Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1637883

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1637883

China Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 95 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

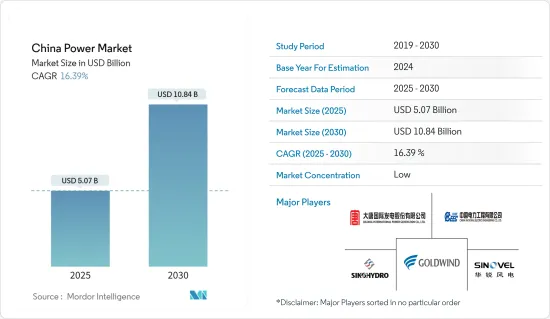

The China Power Market size is estimated at USD 5.07 billion in 2025, and is expected to reach USD 10.84 billion by 2030, at a CAGR of 16.39% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the increasing upcoming investments and the growing manufacturing sector will likely drive the Chinese power market during the forecast period.

- On the other hand, phasing out coal-based power plants, which account for a major share of power generation in China, is expected to hinder the growth of the power market.

- Nevertheless, the Chinese government announced increasing its installation of renewable energy sources to 1200 GW by 2030. It will likely create several opportunities for the Chinese power market in the forecast period.

China Power Market Trends

The Renewable Energy Segment Expected to Dominate the Market

- The Chinese government actively promoted renewable energy development through various policies and incentives, such as subsidies, tax breaks, and regulations. This government support helped to drive growth in the renewable energy sector and is expected to continue in the coming years.

- Moreover, China heavily relies on imported fossil fuels to meet its energy needs. It makes the country vulnerable to price fluctuations and supply disruptions. By investing in renewable energy, China can reduce its dependence on foreign energy sources and increase its energy security.

- Additionally, the cost of renewable energy has decreased rapidly in recent years, making it increasingly competitive with fossil fuels. In some cases, renewable energy is already cheaper than coal-fired power plants. This cost competitiveness makes renewable energy an attractive option for China, which aims to reduce its energy costs.

- In 2022, the electricity generated through renewable energy in China was around 1367 TWh. It is an increase of 19% compared to 2021. A similar trend is expected to be followed during the forecasted period.

- For instance, in March 2022, it was announced by the Chinese government that they intend to construct solar and wind power generation capacity of 450 GW in desert regions such as the Gobi desert. Currently, around 100 GW of solar power capacity is already under construction.

- According to the National Energy Administration (NEA), China connected 32.6 GW of onshore wind capacity in 2022, boosting its total installations to 333.98 GW. Further, the Chinese onshore wind market is expected to grow steadily in the coming years, with rising needs for key components and materials for the national market and international exports. Besides, in China, nearly 70% of the electricity produced is from thermal energy sources. With increasing pollution from thermal sources, the country focuses on increasing the share of cleaner and renewable sources in power generation.

Increasing Upcoming Investment Plans to Drive the Market

- As the world's second-largest economy, China's energy demand grew rapidly to meet its economic development goals. A growing population, urbanization, and industrialization contributed to this demand, increasing the need for electricity generation capacity.

- In 2022, the total electricity generated in China was 8848.7 TWh, an increase of almost 3.6% compared to 2021. This trend is expected to continue as China increases its renewable energy capacity. It will aid in increasing electricity generation capacity.

- Moreover, according to the World Nuclear Association, China currently contains 55 operational nuclear power reactors, with 22 more under construction or development. The Chinese government aims to increase its use of closed-cycle nuclear power in the long term to meet its energy demands, partly due to concerns over the pollution caused by coal-fired power plants.

- In April 2022, China's State Council gave the green light to construct six new nuclear power plants, with plans to build two additional reactors at the Sanmen, Haiyang, and Lufeng nuclear power plant sites. The approved construction involves units 3 and 4 at Sanmen, 3 and 4 at Haiyang, and 5 and 6 at Lufeng. This move is expected to increase China's installed nuclear-generating capacity to 70 GWe by 2025.

- Additionally, the Chinese government shifted its focus on increasing energy security due to recent geopolitical developments like the Russia-Ukraine war. It affected the oil and gas supply globally and China's electricity sector, as the country heavily relies on imported fossil fuels for power generation.

- China is also investing heavily in upgrading other segments of its power sector. It includes transmission and distribution infrastructure in major HVDC and UHVDC projects for transporting renewable electricity from small utility-scale energy projects to demand centers and battery storage capacity to store excess renewable generation while stabilizing the grid.

- For instance, in July 2022, the Baihetan-Jiangsu 800 kV ultra-high-voltage (UHV) direct current power transmission project entered commercial operation, one of the key projects in the larger West-to-East power transmission program. Such developments are expected to help the electricity distribution from utility-scale solar parks.

- Therefore, due to the points mentioned above, the government of China is expected to increase investment in the country's energy sector, which will increase the country's power market.

China Power Industry Overview

The Chinese power market is fragmented. The key players in the market (in no particular order) include Datang International Power Generation Company Limited, China National Electric Engineering Co. Ltd, Xinjiang Goldwind Science & Technology Co. Ltd, Sinohydro Corporation, and Sinovel Wind Group Co. Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 48162

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 China Power Generation and Forecast, in Terawatt, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Upcoming Investments in Renewable Energy Sector

- 4.5.1.2 Growing Manufacturing Sector Increases Demand For Power

- 4.5.2 Restraints

- 4.5.2.1 Rising Phase Out of Coal-based Power Plants

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Power Generation Source

- 5.1.1 Thermal

- 5.1.2 Hydroelectric

- 5.1.3 Nuclear

- 5.1.4 Renewable

- 5.1.5 Other Power Generation Sources

- 5.2 Power Transmission and Distribution (T&D)

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Datang International Power Generation Company Limited

- 6.3.2 China National Electric Engineering Co. Ltd

- 6.3.3 Xinjiang Goldwind Science & Technology Co. Ltd

- 6.3.4 Sinohydro Corporation

- 6.3.5 Sinovel Wind Group Co. Ltd.

- 6.3.6 Wuxi Suntech Power Co. Ltd.

- 6.3.7 China Yangtze Power Co., Ltd.

- 6.3.8 China National Electric Wire & Cable I/E Corp.

- 6.3.9 State Grid Corporation of China

- 6.3.10 Shandong energy group co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Presence of Government Targets to Support Renewable Energy Generation

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.