand in the market. A total of 13,812 passenger aircraft and 268 freighter aircraft are expected to be delivered globally during the forecast period

Asia-Pacific Is Expected To Be The Most Lucrative Market In The Commercial Aviation

- North America is expected to be the second-highest-growing region after Asia-Pacific. In terms of aircraft deliveries, North America's commercial aircraft accounted for almost 29% of the total commercial aircraft worldwide from 2017 to 2022. Aircraft deliveries are expected to rise by 57% from 2023 to 2030. North America may be accountable for 27% of total aircraft deliveries during the forecast period. Europe's commercial aircraft accounted for 17% of the total commercial aircraft worldwide from 2017 to 2022.

- Air travel in South America contracted to 199.15 million air passengers in 2021 compared to 210.73 million passengers traveled in 2020. During the forecast period, Europe, Middle East & Africa, and South America may account for around 20%, 9%, and 3% of total aircraft deliveries, respectively.

- The COVID-19 pandemic greatly impacted the commercial aircraft market due to a halt in global transportation. The stringent lockdowns enforced worldwide also significantly impacted the economic conditions of the commercial aircraft market. Therefore, in 2021, international passenger demand was 75.5% lower than in 2019. Asia-Pacific (APAC) is projected to grow at a healthy rate between 2023 and 2030.

- Domestic passenger traffic has been steadily increasing in the APAC region, although the pandemic had a significant impact on the region's aviation industry. In 2022, the APAC region contributed 38% of total air passenger traffic worldwide.

- The region's rising per capita income due to economic and infrastructure growth contributed to the growth of air passenger numbers and supported the expansion of the regional and domestic airlines' fleets. Narrowbody aircraft accounted for approximately 83% of total deliveries during the period.

Global Commercial Aviation Market Trends

Ease of travel restrictions and the rising number of passengers are driving the demand

- As cross-border travel was progressively restored, the carriers in the Asia-Pacific have raced to put on flights to meet runaway demand, stimulated by the pent-up desire to travel and savings accumulated in the two years of isolation due to COVID-19. As a result, in 2022, air passenger traffic in the region recovered more rapidly from the pandemic than other regions. For instance, in 2022, air passenger traffic in Asia-Pacific was recorded at 2.2 billion, witnessing a growth of 10% compared to 2021. Moreover, airline companies in the region are implementing fleet expansion plans to cater to the growing air passenger traffic in the major countries in the region. China, India, Japan, and Indonesia account for 70% of the total air passenger traffic in Asia-Pacific and are expected to generate more demand for new aircraft compared to other countries in the region.

- Airlines in Asia-Pacific witnessed a notable recovery in international air passenger markets as pent-up travel demand continued to fuel growth despite increasingly challenging global economic conditions. The passenger load factor for the region's airlines also improved, showing a year-on-year increase of 17.9 ppts and reaching 78.8%. These developments in total ASK and passenger load factor are highly encouraging and support the increasing demand for air travel in the region. Moreover, the healthy growth in international passenger traffic shows strong travel demand from the business and leisure sectors. The rapid increase in air passenger traffic in the region is expected to drive the air transport industry in the future.

Commercial Aviation Industry Overview

The Commercial Aviation Market is fairly consolidated, with the top five companies occupying 90.21%. The major players in this market are Airbus SE, ATR, Embraer, The Boeing Company and United Aircraft Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92739

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.1.1 Asia-Pacific

- 4.1.2 Europe

- 4.1.3 Middle East and Africa

- 4.1.4 North America

- 4.1.5 South America

- 4.2 Air Transport Freight

- 4.2.1 Asia-Pacific

- 4.2.2 Europe

- 4.2.3 Middle East and Africa

- 4.2.4 North America

- 4.2.5 South America

- 4.3 Gross Domestic Product

- 4.3.1 Asia-Pacific

- 4.3.2 Europe

- 4.3.3 Middle East and Africa

- 4.3.4 North America

- 4.3.5 South America

- 4.4 Revenue Passenger Kilometers (rpk)

- 4.4.1 Asia-Pacific

- 4.4.2 Europe

- 4.4.3 Middle East and Africa

- 4.4.4 North America

- 4.4.5 South America

- 4.5 Inflation Rate

- 4.5.1 Asia-Pacific

- 4.5.2 Europe

- 4.5.3 Middle East and Africa

- 4.5.4 North America

- 4.5.5 South America

- 4.6 Regulatory Framework

- 4.7 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Aircraft Type

- 5.1.1 Freighter Aircraft

- 5.1.2 Passenger Aircraft

- 5.1.2.1 Narrowbody Aircraft

- 5.1.2.2 Widebody Aircraft

- 5.2 Region

- 5.2.1 Asia-Pacific

- 5.2.1.1 Australia

- 5.2.1.2 China

- 5.2.1.3 India

- 5.2.1.4 Indonesia

- 5.2.1.5 Japan

- 5.2.1.6 Malaysia

- 5.2.1.7 Philippines

- 5.2.1.8 Singapore

- 5.2.1.9 South Korea

- 5.2.1.10 Thailand

- 5.2.1.11 Rest of Asia-Pacific

- 5.2.2 Europe

- 5.2.2.1 France

- 5.2.2.2 Germany

- 5.2.2.3 Italy

- 5.2.2.4 Netherlands

- 5.2.2.5 Russia

- 5.2.2.6 Spain

- 5.2.2.7 Turkey

- 5.2.2.8 UK

- 5.2.2.9 Rest of Europe

- 5.2.3 Middle East and Africa

- 5.2.3.1 Algeria

- 5.2.3.2 Egypt

- 5.2.3.3 Qatar

- 5.2.3.4 Saudi Arabia

- 5.2.3.5 South Africa

- 5.2.3.6 United Arab Emirates

- 5.2.3.7 Rest of Middle East and Africa

- 5.2.4 North America

- 5.2.4.1 Canada

- 5.2.4.2 Mexico

- 5.2.4.3 United States

- 5.2.4.4 Rest of North America

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Chile

- 5.2.5.3 Colombia

- 5.2.5.4 Rest of South America

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 ATR

- 6.4.3 COMAC

- 6.4.4 De Havilland Aircraft of Canada Ltd.

- 6.4.5 Embraer

- 6.4.6 The Boeing Company

- 6.4.7 United Aircraft Corporation

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.