PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444718

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444718

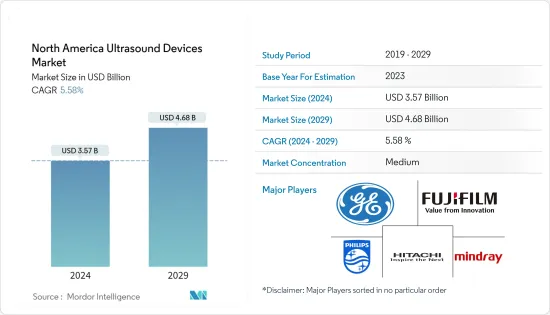

North America Ultrasound Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The North America Ultrasound Devices Market size is estimated at USD 3.57 billion in 2024, and is expected to reach USD 4.68 billion by 2029, growing at a CAGR of 5.58% during the forecast period (2024-2029).

The outbreak of the COVID-19 pandemic pushed the medical device industry into action with a race to develop both therapeutic and preventive devices. There was an increased use of ultrasound devices during COVID-19, which positively impacted the market during the pandemic. For instance, according to the PubMed study published in August 2020, the American College of Radiology discouraged the use of routine imaging procedures such as chest radiographs and encouraged the use of ultrasound. It also stated that handheld ultrasound devices fit into a single-use plastic cover and can be easily decontaminated, making them ideal for minimizing viral contamination and spread during the pandemic. Many handheld ultrasound devices now have teleguidance capabilities that allow professionals to guide a novice user through an exam remotely, minimizing exposure, conserving personal protective equipment, and reducing patient transport for imaging procedures. Therefore, owing to such factors, the use of ultrasound devices was positively impacted during the pandemic in the North American region.

The main things that are driving the market are the growing use of diagnostic imaging, the rise of chronic diseases, and the speed with which technology is improving.

The increasing prevalence of chronic diseases in North American countries such as the United States and Canada is fueling market growth. For instance, as per the report published by the American Cancer Society in January 2022, around 19,880 women are expected to be diagnosed with ovarian cancer. It was also reported that ovarian cancer ranks fifth in cancer deaths among women. In addition, it also reported a woman's risk of getting ovarian cancer during her lifetime is about 1 in 78, and her lifetime chance of dying from ovarian cancer is about 1 in 108.

The American Cancer Society also stated that cancer mainly develops in older women. Around half of the women who were diagnosed with ovarian cancer were 63 years of age or older. It is more common in white women than in African-American women. Ultrasound is the initial and most important imaging modality for the detection of ovarian cancer. Moreover, ultrasound is also considered an accurate technique for the determination and monitoring of ovarian cancer. Therefore, such instances are anticipated to propel the market's growth over the forecast period.

Furthermore, Sonography Canada, an organization dedicated to the ultrasound sector in Canada, announced its strategic plan for the year 2023-2026 in February 2022. Owing to such strategic movements in the country, the market studied is expected to witness strong growth in Canada.

But strict changes to regulations are likely to slow the market's growth over the next few years.

North America Ultrasound Devices Market Trends

Portable Ultrasound Segment is Expected to Witness a Healthy Growth Over the Forecast Period

Portable ultrasound devices are mobile ultrasound systems designed for use in small spaces, such as points of care and beside hospital beds. It can be cart-based, tablet-based, or hand-carried. Portable ultrasound units are becoming standard equipment in many clinics, affording easy access to this imaging modality.

The growth of the segment is owing to the significant technological advancements in the development of various portable or hand-held ultrasound devices, rising cases of chronic diseases, and a wide range of applications with added advantages, which are the major factors propelling the segment's growth over the forecast period. For instance, in August 2021, EchoNous scaled up the production of its portable ultrasound platform with a full-body probe after getting approval from the United States Food and Drug Administration. Lexa, an ultrasound probe, was designed specifically for the Kosmos platform, the first hybrid point-of-care ultrasound (POCUS) tool. Hence, with such new product launches in the United States, the segment is expected to witness strong growth in the forecast period.

Furthermore, increasing strategic movement by the key companies operating in the portable ultrasound business is contributing to segment growth in the North American region. EagleViewUltrasound, for example, launched its first portable doppler ultrasound in January 2022, allowing clinicians to quickly access ultrasound images at any time, easing point-of-care diagnosis.Such launches will open opportunities for market growth due to the rise in the adoption of portable ultrasound devices for easy diagnosis.

Because of this, the segment is expected to grow at a fast rate over the next few years, thanks to improvements in technology and strategic moves by key companies.

The United States is Expected to Hold a Significant Share in the Market Over the Forecast Period

Over the forecast period, the United States is expected to hold a significant share of the overall North American ultrasound devices market. The growth is due to factors such as rising cases of chronic diseases, technological advancements, key product launches, a high concentration of market players' or manufacturers' presence, and acquisitions and partnerships among major players.

The increasing number of hospitals operated by private players in the United States is propelling the growth of the market. According to the American Hospital Association Statistics Report, in 2021, there were 2,946 nongovernment, not-for-profit community hospitals, and this number increased to 2,960 in 2022. The increased number of hospitals creates a demand for medical devices such as ultrasound, which is expected to drive market growth.

Furthermore, product launches and partnership deals among major players are anticipated to drive the market in the country. For example, in May 2022, Butterfly Network announced that it had signed a deal with the Medical University of South Carolina (MUSC) to provide its point-of-care ultrasound devices and software to the organization, which includes its medical school, research facilities, and 14 hospitals.

Because of this, the studied market is expected to grow in the United States because there are more and more hospitals and more and more ultrasound devices are coming out.

North America Ultrasound Devices Industry Overview

The North American ultrasound devices market is fragmented and competitive and consists of several major players. The market comprises major players who are focusing on R&D to form a stable and safe formulation. The market has been noticing technological developments on a large scale for the past couple of years. The competitive landscape includes an analysis of a few international as well as local companies that hold market shares and are well known, including Fujifilm Holdings Corporation, GE Healthcare (a GE Company), Hitachi Medical Corporation, Mindray Medical International Ltd., Koninklijke Philips NV, Hologic Inc., Siemens Healthcare, and Canon Medical Systems Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased Adoption of Diagnostic Imaging

- 4.2.2 Increasing Prevalence of Chronic Diseases

- 4.2.3 Rapid Technological Advancements

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Reforms

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Type

- 5.1.1 Stationary Ultrasound

- 5.1.2 Portable Ultrasound

- 5.2 By Technology

- 5.2.1 2D Ultrasound Imaging

- 5.2.2 3D and 4D Ultrasound Imaging

- 5.2.3 Doppler Imaging

- 5.2.4 High-intensity Focused Ultrasound

- 5.3 By Application

- 5.3.1 Anesthesiology

- 5.3.2 Cardiology

- 5.3.3 Gynecology/Obstetrics

- 5.3.4 Musculoskeletal

- 5.3.5 Radiology

- 5.3.6 Critical Care

- 5.3.7 Other Applications

- 5.4 Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Fujifilm Holdings Corporation

- 6.1.2 GE Healthcare

- 6.1.3 Hitachi Medical Corporation

- 6.1.4 Mindray Medical International Ltd

- 6.1.5 Koninklijke Philips NV

- 6.1.6 Hologic Inc.

- 6.1.7 Siemens Healthineers

- 6.1.8 Canon Medical Systems Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS