PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1642192

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1642192

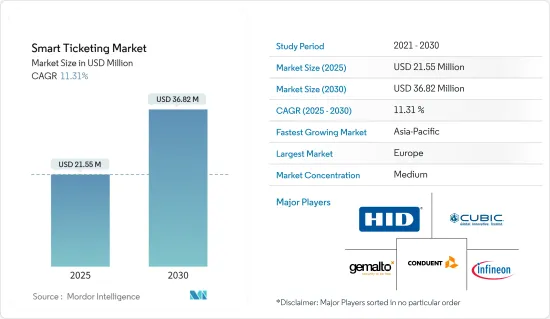

Smart Ticketing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Smart Ticketing Market size is estimated at USD 21.55 million in 2025, and is expected to reach USD 36.82 million by 2030, at a CAGR of 11.31% during the forecast period (2025-2030).

Smart tickets, as a substitute for traditional paper-based ticketing, gained traction recently due to the emphasis on digitizing ticketing processes. Smart tickets can save a passenger's time by eliminating the need to wait in line to buy a ticket. Also, covering both smartcards and apps on mobile phones, the technology evolved significantly and emerged as a better alternative to paper tickets.

Key Highlights

- Widely used across different forms of transportation, the use cases are increasing across sports and entertainment events. One such example of a use case is the city of Rio de Janeiro, which hosted the Olympic Games and anticipated 500,000 foreign visitors. The public transport ticketing displayed the contactless technology of Gemalto. The company supplied its waterproof 'Celego Contactless Wristband' and its 'Celego Contactless Sticker,' embedded with a contactless chip from Gemalto and certified by Visa and MasterCard. Also, activated with a wave of the wristband near the contactless readers, the solution was one of the major innovations introduced in the region to improve the infrastructure.

- Regional governments are even reaching new milestones in terms of the usage of smart tickets. For instance, according to the Rail Delivery Group (RDG), a British rail industry membership body, more train journeys were made with smart tickets, reaching 65 million. Compared to four weeks from August to September 2019, with the same period in 2018, about 8.4 million more journeys were made with a smart ticket. The RDG data also reveals that passengers chose smart tickets for 50% of all trips, significantly increasing from 37% a year ago.

- The trend of mobile ticketing is also becoming popular among several sports and entertainment events. Several prominent American Football stadiums and associated sports teams implemented mobile ticketing in Europe. With fans entering stadiums via mobile access provisions, this trend is expected to gain traction in Europe. Such increasing interest may challenge the growth of smartcards over the forecast period.

- Rambus, a prominent company in the market, predicts that mobile may become a critical factor for the future of public transport. Furthermore, smart and mobile ticketing can support a better transport experience and improve efficiency during peak times. For instance, the iMOVE testbed in Melbourne, Australia, aims to create a user-focused transport system more responsive to disruption, which can be possible by collecting data from cars, cyclists, public transport, traffic infrastructure, and pedestrians. Other cities, including the United Kingdom, are also expected to take a similar approach.

- Since the pandemic struck, contactless fare payments have become the norm. The increasing adoption of more brilliant payments has enabled safe, seamless travel. As the world is continuously fighting the rapid spread of the COVID-19 pandemic, contactless payments in transportation applications are playing a very crucial role in helping to safeguard people and ensuring to protect that vehicle operator from collecting fares while avoiding close contact with riders.

Smart Ticketing Market Trends

Smart wearables Occupies the Significant Share

- Smart cards' growth for smart ticketing systems, coupled with the growth prospects from multiple applications, increases the demand for other ticketing systems, such as contactless methods through smartphones, the latest devices, and smart wearables.

- Furthermore, wearables have become very popular due to consumer growth in the fitness trend. According to Cisco Systems, the number of linked wearable devices is anticipated to rise from 593 million in 2018 to 1,105 million in the current year. Due to new features, such as the brand that fits an everyday lifestyle, the smartwatch industry is growing. To retain their income, powerful companies like Apple and Fossil keep their prices in line with the price ranges of conventional watches. Many more upscale watchmakers, including TAG and Armani, have entered the market thanks to Google's WearOS.

- Smart wearable manufacturers, including Samsung, have enabled payment through their smartwatches. Most device manufacturers make payments through their mobile wallets' payment-enabled services, such as Apple Pay, Samsung Pay, Garmin Pay, Fitbit Pay, and GooglePay. Although costs through smartwatches are still in their initial stages, they show a lot of potentials. Such advancements are expected to enable travelers to purchase tickets through their wearable devices.

