PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687127

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687127

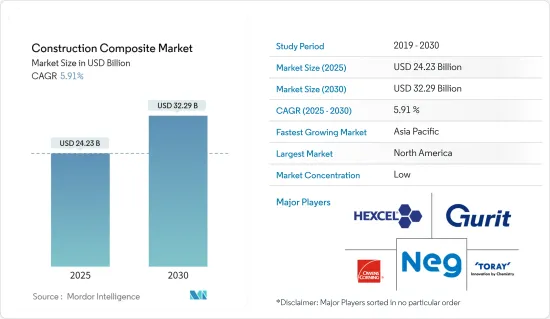

Construction Composite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Construction Composite Market size is estimated at USD 24.23 billion in 2025, and is expected to reach USD 32.29 billion by 2030, at a CAGR of 5.91% during the forecast period (2025-2030).

COVID-19 negatively impacted the market in 2020 as the pandemic severely affected international trade and hampered several industries, including manufacturing, building, and construction. However, in 2021, the market demand from these sectors recovered significantly.

Key Highlights

- Over the medium term, the factors driving the growth of the market studied are the increasing usage of composites in construction applications and the rehabilitation of old concrete structures.

- On the other hand, the high initial production and installation costs of composites, coupled with the inadequacy of skilled labor, are hindering the market's growth.

- Increasing the ability to mass-produce composites in the construction sector will likely create opportunities for the market in the coming years.

- North America is expected to dominate the market in terms of revenue while the Asia-Pacific region is likely to witness the highest CAGR during the forecast period.

Construction Composites Market Trends

Civil Construction Sector to Dominate the Market

- Civil construction comprises the construction of bridges, dams, roads, airports, canals, railway infrastructure, and related structures.

- Toward the end of 2021, several Chinese provinces announced major infrastructure projects. South China's Guangxi Zhuang Autonomous Region unveiled a batch of major construction projects, with a total investment of CNY 185.9 billion (USD 29.15 billion). Those projects cover many sectors, including transportation, new energy, logistics, and basic infrastructure.

- Furthermore, China plans to expand its railway network, which is the second-largest in the world, by one-third in the next 15 years, as part of a long-term plan to propel urbanization and stimulate local economies. According to a plan issued by the state-owned China State Railway Group, China aims to have about 200,000 km (124,274 miles) of railway tracks by the end of 2035, including about 70,000 km of high-speed railways.

- In Germany, the Ministry of Transport and Digital Infrastructure plans to invest USD 348.72 million in future technologies, such as electric mobility or automated and networked driving for electric vehicle charging infrastructure. Also, the country has started working on the A49 highway project connecting Schwalmstadt and the Ohmtal interchange in Central Hesse. This, in turn, is expected to increase the consumption of composite materials.

- The Schwalmstadt-Ohmtal project is based on a public-private partnership model with an investment of USD 813.68 million. The construction, which comprises 93 km of road, is expected to be completed in the third quarter of 2024. These massive railway and road construction projects may drive the demand for construction composites during the forecast period.

- According to US Census Bureau, annual value of highway and street construction put in place of United states, in 2021 accounted for USD 100.68 million, compared to USD 102.32 million in 2020.

- In Canada, as part of the "Investing in Canada" plan, the government announced plans to invest nearly USD 140 billion in major infrastructure developments in the country by 2028.

North America Region to Dominate the Market

- In North America, the utilization of construction composites is increasing due to the growing construction sector in countries such as the United States, Canada, and Mexico.

- The North American region is one of the largest consumption markets for construction composites. The United States has one of the world's largest construction industries. In the full year 2021, construction spending amounted to USD 1,590.37 billion, 8.2% above USD 1,469.2 billion in 2020, thereby increasing the consumption of construction composites from various construction applications.

- According to the US Census Bureau, during February 2022, the construction spending in the country was estimated at a seasonally adjusted annual rate of USD 1704.4 billion, 0.5% more than the revised January estimate of USD 1,695.5 billion. Moreover, the February 2022 estimation is 11.2% more than the February 2021 estimate of USD 1,533.3 billion. During the first two months of 2022, construction spending amounted to USD 237.8 billion, 10.4% percent above USD 215.4 billion for the same period in 2021.

- In Canada, the residential and commercial sectors have been witnessing steady growth in the recent past. There has been a boom in the construction of skyscrapers in Canada (more specifically in Toronto) in recent times. Over 30 high-rise buildings are expected to be completed by 2025, and another 50 such buildings are in the proposal and planning phases in Toronto.

- Moreover, as part of the ''Investing in Canada Plan'', the government has announced plans to invest nearly USD 140 billion in infrastructure developments in the country by 2028.

Construction Composites Industry Overview

The global construction composite market is fragmented. Some major players in the market (in no particular order) include Hexcel Corporation, Owens Corning and Nippon Electric Glass Co. Ltd., Toray Industries Inc., and Gurit.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Use of Composites in Construction Applications

- 4.1.2 Rehabilitation of Old Concrete Structures

- 4.2 Restraints

- 4.2.1 High Initial Production and Installation Costs of Composites

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Revenue)

- 5.1 Resin Type

- 5.1.1 Polyester Resin

- 5.1.2 Vinyl Ester

- 5.1.3 Polyethylene

- 5.1.4 Polypropylene

- 5.1.5 Epoxy Resin

- 5.1.6 Other Resin Types

- 5.2 Fiber Type

- 5.2.1 Carbon Fibers

- 5.2.2 Glass Fibers

- 5.2.3 Natural Fibers

- 5.2.4 Other Fiber Types

- 5.3 End-use Sector

- 5.3.1 Industrial

- 5.3.2 Commercial

- 5.3.3 Housing

- 5.3.4 Civil

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) ** / Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles (Overview, Financials, Products and Services, and Recent Developments)

- 6.4.1 Aegion Corporation

- 6.4.2 Exel Composites

- 6.4.3 Gurit

- 6.4.4 Hexcel Corporation

- 6.4.5 Kordsa Teknik Tekstil AS

- 6.4.6 Toray Industries Inc.

- 6.4.7 Mitsubishi Chemical Corporation

- 6.4.8 Nippon Electric Glass Co. Ltd

- 6.4.9 Owens Corning

- 6.4.10 SGL Carbon

- 6.4.11 Teijin Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Ability to Mass Produce Composites in the Construction Sector