- Similarly, companies like Watchdata Technologies offer a wide range of products catering to the innovative ticketing system, including smart mobile terminals, smart wearable devices, contact, and contactless EMV, UICC, e-ID and transportation smartcards, online security tokens, card readers, electronic toll collection (ETC) devices. The end-to-end solutions include secure hardware, operating systems, software applications, and personalization and remote lifecycle management services.

Europe Holds the Largest Market Share

- Europe is the home of the leading smart ticketing solution vendors, such as Infineon Technologies, Gemalto, and Giesecke+Devrient (Germany), which are also increasing their presence in this market by offering integrated payment solutions through partnerships with smart ticket developers and operators.

- The demand for smart ticketing in Germany is driven by the growing tourism industry, the simplified technology ecosystem, and the need to innovate more potential ticketing systems across urban areas. The leading payment solution vendors in the region are also increasing their presence in this market by offering integrated payment solutions through partnerships with smart ticket developers and operators.

- With more than 4 billion trips yearly, Paris Region is one of the largest transit networks worldwide, offering its travellers the benefits of contactless mobile ticketing - compatible with existing contactless readers based on Calypso's open transit standard. Firms, like Wizway solutions, as enabled contactless mobile ticketing for several key transit authorities and operators.

- Technological advancements in smart ticketing have propelled businesses to adopt technologies like RFID, NFC, QR codes, and barcode in Germany. The rise of smartphones equipped with NFC technology has introduced the necessary infrastructure for smart ticketing across the industries in the region. RFID technology is extensively used in smart cards due to its cost-effectiveness and is commonly accepted in entertainment, sports, and transport, among other industries.

Smart Ticketing Industry Overview

The smart ticketing market is moderately concentrated, and with the increasing government initiatives supporting this market, more global players are expected to enter this market. Product launches, high expenses on research and development, partnerships and acquisitions, etc., are the prime growth strategies these companies adopt to sustain the intense competition. Some global players are Cubic Corporation, Infineon Technologies AG, and HID Global. Some of the recent developments in the market are:

- July 2022 - Helsingin Seudun Liikenne (HSL), the Helsinki Region Transport Authority, has chosen Conduent to implement a next-generation fare collection system across its network of buses, trams, trains, metros, and ferries, according to Conduent Transportation, a global business unit of Conduent Incorporated. Two hundred thirty-eight million passengers boarded HSL's public transportation systems in 2021.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGTHS

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitute Products

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Intelligent Transportation

- 5.1.2 Growing Adoption of Modern Technology for Different Mode of Transportation such as Railways and Roadways is Propelling the Implementation of Smart Ticketing

- 5.1.3 Increasing usage of Smart wearable to drive the market growth

- 5.2 Market Restraints

- 5.2.1 High Initial Setup Costs

6 TECHNOLOGY SNAPSHOT

- 6.1 Connectivity

- 6.1.1 Near-field Communication (NFC)

- 6.1.2 Radio-frequency Identification (RFID)

- 6.1.3 Barcode

- 6.1.4 Cellular Network and Wi-Fi

7 MARKET SEGMENTATION

- 7.1 By Offering

- 7.1.1 Smart Cards

- 7.1.2 Wearables

- 7.1.3 Readers

- 7.1.4 Others (Validators, Ticketing Mobile Terminals/Ticketing Machines)

- 7.2 By Application

- 7.2.1 Transportation

- 7.2.1.1 Railways

- 7.2.1.2 Airways

- 7.2.1.3 Roadways

- 7.2.2 Sports & Entertainment

- 7.2.1 Transportation

- 7.3 By Geography

- 7.3.1 North America

- 7.3.1.1 United States

- 7.3.1.2 Canada

- 7.3.2 Europe

- 7.3.2.1 Germany

- 7.3.2.2 United Kingdom

- 7.3.2.3 France

- 7.3.2.4 Rest of Europe

- 7.3.3 Asia Pacific

- 7.3.3.1 China

- 7.3.3.2 Japan

- 7.3.3.3 India

- 7.3.3.4 Australia and New Zealand

- 7.3.3.5 Rest of APAC

- 7.3.4 Rest of the World

- 7.3.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Cubic Corporation

- 8.1.2 Infineon Technologies

- 8.1.3 Conduent Inc

- 8.1.4 Vix Technology

- 8.1.5 Rambus Incorporated ( Visa Inc.)

- 8.1.6 Hid Global

- 8.1.7 Gemalto Nv ( Thales Group)

- 8.1.8 Giesecke+Devrient

- 8.1.9 Indra Sistemas

- 8.1.10 Confidex Ltd.

- 8.1.11 NEC Electronics (NEC Corporation)

- 8.1.12 Paragon ID ( Paragon Group Limited)

- 8.1.13 Softjourn, Inc.

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET